Bitcoin Investment Fundamentals 2026 Guide

Bitcoin in 2026 is no longer driven by the four-year halving cycle. Spot ETFs, institutional flows and macro liquidity now set the tone. This guide gives you a complete framework — allocation, custody, ETFs, DCA and regional tax context — built for serious US, EU and UK investors who want a structured approach rather than market timing.

Why Bitcoin Looks Different in 2026

Most Bitcoin guides written today still teach the four-year halving cycle as the master narrative. That model has weakened. Spot Bitcoin ETFs, approved in January 2024, now move more capital in a typical month than miners produce in a year. And 2025 was the first post-halving year ever to finish in the red — down roughly 6% from its January open by year-end.

The price driver has shifted. Where the halving once dominated, institutional flow, global liquidity and central-bank policy now lead. This guide does not predict where Bitcoin will trade. It does something more useful: it gives you a structured framework for entering Bitcoin in the post-cycle era.

If you have searched Bitcoin investment guides recently, you have probably hit a familiar pattern. Half are influencer-driven enthusiasm focused on price predictions. The other half are institutional research papers written for fund managers, not for individuals. This guide sits in the gap between them. It assumes you have a meaningful sum to allocate and want institutional-quality reasoning rather than influencer enthusiasm — but presented in language that respects your time and your judgement.

The framework covers five practical decisions:

- Allocation — how much Bitcoin fits your portfolio, sized to wealth and behaviour rather than to forecasts.

- Wrapper — ETF or direct ownership, chosen by account structure, not ideology.

- Entry — DCA or lump sum, with concrete frequency and amount selection.

- Custody — exchange, hardware wallet or multi-sig, decided by holding size.

- Tax wrapper — IRA, ISA, SIPP or direct, often the largest after-tax difference.

Each decision has a defensible answer that does not depend on price prediction. We work through them in order. By the end of this guide, you will have a complete framework you can act on this week — and a clear sense of where to read deeper on any single piece. Readers entirely new to digital money may want to step back briefly to how Bitcoin compares to traditional fiat money before tackling allocation.

Three structural shifts define the landscape going into 2026. Bitcoin became investable through traditional brokerage and retirement accounts, with spot ETFs collectively holding well over $100 billion within their first two years. BlackRock, Fidelity and a handful of other large issuers now concentrate a significant share of liquid Bitcoin supply, changing how price discovery works during macro shocks. Volatility has compressed materially compared with prior cycles — drawdowns are still meaningful, but the violent 80%+ corrections that characterised earlier cycles have softened as institutional holders smooth the order book.

What this means in practice is straightforward. The tactics that worked in 2017 and 2021 — buy on the halving, sell on the cycle peak — have lost their statistical edge. The strategies that work in 2026 are slower, less narrative-driven, and more focused on what the individual investor actually controls: position size, custody quality, behavioural discipline through drawdowns, and tax-wrapper efficiency. None of these depend on guessing where Bitcoin will trade in 18 months. All of them produce better outcomes than market timing across any reasonable holding period.

If you read nothing else in this guide, internalise this: in 2026, the strongest predictor of long-term Bitcoin outcomes is rarely entry timing. It is allocation size relative to total wealth, custody quality, behavioural discipline through drawdowns, and minimisation of avoidable tax leakage. Each of those is controllable, whereas price is not.

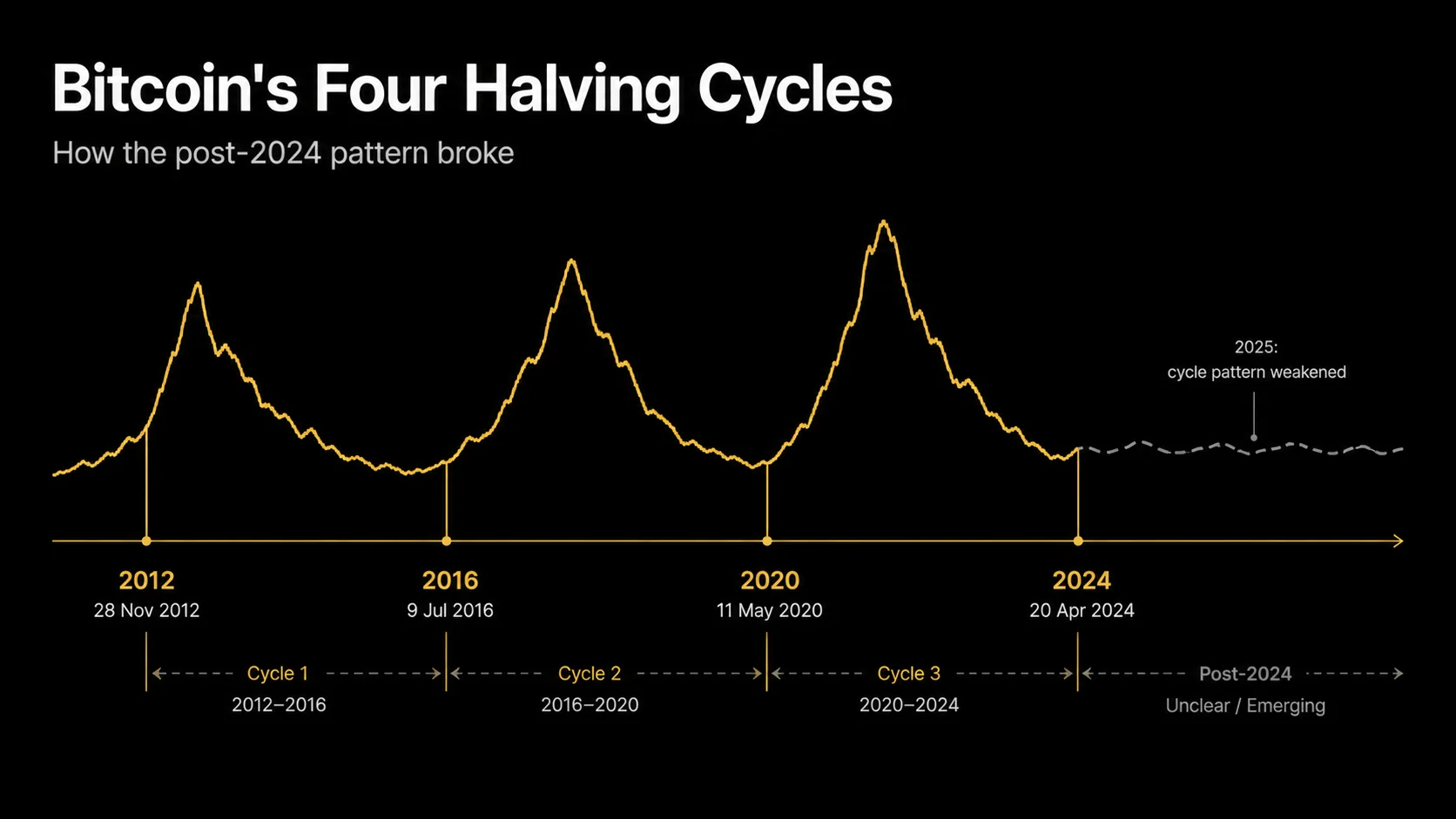

The Halving Cycle Has Evolved

Bitcoin's first three completed cycles followed a recognisable rhythm. Block reward halvings in November 2012, July 2016 and May 2020 each cut new BTC issuance by 50%. Each was followed within 12 to 18 months by a price peak, then a multi-year drawdown of 70-85% before the next cycle began. Investors who timed accumulation to the post-halving year and distribution to the cycle peak outperformed both buy-and-hold and active traders.

The model worked because miner-issued supply was the dominant new-Bitcoin flow into the market. Demand growth was relatively steady year-to-year, so a halving-induced supply cut translated into upwards pressure on price.

The April 2024 halving broke that pattern. Four months earlier, US spot Bitcoin ETFs launched in January 2024 and immediately began absorbing BTC at unprecedented scale. Within their first year, the ETFs collectively accumulated holdings that dwarf typical annual miner issuance. The supply-demand math anchoring the four-year cycle thesis no longer works the same way. When demand-side institutional flows can move more BTC in a quarter than miners produce in a year, the supply-side halving signal becomes a smaller part of the price equation.

The 2025 evidence supports the shift. For the first time in Bitcoin's history, the year following a halving finished negative. Bitcoin closed down roughly 6% from its January open through year-end — a result that contradicts every prior post-halving-year pattern. Volatility compressed as institutional holders smoothed the order book. Drawdowns occurred but were smaller and shorter than in prior cycles. The cycle-peak prediction model that worked through 2021 produced no peak through 2025 and into 2026.

Several forces explain the shift. ETF flows operate on a daily cadence linked to brokerage account flows, retirement-fund rebalancing and macro liquidity conditions. None of these respect the halving schedule. BlackRock's IBIT alone holds a position that represents a meaningful share of liquid supply. Similar concentration exists across the top three or four issuers. Sovereign and corporate treasury holdings have grown materially. The marginal Bitcoin buyer in 2026 is more often a 401(k) auto-rebalance or a wealth manager allocating to an alternatives sleeve than a retail trader chasing the halving narrative.

What replaces the halving cycle as a price-discovery model? The honest answer is that no single replacement model has matured. The most defensible framework treats Bitcoin like any other globally-traded macro asset. Its price reflects net flows from institutional and retail buyers minus net selling pressure from holders and miners. Global liquidity conditions and the relative attractiveness of competing assets mediate that equation. Federal Reserve policy, dollar liquidity and yields on competing assets now move Bitcoin at least as much as the mining schedule does.

The practical implication is straightforward. Cycle-timing strategies built around halving dates have lost their statistical edge. Strategies that fared well in the post-ETF era share three traits:

- Consistent accumulation through dollar-cost averaging rather than calendar-driven entry. Investors who continued buying through the 2025 drawdown ended the period with lower average cost than those who tried to time the cycle bottom.

- Position sizing relative to total wealth rather than to cycle predictions. Investors sized at 5-10% of net worth held through the 2025 chop without forced selling. Investors sized at 30%+ of net worth, betting on a cycle peak, were the ones who sold at unfavourable prices.

- Willingness to hold through drawdowns that no longer follow the previous cycle's timing. The 2022 drawdown was 75% peak-to-trough. The 2025 drawdowns were 30-40% — milder, but extended in duration. Strategies optimised for sharp recovery patterns underperformed strategies built for patient accumulation.

The deeper analysis of this shift — including a section-by-section comparison of supply-driven and demand-driven cycle models — sits in our dedicated cycle satellite.

ETF vs Direct Bitcoin Ownership

Until January 2024, owning Bitcoin meant either holding the asset directly through an exchange or self-custody wallet, or accepting indirect proxy exposure through Bitcoin-mining stocks and futures-based products. The launch of US spot Bitcoin ETFs changed the structure. BlackRock's IBIT, Fidelity's FBTC, ARK 21Shares' ARKB and similar products from other major issuers now offer Bitcoin price exposure inside ordinary brokerage accounts, retirement wrappers and tax-advantaged structures.

Both routes give you Bitcoin exposure. The trade-offs differ on tax wrapper, custody control, fees and accessibility.

What ETFs do well

Spot Bitcoin ETFs hold actual Bitcoin in institutional cold storage on behalf of shareholders. A regulated custodian and standard ETF reporting wrap the structure. They trade on major exchanges during normal market hours and settle through traditional brokers. They fit retirement and tax-advantaged accounts that cannot hold direct Bitcoin.

Expense ratios across the major US issuers sit at 0.20-0.25% per year, materially cheaper than the trading and withdrawal fees most retail investors pay through unit-cost exchange purchases. The operational simplicity itself produces benefits worth pricing in. There is no seed phrase to manage, no hardware wallet to lose, no risk of irreversible address-typing errors. For investors whose Bitcoin allocation lives inside an IRA, 401(k), ISA or pension wrapper, ETFs are usually the only realistic path.

What direct ownership does well

Direct Bitcoin ownership puts you in control of the keys. No annual expense ratio chips at your position over decades. No issuer can suspend redemptions during market stress. You can move funds across borders, send transactions outside business hours, and use Bitcoin as a settlement asset rather than a price-exposure instrument.

Self-custody removes counterparty risk. The historical pattern of large retail losses in crypto comes from custodial failures — exchange collapses, withdrawal freezes — not from market drawdowns. Direct holdings can also provide privacy and optionality that wrapped products cannot match. Both come with corresponding responsibility.

Decision matrix by account structure

The choice often splits along account-structure lines rather than ideological ones. If your Bitcoin allocation belongs inside a tax-advantaged retirement wrapper, ETFs are usually the answer because direct Bitcoin custody is impractical or impossible inside those structures. If your allocation is taxable, the trade-off depends on holding size and custody confidence.

Small positions can stay on a regulated exchange acceptable for ETF-equivalent simplicity. Strategic conviction positions tend to migrate to hardware wallet self-custody, where the lack of expense ratio compounds materially over multi-decade horizons. Many investors split: ETFs in retirement accounts, direct ownership for conviction holdings.

Take a concrete example. A US investor with a $50,000 (£40,000) Bitcoin allocation might hold $30,000 inside a Roth IRA via an ETF for tax-free compounding, and $20,000 in direct Bitcoin on a hardware wallet for self-custody control. A UK investor with the same allocation might hold £30,000 via an ISA-eligible Bitcoin ETP for shielded gains, and £10,000 in direct BTC on a Tangem or Ledger device.

Regional notes

In the US, spot Bitcoin ETFs are available through standard brokerages including Fidelity, Schwab and Vanguard. Self-directed IRAs through specialised custodians can hold direct Bitcoin. The IRS treats both as property for capital-gains purposes. ETF dividends or capital distributions, when present, follow standard 1099 reporting.

In the EU, ETF availability varies. Several Bitcoin ETPs trade on European exchanges and are accessible through major brokers. The specific products and tax treatment differ by country under the broader MiCA framework.

In the UK, regulated brokerages including Hargreaves Lansdown, IG and Trading 212 offer access to Bitcoin ETPs that can be held inside ISA wrappers. ISA shelter can produce significant tax efficiency relative to direct CGT-taxable holdings.

For a deeper walkthrough of the ETF landscape, fee structures, tracking error dynamics and the precise tax-wrapper differences across regions, see our dedicated ETF vs direct Bitcoin satellite.

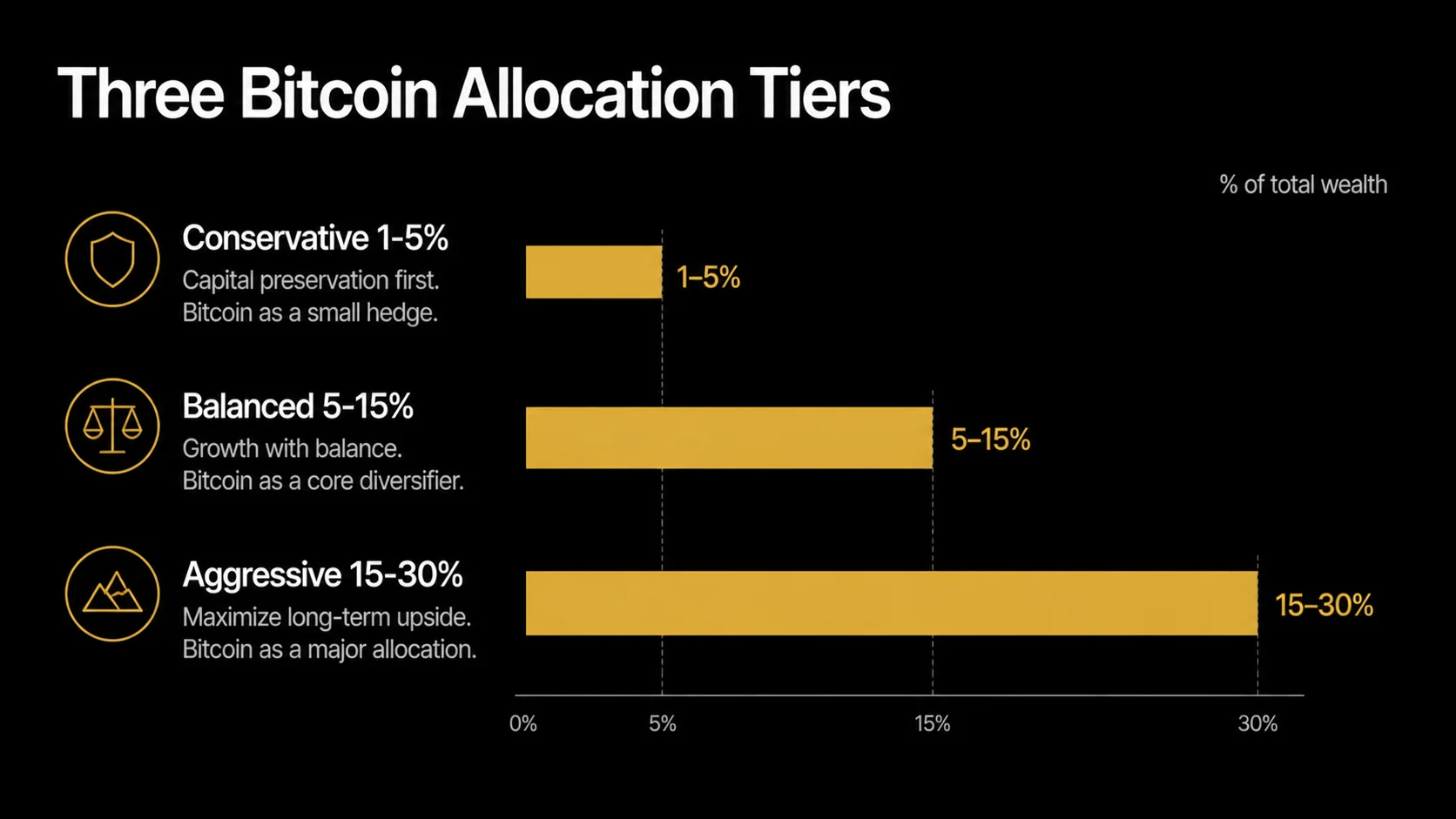

How Much Bitcoin Should You Hold

Allocation sizing is the single most important Bitcoin investment decision, and the most underweighted in popular commentary. A 1% allocation that holds through a 70% drawdown produces meaningfully different outcomes — and behavioural experiences — from a 30% allocation that does the same. The right size for you depends on time horizon, income stability, existing wealth concentration, and tolerance for sustained periods of being underwater on the position. None of that depends on price predictions.

The volatility budget concept

Allocation sizing sits cleanly inside a volatility-budget framework. Bitcoin has historically experienced peak-to-trough drawdowns of 50-85% across its multi-year cycles. Even with the volatility compression of the post-ETF era, drawdowns of 40-50% remain plausible during macro shocks.

The test is simple. If a 40-50% drop in your Bitcoin position would force you to sell other assets at a bad time, harm your retirement timeline or trigger emotional decisions that compound the loss, your allocation is too large. If the same drop produces a meaningful but absorbable hit to net worth that does not change your behaviour, your allocation is calibrated.

Conservative tier: 1-5% of investable assets

The conservative tier treats Bitcoin as a small alternatives sleeve inside a traditional portfolio. A 60/40 stock-bond split with a 2% Bitcoin sleeve, drawn proportionally from equities, produces a portfolio that captures meaningful Bitcoin upside without exposing the investor to position-size-induced behavioural failures during drawdowns.

This tier suits investors near retirement, those with concentrated single-stock or single-property wealth, and anyone whose income cannot absorb a Bitcoin drawdown that coincides with a job loss or other shock.

Concrete example: a $125,000 (£100,000) portfolio with a 2% allocation holds $2,500 of Bitcoin. Large enough to matter if the asset compounds. Small enough that a 70% drawdown costs $1,750 — a real loss, but one that does not reshape the household balance sheet.

Balanced tier: 5-15% of investable assets

The balanced tier treats Bitcoin as a meaningful but not dominant portfolio component. A 10% allocation in a portfolio that otherwise holds equities, bonds and cash gives Bitcoin enough weight to materially influence long-term returns without making the portfolio a Bitcoin proxy.

This tier suits investors with 10+ year horizons, stable income, and existing diversification across other asset classes. The trade-off is real. A 60% Bitcoin drawdown removes 6% from total portfolio value, which most investors with stable income can absorb behaviourally if they expected it. The same drawdown at a 30% allocation removes 18% from total portfolio value — a level that often produces forced selling regardless of the investor's prior conviction.

Aggressive tier: 15-30% of investable assets

The aggressive tier is for investors with strong prior conviction, long horizons, stable wealth structures and demonstrated ability to hold through prior drawdowns. Position sizes above 30% start to dominate portfolio outcomes and behaviour.

Investors choosing this tier should be honest about prior performance. If you did not hold a Bitcoin position through the 2022 drawdown without selling, your behavioural calibration may not yet support a 25% allocation. Most investors who can sustainably hold the aggressive tier got there gradually through balanced-tier holdings that grew with the asset, not through initial large lump-sum sizing.

Rebalancing mechanics

How you handle the position after the initial allocation matters at least as much as the starting size. A Bitcoin sleeve that drifts from 10% to 25% after a strong rally has effectively become a different portfolio — one with much higher volatility exposure than the investor originally chose. Whether you trim that gain or let it ride changes the outcome by an order of magnitude across multi-year horizons.

Two approaches fit retail portfolios. Calendar rebalancing — typically quarterly or annually — checks allocation drift on a fixed schedule and rebalances if drift exceeds a threshold. Threshold rebalancing checks drift continuously and rebalances when the position moves more than 5 or 10 percentage points from target. Threshold rebalancing tends to capture more value through volatility but produces more frequent taxable events and trading friction.

The deeper analysis of allocation tier selection, rebalancing mathematics, and Bitcoin's role inside specific portfolio structures sits in our dedicated portfolio allocation satellite. Investors comparing Bitcoin against gold or traditional store-of-value assets within an allocation framework will find the relative case in our Bitcoin vs gold comparison.

Entry Strategy: DCA vs Lump Sum

Once you have decided on allocation size, the next question is how to deploy it. Two structured approaches dominate retail practice. Dollar-cost averaging (DCA) spreads purchases across multiple periods. Lump-sum investing deploys the full allocation immediately.

Most investment research finds lump-sum investing produces higher average returns across long horizons because markets trend up more often than they trend down. Bitcoin partially breaks that pattern. Its drawdowns are deeper and its volatility is higher than traditional asset classes, which raises the regret cost of a poorly-timed lump-sum entry to a level where DCA mathematics often dominate.

Why DCA dominates for Bitcoin

Three factors push most retail Bitcoin investors towards DCA.

First, the wide volatility range means a single-day entry can be 30-50% from the average price across a six-month window. DCA averages out timing risk.

Second, behavioural research consistently finds investors hold positions better when they enter gradually. The psychological commitment of "I bought $7,500 of Bitcoin this morning" produces different decision-making than "I have been buying $625 of Bitcoin every month for the past 12 months and the position is now worth $7,500".

Third, DCA matches typical income cadence. Most retail investors deploy from monthly or quarterly disposable income, which mechanically produces a DCA structure regardless of intent.

When lump-sum makes sense

Lump-sum deployment fits specific scenarios. Investors with a windfall — inheritance, business sale, bonus — who can afford the full allocation comfortably and have sufficient existing holdings to absorb timing risk often find lump-sum produces better expected returns. Investors deploying a small amount relative to net worth can afford the regret cost of bad timing. Investors who have already held Bitcoin through a prior drawdown without selling have demonstrated the behavioural discipline that survives a poorly-timed lump-sum entry.

Most other investors are better served by a DCA programme spanning 6-12 months that captures most of the average-return benefit while protecting against worst-case entry timing.

Frequency and amount selection

Within a DCA programme, two parameters matter: how often to buy and how much.

Weekly purchases produce smoother averaging and capture more volatility benefit, at the cost of more transaction friction. Monthly purchases align with most salary cadences and produce 70-80% of the volatility benefit of weekly purchases. Quarterly is the minimum useful frequency.

The amount per purchase should reflect a stable percentage of disposable income rather than a fixed currency figure, so the programme survives income changes. A practical rule: pick a percentage you can sustain for 24 months without strain, run that, and adjust upwards only after demonstrated behavioural sustainability.

The execution detail — including step-by-step recurring-buy walkthroughs on the major exchanges, fee structure analysis, and the specific scenarios where lump-sum entry beats DCA — sits in our dedicated DCA playbook satellite. The general DCA framework that applies across cryptocurrencies sits in our DCA setup guide.

Custody Decision Framework

Custody is the area where retail investors have lost the most money in Bitcoin's history — not to market drawdowns, but to exchange collapses, withdrawal freezes, hot-wallet thefts, and irrecoverable seed-phrase loss. Mt. Gox in 2014, QuadrigaCX in 2019, FTX in 2022 and Celsius in the same window each demonstrated that custody quality matters more than market timing for long-term investor outcomes.

The good news: the custody decision tree is one of the simplest decisions in Bitcoin investing. It depends almost entirely on holding size.

The decision tree by holding size

For Bitcoin holdings below approximately $1,000 (£800) or three months of disposable income, whichever is lower, regulated exchange custody with two-factor authentication is acceptable. The inconvenience and learning curve of hardware wallet setup outweighs the marginal counterparty risk at small sizes.

Use a major regulated exchange — OKX, Coinbase or Kraken depending on jurisdiction. Enable Google Authenticator or a Yubikey for 2FA. Set a strong unique password. Enable withdrawal address whitelisting. This setup is enough for the first $1,000.

Above $1,000 (£800), hardware wallet self-custody becomes worth the setup cost. Hardware wallets store private keys offline in a dedicated device. They sign transactions inside the device without exposing keys to your computer. They provide multiple physical backups through seed-phrase recording.

Ledger and Tangem are the two products we recommend for first-time hardware wallet users. Both have demonstrated long track records, clear documentation, and price points below $200 (£160). The setup process takes 30-60 minutes the first time and produces a permanent storage system for any Bitcoin you choose to move there.

Above approximately $50,000 (£40,000) in Bitcoin, multi-signature setups become worth the additional complexity. Multi-sig requires multiple keys — typically 2-of-3 or 3-of-5 — to sign transactions, eliminating single points of failure. A theft of one device or one seed phrase no longer compromises funds. The setup is more involved than single-key hardware wallets, with implications for inheritance planning and key-custody distribution that take careful thought.

Most investors crossing the $50,000 threshold work through multi-sig configuration with established hardware wallet vendor documentation as a reference.

Hardware wallet selection

The two hardware wallets we recommend for first-time setup balance security, usability and price.

Ledger Nano S Plus and Nano X have the longest track record in the industry and the broadest software ecosystem. Ledger has matured significantly since the 2020 customer-data breach, with stronger operational practices and ongoing third-party security audits.

Tangem Wallet uses a card-based form factor with EAL6+ secure-element certification. The user experience is simpler for newcomers, and the device pairs to a smartphone via NFC. The trade-off is a smaller ecosystem and shorter track record than Ledger.

Both are appropriate for Bitcoin storage above the $1,000 threshold. The right choice depends on personal preference more than on objective security differences. The detailed comparison — including security architecture, supply chain considerations and side-by-side feature analysis — sits in our hardware wallet comparison.

Seed phrase storage

Hardware wallet security depends on seed-phrase storage as much as on the device itself. The 12 or 24 words generated during initial setup recover the wallet on any compatible device. Anyone who reads the seed phrase can steal the funds. Anyone who loses it cannot recover the wallet.

The standard practice in 2026 is metal seed-phrase storage products that survive fire, flood, corrosion and most physical disasters. Cryptosteel, Billfodl, Blockplate and SeedPlate are the established options in the $50-150 (£40-120) range.

Paper backups are deprecated for serious holdings. Paper degrades, ink fades, water destroys, and most retail seed-phrase losses come from inadequate physical storage rather than theft.

Inheritance and access planning

Long-term Bitcoin holders need a plan for what happens to the wallet if they cannot access it — through illness, accident, or death. The standard approaches range from simple to complex. Simple: sealed instructions in a safe accessible to a trusted family member. Complex: legal trust structures with custodian instructions.

The right approach depends on holding size, family situation and jurisdiction. The critical principle is that inheritance planning should happen before it is needed and should be reviewed at least annually.

Avoiding the most common mistakes

Three errors account for the majority of retail custody losses.

The first is leaving large holdings on exchanges past the point where exchange custody makes sense — typically driven by inertia rather than conscious decision.

The second is photographing or digitally storing seed phrases. "I'll just take a photo for backup" exposes the seed to malware, cloud-storage breaches and device theft.

The third is not testing the recovery process before relying on it. A hardware wallet you cannot recover from a fresh device using only the seed phrase is not actually backed up. Run a full recovery test on a wallet with a small balance before trusting the system with significant funds.

Tax Basics by Region

Bitcoin tax treatment varies meaningfully across jurisdictions. The wrapper structure you use affects after-tax returns more than most retail investors realise. The high-level framework below covers the major regions for our readership. None of this constitutes tax advice — verify with a qualified accountant familiar with cryptocurrency taxation in your jurisdiction, particularly for larger positions.

United States

The IRS treats Bitcoin as property. Disposals — sales, swaps to other crypto, payments for goods — trigger capital gains.

Short-term gains on positions held less than one year are taxed at ordinary income rates (10-37% federal). Long-term gains on positions held more than one year are taxed at preferential rates (0%, 15% or 20% federal depending on income band) plus state tax in most states.

The wash-sale rule that applies to stocks does not currently apply to Bitcoin. This allows tax-loss harvesting strategies that are not available with traditional securities.

Self-directed IRAs through specialised custodians can hold direct Bitcoin tax-deferred (Traditional IRA) or tax-free (Roth IRA), although the custodian fees often offset the wrapper benefit for smaller positions. Spot Bitcoin ETFs in standard brokerage IRAs receive standard ETF tax treatment, which is usually the simpler path.

European Union

Tax treatment varies materially by country under the broader MiCA regulatory framework that came into effect during 2024-2025.

Germany treats Bitcoin held more than 12 months as tax-free on disposal — one of the most favourable treatments globally — although the rule is subject to regular legislative review. France applies a flat 30% rate on most crypto disposals (single tax on capital income). Portugal moved from a tax-haven position to a 28% rate on disposals within one year of acquisition and 0% beyond, similar to Germany's structure but with different specifics.

The Netherlands treats Bitcoin under wealth-tax rules rather than capital-gains rules, with annual taxation on assumed returns. Spain, Italy and other major EU jurisdictions each have distinct rules. Verify with a local accountant for any meaningful position.

United Kingdom

HMRC treats Bitcoin disposals as capital gains. The annual capital-gains tax allowance for the 2026/27 tax year, currently set at £3,000, applies before the gain becomes taxable. Above the allowance, gains are taxed at 18% (basic-rate band) or 24% (higher and additional-rate bands), following the rate increase that took effect in October 2024.

Spot Bitcoin ETPs that have been approved for the UK retail market are eligible for ISA wrappers through brokers including Hargreaves Lansdown, IG, Trading 212 and AJ Bell. Holding Bitcoin exposure inside an ISA shelters gains from CGT and dividend tax, which can produce a meaningful long-term tax efficiency advantage relative to direct Bitcoin holdings outside any wrapper.

Direct Bitcoin holdings remain subject to CGT on disposal and to detailed transaction reporting requirements that have grown stricter over recent years.

Practical implications

The tax wrapper choice often outweighs the ETF-vs-direct choice in long-term return terms.

For US investors with tax-advantaged retirement accounts, ETFs in the IRA are usually the highest-after-tax-return path. For UK investors with ISA capacity, ISA-eligible Bitcoin ETPs can produce 20-30 percentage points of long-term return advantage relative to taxable direct holdings depending on tax band.

EU investors face the most country-specific decisions. In Germany, the one-year holding rule favours direct holdings. In France, the flat 30% applies to both. In the Netherlands, wealth-tax treatment changes the calculation entirely.

For positions large enough to matter, the few hundred pounds or dollars spent on a qualified tax accountant before structuring the position pays back many times over.

Risk Landscape 2026

The 2026 Bitcoin risk landscape differs from earlier eras in ways worth naming explicitly. Some traditional risks have softened. New risks have emerged from the institutionalisation of the asset.

Volatility risk

Bitcoin's volatility has compressed materially since the 2022 cycle bottom and the 2024 ETF approval. It remains structurally higher than traditional asset classes. Drawdowns of 40-50% remain plausible during macro shocks and sentiment shifts.

The 70-85% drawdowns characteristic of prior cycles are less likely in the post-ETF era because institutional holders smooth the order book — but "less likely" is not "impossible". Allocation sizing should assume a 50% drawdown is the realistic worst case from any entry point, with smaller drawdowns the more probable outcome.

ETF concentration risk

Spot ETF growth has produced concentration that did not exist in earlier cycles. A small number of large issuers — BlackRock's IBIT, Fidelity's FBTC, ARK's ARKB and a handful of others — collectively hold a meaningful share of liquid Bitcoin supply.

This has stabilised price during normal markets but creates a new tail risk. Coordinated outflows during macro stress could amplify downside moves rather than dampen them, in a way that Bitcoin has not previously experienced at this institutional scale. The risk is not that ETFs themselves fail — they are structurally simple — but that their flow patterns differ from retail-driven cycles in ways that remain to be observed through a full macro cycle.

Regulatory risk

Regulatory clarity has improved meaningfully since 2022. The US ETF approvals, the EU's MiCA framework, the UK's Financial Conduct Authority registration regime, and broadly stable regulatory positions across most major jurisdictions create a more predictable operating environment than existed during prior cycles.

Residual risk still exists despite mitigation. Jurisdictions could change tax treatment, restrict self-custody, or introduce new reporting requirements that affect cost or accessibility. The trend has been towards integration rather than restriction, but the pace and direction can shift with political cycles.

Custodial risk

Exchange and custodian failures remain the single largest historical source of retail Bitcoin losses. The 2022 collapses (FTX, Celsius, BlockFi, Voyager) cost retail investors billions of dollars in funds that survived market volatility but did not survive custodial failure.

The post-2022 environment has improved through proof-of-reserves audits, regulatory oversight and survival-of-the-fittest amongst exchanges. Risk is lower but not eliminated — significant Bitcoin holdings should sit in self-custody once the holding size justifies the setup cost, regardless of how reputable the exchange appears.

Macro liquidity risk

Bitcoin's correlation with global liquidity conditions has strengthened in the post-ETF era. Federal Reserve policy, dollar liquidity and yields on competing assets now affect Bitcoin price more directly than during earlier retail-driven cycles.

Periods of liquidity tightening — quantitative tightening cycles, rate hikes, dollar strength — tend to compress Bitcoin alongside other risk assets. This is not a structural problem with Bitcoin. It is the normal behaviour of an asset that has reached institutional scale. Investors should expect Bitcoin to behave more like a high-volatility macro asset than like the uncorrelated diversifier that some early-cycle commentary positioned it as.

Technology risk

Bitcoin's core protocol has operated without significant disruption since 2009. Tail risks remain real. A critical bug in core node software, a sustained 51% mining attack, or a regulatory crackdown on mining concentrated in particular jurisdictions could each produce disruption that no individual investor can hedge against.

The probability of any of these is low, and Bitcoin's track record provides reasonable confidence in core protocol stability. The technology risk worth paying attention to is closer to home: irrecoverable seed-phrase loss, hardware wallet supply-chain compromise, and software-wallet bugs are realistic operational risks that affect more retail investors than core-protocol failures ever will.

Common Framework Misuses

The framework above gives defensible answers to the five core decisions. But applying it correctly is harder than reading it. Four patterns produce most of the bad outcomes we see retail investors generate, even when they have read the right material.

Treating allocation tier as static

Most investors choose an allocation tier once and never revisit it. Your tier should evolve with your circumstances. Your income stability changes over time, and your wealth concentration changes alongside it. Time horizon shortens as you approach retirement. The 15% allocation that suited you at 35 with strong income probably does not suit you at 60 with a fixed-income lifestyle and a recent inheritance.

Review your allocation tier annually. Ask whether your current size still matches your current life situation, not the situation you were in when you first sized the position. Most allocation drift problems are not market-driven — they are life-driven, and the investor has not adjusted.

Confusing wrapper choice with ideology

The ETF-versus-direct decision often gets framed as a Bitcoin-purist debate. It is not actually a referendum on Bitcoin. It is an account-structure decision, and the ideological framing causes real damage in two directions.

On one side, investors with most of their wealth in retirement accounts refuse ETFs because "not your keys, not your coins" — and end up with no Bitcoin exposure at all because direct Bitcoin will not fit inside their 401(k). On the other side, investors with significant taxable wealth default to ETFs because they feel safer — and pay 0.20-0.25% per year in expense ratio for decades when direct ownership would have served them equally well.

The correct frame: ETF if your account structure benefits from it, direct if your account structure does not. Many investors hold both for the same reason most other investors hold a mix of asset classes — different parts of the portfolio serve different purposes.

Over-engineering custody for the holding size

The custody decision tree is simple. Investors who try to make it complicated either burden themselves with multi-sig setups for $5,000 holdings (where the operational complexity exceeds the security benefit) or stay on exchange custody for $200,000 holdings (where the counterparty risk dwarfs the convenience benefit).

Calibrate custody to actual holding size, not to perceived sophistication. A $3,000 Bitcoin holding on a regulated exchange with strong 2FA is fine. A $30,000 holding on a hardware wallet with metal seed-phrase backup is fine. A $300,000 holding in a properly-configured 2-of-3 multi-sig is fine. Mismatches in either direction produce worse outcomes than the simpler default would have.

Ignoring tax wrapper opportunity until disposal

The most common tax-related mistake is treating tax planning as something you do at sale time rather than at purchase time. Decisions made when you first allocate to Bitcoin — which wrapper, which jurisdiction-specific structure, what records to maintain — determine how much of the eventual gain you keep. Decisions made at sale time can only react to the structure you already created.

For a UK investor with ISA capacity, the difference between holding ISA-eligible Bitcoin ETPs inside the wrapper versus direct Bitcoin outside it can compound to 20-30 percentage points of after-tax return advantage over a decade. For a US investor, the choice between a Roth IRA holding ETFs versus a taxable brokerage account holding direct Bitcoin can produce similar magnitude differences. None of that is recoverable after the fact. The wrapper decision is the single highest-leverage decision in the framework, and most investors make it casually or not at all.

Practical Takeaways

Bitcoin investment in 2026 is a different exercise from Bitcoin investment in earlier cycles. The four-year halving model has weakened. ETF flows now dominate price discovery in ways that did not exist before January 2024. Volatility has compressed materially compared with prior cycles. Institutional holders concentrate a meaningful share of liquid supply. Tax wrappers in major jurisdictions allow Bitcoin exposure inside structures that would have been impractical or impossible five years ago.

Five practical principles consistently produce good outcomes across this changed landscape:

- Size your allocation to total wealth and behavioural tolerance, not to price predictions.

- Choose ETF or direct ownership based on account structure, not ideology.

- Deploy through dollar-cost averaging unless you have specific reasons to lump-sum.

- Secure holdings above the trivial threshold in hardware wallets with metal seed-phrase storage.

- Structure for the most favourable tax treatment your jurisdiction allows.

Each of these is controllable, while price is not — internalising that distinction is the difference between disciplined long-term Bitcoin investing and speculation dressed up in investment language.

What to do this week

If you are starting from scratch, work through the framework in order. Decide your target allocation tier. Choose between ETF and direct ownership based on whether your allocation lives in a tax wrapper. Set up a recurring buy through OKX, Coinbase or Kraken depending on your jurisdiction. Define the threshold at which you will move funds to a hardware wallet. Confirm the tax treatment you will apply with a qualified accountant if the position is meaningful. Most of these decisions take an evening to make and a weekend to execute, and once made they require minimal ongoing attention.

If you already hold Bitcoin, the framework still applies as a check. Is your allocation calibrated to your actual behavioural tolerance, or to the conviction you felt when you first entered? Is your custody appropriate for current holding size, or is exchange inertia keeping funds where they should not be? Is your tax wrapper choice still the most efficient given current jurisdiction rules? Honest answers to those three questions catch most allocation drift problems before they become consequential.

Calibration milestones

The framework is not a one-time setup. It is a structure to revisit at predictable points. Three milestones are worth scheduling:

- Annual review — once per year, assess whether your allocation tier still matches your current life situation. Income changes, wealth concentration changes, time horizon shortens, and your behavioural tolerance evolves through cycles. The right tier at age 35 with strong income is rarely the right tier at age 60 with a fixed-income lifestyle.

- Drawdown response review — after the next 30%+ Bitcoin drawdown, observe your own behaviour honestly. Did you hold without anxiety? Did you reach for the sell button? Did you actually sell? The answer calibrates your true tier rather than your assumed tier, and it is the most important data point you will collect about your own Bitcoin investing capacity.

- Wrapper opportunity review — when tax laws change in your jurisdiction or when new wrapper options become available, reassess whether your structure is still optimal. The wrapper decision compounds over decades, and small efficiency improvements made early produce large after-tax differences over a 20-year holding period.

The remaining sections of this cluster cover the execution detail. The cycle satellite analyses the post-halving shift in depth. The ETF satellite gives the full ETF-versus-direct decision matrix. The DCA playbook walks through recurring-buy setup on each major exchange. The allocation satellite goes deeper on portfolio construction with Bitcoin. The Bitcoin vs gold compare provides macro context for thinking about Bitcoin alongside traditional store-of-value assets. The Bitcoin review covers the asset itself in depth. Together they form a complete framework for the post-cycle era.

Sources

- Federal Reserve — macro liquidity context referenced in the cycle and risk sections

- U.S. Securities and Exchange Commission — spot Bitcoin ETF approval and ongoing oversight

- UK Financial Conduct Authority — UK regulatory framework for crypto exchanges and ISA-eligible products

- HM Revenue and Customs — UK Bitcoin tax treatment and capital gains framework

- Internal Revenue Service — US Bitcoin tax treatment as property and reporting requirements

- EUR-Lex — official source for the EU MiCA framework affecting Bitcoin treatment

- Bitcoin Cycle 2026: How ETF Flows Reshaped Halving Dynamics

- Spot Bitcoin ETF vs Direct BTC Decision Framework

- Bitcoin DCA Playbook: Setup, Frequency, Allocation

- Bitcoin Portfolio Allocation

- Bitcoin vs Gold Comparison

- Bitcoin Review: Investment Analysis

- What is Bitcoin? Technology and Investment

- Your First 30 Days on a Crypto Exchange

- Crypto vs Stocks: Asset-Class Comparison

Frequently Asked Questions

- Is the four-year halving cycle still useful in 2026?

- The halving still affects supply, but its market signal has weakened. Spot Bitcoin ETFs absorb more BTC in a typical week than miners produce in a month. Demand-side flows now drive price discovery more than the supply-side halving event. Treat the halving as one factor amongst several, not as a master timing model.

- How much Bitcoin should I hold in my portfolio?

- Three reasonable tiers exist for most investors. Conservative exposure sits at 1-5% of investable assets and behaves like a small alternatives sleeve. Balanced allocation runs 5-15% for investors who want meaningful upside without dominating the portfolio. Aggressive allocation of 15-30% suits investors with conviction, long horizons and tolerance for 50% drawdowns. The right tier depends on time horizon, income stability and behavioural tolerance, not on price predictions.

- Should I buy a Bitcoin ETF or direct Bitcoin?

- ETFs are simpler. They fit existing brokerage and retirement accounts and remove custody responsibility. Direct Bitcoin gives you self-custody control, no annual expense ratio, and the option to use BTC outside the financial system. Most retirement and tax-wrapper allocations work better through ETFs. Strategic conviction holdings often work better as direct ownership in a hardware wallet. Many investors hold both.

- Is dollar-cost averaging better than a single lump-sum purchase?

- Lump-sum investing has historically beaten DCA on average across most asset classes. Bitcoin is the exception when emotional volatility is factored in. DCA reduces regret risk after large drawdowns, smooths the entry price, and matches typical income cadence. For most retail investors, a 6-12 month DCA programme on Bitcoin captures most of the average-return upside while protecting against the worst entry timing.

- When do I need to move Bitcoin to a hardware wallet?

- A practical threshold is roughly $1,000 (£800) or three months of disposable income, whichever is lower. Below that, exchange custody with two-factor authentication is acceptable. Above that, hardware wallet self-custody removes counterparty risk that has historically caused the largest retail losses in crypto. Above $50,000, multi-signature setups become worth the additional complexity.

- How is Bitcoin taxed in the US, EU and UK?

- In the US, Bitcoin is taxed as property. Short-term gains are taxed as ordinary income; long-term gains at 0-20% federal rates. In the EU, treatment varies by country under the MiCA framework. Germany treats long-held Bitcoin as tax-free after one year. France applies a flat 30% rate on disposals. In the UK, HMRC treats Bitcoin disposals as capital gains, with rates of 18% or 24% depending on income band and an annual allowance of £3,000 for 2026/27. Always verify current thresholds with a qualified accountant.

- What are the main risks of holding Bitcoin in 2026?

- Volatility remains structural — drawdowns of 50% or more have occurred in every multi-year period. ETF concentration creates a new risk: a small group of large issuers now controls a meaningful share of liquid supply. Regulatory uncertainty exists in some jurisdictions. Custodial failures on exchanges have caused the largest historical retail losses. Macro liquidity tightening can compress prices independently of Bitcoin-specific news. Position size and custody quality manage these risks better than market timing.

- Should I sell Bitcoin during major drawdowns?

- If your allocation was correctly sized for your wealth and behavioural tolerance, the answer is almost always no. Investors who sell during 50%+ drawdowns and try to re-enter typically miss the recovery and end up worse off than buy-and-hold. The fact that a drawdown produces strong urge to sell usually indicates the position was sized too aggressively to begin with. The right response is to fix sizing on the next position, not to capitulate during the current drawdown. If selling feels imperative during a drawdown, sell only enough to bring allocation back to a sustainable size, not the entire position.

- How does Bitcoin fit alongside traditional retirement planning?

- Treat Bitcoin as one component of a broader retirement portfolio, not as a replacement for traditional asset classes. For most retail investors, a 5-10% Bitcoin allocation inside a tax-advantaged retirement wrapper produces meaningful upside without dominating retirement outcomes. Larger allocations require corresponding behavioural tolerance and longer time horizons. Investors within 10 years of retirement should generally cap Bitcoin allocation at 5% of total wealth. Investors with 20+ years to retirement can sustain higher allocations because time horizon absorbs drawdown risk.

- Is Bitcoin self-custody too complicated for non-technical investors?

- No, modern hardware wallets have made self-custody accessible to non-technical users. Tangem in particular targets first-time hardware wallet users with NFC-based pairing and simplified setup. Ledger offers a more feature-rich ecosystem that scales with sophistication. Both are appropriate for non-technical buyers above the $1,000 threshold. The actual complexity is not technical — it is procedural: backing up the seed phrase correctly, testing recovery, and avoiding common phishing patterns. The procedures take 30-60 minutes to learn once and protect funds for decades.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.