Bitcoin DCA Strategy Playbook 2026 Guide

Concrete recurring-buy execution on OKX, Coinbase and Kraken — with frequency selection logic, amount-sizing rules, and the specific scenarios where lump-sum entry beats DCA.

Introduction

Most Bitcoin DCA content tells you that dollar-cost averaging is a good idea and stops there. This playbook does the opposite. It assumes you have already decided to DCA and walks you through the execution.

The execution matters more than retail investors typically appreciate. The difference between a DCA programme that compounds reliably for a decade and one that breaks down within six months is rarely about the broader strategy — it is almost always about the specific configuration choices made at setup. Frequency, amount sizing, fee optimisation, withdrawal cadence and exchange selection each produce small differences in outcome that compound to meaningful ones over multi-year horizons.

We cover the setup, the frequency choice, the amount-sizing logic, the specific recurring-buy interfaces on the three exchanges that matter for our readership, and the scenarios where lump-sum entry beats DCA. By the end you should be able to set up a recurring Bitcoin purchase in under 30 minutes on whichever exchange fits your jurisdiction.

The structure is intentional. Each exchange walkthrough gives you the exact menu path, the configuration choices that matter, and the fee implications. The frequency and amount sections cover the trade-offs that are not obvious from the exchange UI itself. The "when not to DCA" section is honest about cases where lump-sum produces better expected outcomes — DCA is not the right answer for every investor every time.

One framing point before we start. DCA is a discipline, not a price strategy. It works because it removes timing decisions from the path of execution, not because it produces better mathematical returns than lump-sum on average. Most investment research finds lump-sum beats DCA across most asset classes when the investor can actually deploy the lump sum and hold through drawdowns. Bitcoin is the asset class where the behavioural advantages of DCA most often dominate the mathematical advantages of lump-sum, because Bitcoin's drawdowns are deep enough and emotionally taxing enough that retail investors consistently fail to hold lump-sum entries through them. DCA is the operational answer to that behavioural reality.

Geographic note: OKX is our default recommendation outside the US, with the most competitive combination of fees, recurring-buy interface and proof-of-reserves transparency. OKX does not serve US residents directly. US investors should skip ahead to the Coinbase Auto-Invest or Kraken DCA walkthroughs, both of which provide equivalent functionality through US-regulated venues. The frequency, amount and lump-sum sections apply equally regardless of which exchange you choose.

If you arrived from our Bitcoin investment fundamentals hub, this playbook gives you the execution depth on the entry strategy section. The general DCA framework that applies across cryptocurrencies sits in our DCA setup guide.

DCA Mechanics and Historical Performance

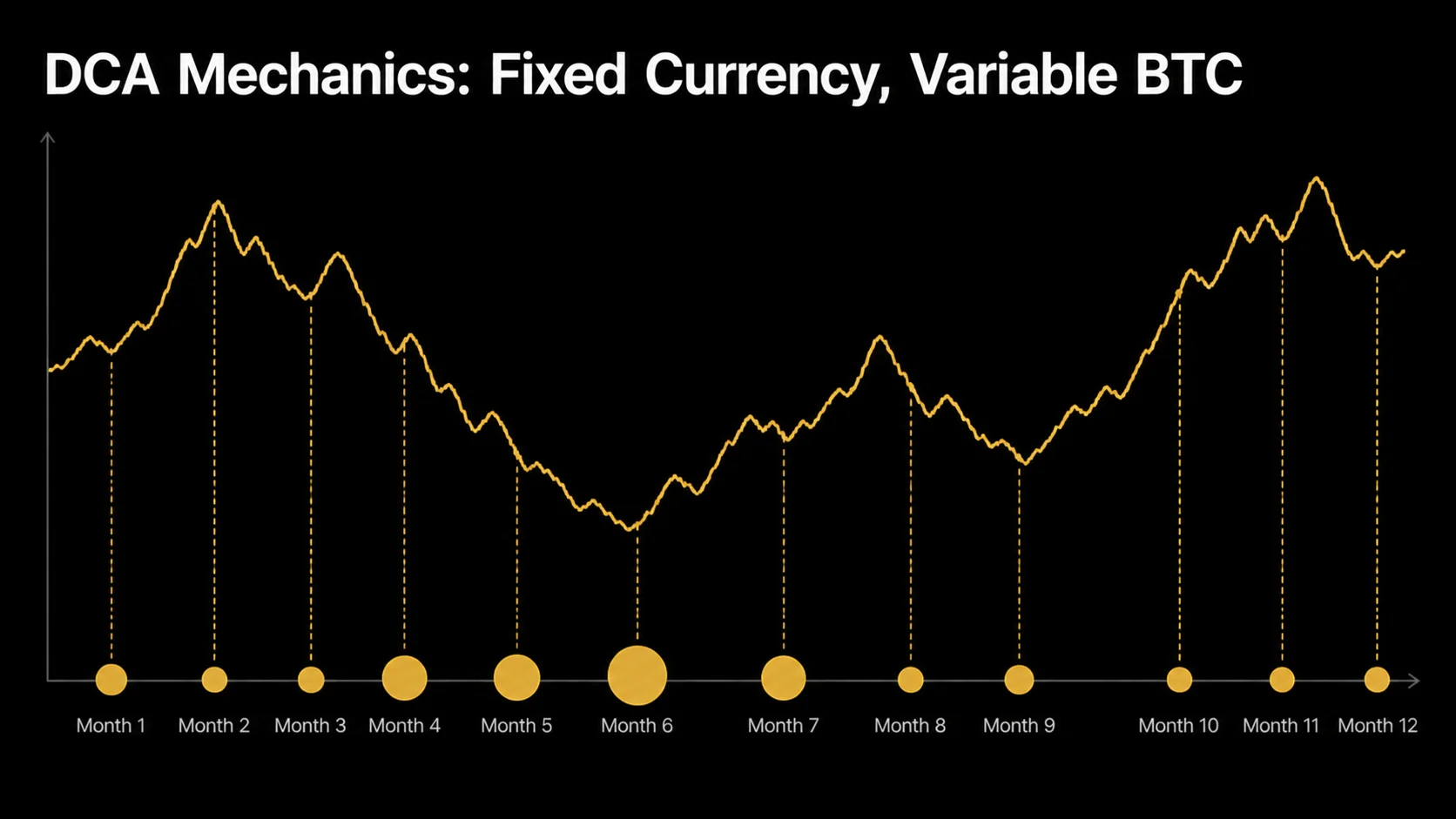

Dollar-cost averaging on Bitcoin works the same way it works on any other asset. You commit to buying a fixed currency amount on a recurring schedule, and you accept the resulting average purchase price rather than attempting to time individual entries.

The mathematics are straightforward. When prices are low, your fixed amount buys more Bitcoin. When prices are high, it buys less. Over a full market cycle, the average purchase price tends to land below the simple time-average of the price series — the source of the strategy's defensive properties.

The historical backtest

The standard reference figure for Bitcoin DCA performance is the long-running backtest of $100 per month from January 2014 through early 2026. A consistent $100/month allocation over that 12-year window resulted in total invested capital of approximately $14,600 with a portfolio value that peaked near $1,000,000 around Bitcoin's October 2025 all-time high and stood at roughly $600,000 to $650,000 by mid-2026 after a ~50% fall from that peak — still a cumulative return in the multi-thousand percent range, though the dollar figure moves directly with the live Bitcoin price.

Several caveats apply.

- The window covers a period of extraordinary Bitcoin appreciation that may not repeat.

- The starting point of January 2014 happened to be a relatively low entry against the subsequent multi-cycle rally.

- Any DCA window of similar length but with different start and end points produces different results.

The figure illustrates the principle of long-term DCA discipline rather than serving as a return projection. What it shows reliably is that consistent buying through multiple cycles outperforms most attempts at active timing amongst retail investors, even when the start and end dates are less flattering.

Why DCA works behaviourally

The behavioural advantage of DCA matters as much as the mathematical one. Investors who buy a single large position face the full emotional weight of any subsequent drawdown. A 50% drop on a $10,000 lump-sum purchase produces a visible $5,000 loss that often triggers selling at the bottom.

The same 50% drawdown on a position built through 24 months of $400 monthly purchases feels different. Most of the position was acquired below the peak. The average cost basis is lower. The emotional commitment of monthly contribution discipline tends to sustain through the drawdown.

Behavioural research consistently finds that DCA investors hold positions through volatility better than lump-sum investors do. That often matters more for long-term outcomes than the small expected-return difference.

Why DCA works mechanically

The mechanical advantage comes from the volatility geometry of buying. A fixed dollar amount mechanically buys more units when price is low and fewer when price is high, which produces an average purchase price below the simple time-average for any volatile asset with mean-reverting properties.

Bitcoin's volatility has been higher than most asset classes throughout its history, which amplifies the DCA mechanical benefit. Even with the volatility compression of the post-ETF era, Bitcoin's intra-cycle volatility remains high enough for DCA to capture meaningful averaging benefit relative to single-point entries.

Setup Walkthrough: OKX Recurring Buy

OKX offers automated Bitcoin recurring purchases through its dedicated DCA Bot (formerly named "Recurring Buy" in the standard interface). The setup takes 5-10 minutes once your account is funded and produces a fully-automated programme that runs without further intervention.

OKX is our default recommendation outside the US for several reasons:

- Low fees on BTC pairs (typically 0.08-0.10% spot fees, often lower with promotional discounts)

- Deep liquidity with consistent execution

- Proof-of-reserves audits published quarterly

- Recurring-buy interface that handles weekly and monthly cadences cleanly

Prerequisites

Before setting up the OKX recurring buy:

- OKX account with KYC verification at level 1 or higher

- Funded fiat balance via bank transfer (SEPA in the EU, Faster Payments in the UK, ACH equivalents elsewhere) or via the OKX P2P market for jurisdictions where fiat on-ramps are limited

- Two-factor authentication enabled (authenticator app, not SMS)

Setup steps

Navigate from the OKX main interface to Trade → Trading Bots → DCA Bot on desktop, or Discover → Trading Bots → DCA on mobile. Then:

- Select Bitcoin (BTC) as the target asset

- Select your funding currency (USDT, USDC, EUR, GBP or local fiat depending on availability) as the source

- Choose your frequency (daily, weekly or monthly)

- Set the purchase amount per period and start time

- Confirm — the bot begins executing on the schedule

You can pause, resume or modify the bot at any time from the same interface.

Fee structure

OKX charges standard spot trading fees on each recurring purchase — typically 0.08-0.10% for the maker/taker rate, with discounts available for OKB token holders and high-volume tiers. There is no separate recurring-buy fee on top of the base spot fee.

Concrete example: a $250 monthly purchase incurs a typical fee of $0.20-0.25 per transaction, or approximately $3 per year on a $3,000 annual programme. This is materially lower than most retail credit-card crypto purchase services and competitive with dedicated DCA platforms.

Important configuration choices

Three configuration choices matter:

- Funding currency: USDT or USDC produces the lowest spread on the BTC pair compared with direct fiat purchases — saving 0.1-0.3% per transaction. The trade-off is an extra step (convert fiat to USDT/USDC first). For most retail investors the simpler fiat-to-BTC path is acceptable.

- Start time: aligning the recurring buy to the day after your salary deposit avoids timing dependence on month-end exchange flows.

- Withdrawal cadence: decide whether OKX will hold the accumulated BTC indefinitely or whether you will move it to self-custody on a schedule. For positions accumulating beyond approximately $1,000 (£800), set a recurring monthly or quarterly withdrawal to a hardware wallet address rather than letting the balance sit on the exchange. This converts the DCA programme into self-custody accumulation rather than exchange custody accumulation.

Setup Walkthrough: Coinbase Auto-Invest

Coinbase Auto-Invest is the standard recurring-buy interface for US Bitcoin DCA. The setup is more polished than most competitors and integrates cleanly with US bank accounts via ACH transfer.

Coinbase is publicly traded in the US and operates under federal and state regulatory oversight. Coinbase UK Limited is FCA-registered for UK customers, with a separate entity providing services to EU customers. This regulatory profile makes Coinbase the standard choice for US-resident DCA programmes that cannot use OKX, and a credible alternative for UK and EU investors who prefer a US-listed counterparty.

Prerequisites

- Coinbase account with identity verification (basic KYC requires government-issued ID and a selfie liveness check; advanced verification adds proof of address for higher limits)

- Linked US bank account via Plaid integration or routing/account number entry (ACH transfers are free; debit-card purchases incur higher fees and are not recommended for DCA)

- Two-factor authentication via authenticator app (not SMS)

Setup steps

From the Coinbase web or mobile interface, navigate to Trade → Buy → Auto-Invest. Then:

- Select Bitcoin (BTC) as the target asset

- Choose your linked bank account as the funding source

- Set your purchase amount and frequency (daily, weekly, every two weeks, or monthly)

- Review the displayed estimated fee for each purchase before confirming

- Confirm — the schedule activates from the next available execution date

Modify, pause or cancel from Profile → Auto-Invest at any time.

Fee structure

Coinbase fees on the standard interface are higher than OKX or Kraken but lower on the Coinbase Advanced (formerly Coinbase Pro) interface.

Standard Auto-Invest fees vary by payment method and amount, typically running 1-2% on small transactions and decreasing on larger amounts. For Coinbase customers running serious DCA programmes, switching to Coinbase Advanced for the recurring buys reduces fees to 0.0-0.6% maker/taker — materially closer to OKX and Kraken levels. The Advanced interface requires a separate setup but uses the same Coinbase account and funding sources.

Coinbase One subscription

Coinbase One ($29.99/month at time of writing) waives most trading fees on Coinbase, which can produce material savings for active DCA programmes above approximately $200/month. Breakeven depends on transaction frequency and amount. For a $500/month DCA programme, the subscription typically pays for itself within a few months. For smaller programmes the standard fee structure is more economical.

UK and EU notes

UK Coinbase customers operate under Coinbase UK Limited, FCA-registered, with bank deposits via Faster Payments rather than ACH. The Auto-Invest mechanism is the same. UK customers seeking ISA-eligible Bitcoin exposure cannot use Coinbase Auto-Invest directly — ISA Bitcoin exposure is delivered through approved Bitcoin ETPs held in ISA-eligible brokerage accounts (Hargreaves Lansdown, IG, Trading 212, AJ Bell), not through direct exchange purchases. EU Coinbase customers operate under the Coinbase Europe entity, with SEPA bank transfers replacing ACH.

Setup Walkthrough: Kraken DCA

Kraken offers Bitcoin DCA through its Recurring Buy feature, available on both the standard Kraken interface and the more advanced Kraken Pro.

Kraken is one of the longest-operating crypto exchanges (founded 2011), holds regulatory licences in the US and across multiple jurisdictions, publishes proof-of-reserves audits, and has never experienced a major security incident affecting customer funds. For US investors who prefer Kraken's lower fees over Coinbase's polish, or for non-US investors who prefer Kraken's regulatory profile over OKX, Kraken is a strong DCA venue.

Prerequisites

- Kraken account with identity verification (Starter, Express, Intermediate or Pro tier — Intermediate is the standard tier for serious DCA programmes)

- Funded account via ACH transfer, wire transfer or FedNow (US users), or via SEPA, Faster Payments or local equivalents (non-US)

- Two-factor authentication enabled (mandatory for serious account features)

Setup steps

From the Kraken web interface, navigate to Funding → Buy Crypto → Recurring Buy. Then:

- Select Bitcoin (XBT in Kraken's interface, equivalent to BTC) as the target asset

- Choose your funding currency as the source

- Set your purchase amount and frequency (daily, weekly, bi-weekly or monthly)

- Confirm — the schedule activates immediately

Modify or cancel from the Recurring Buy management page. Kraken Pro users have access to similar functionality through the advanced interface with lower fees on the underlying transactions.

Fee structure

Kraken Recurring Buy on the standard interface charges a 1.5% fee on each transaction, similar to Coinbase standard. Kraken Pro fees are 0.16-0.26% maker/taker on spot trades — materially lower.

For DCA programmes above approximately $500/month, executing through Kraken Pro produces meaningful annual savings at the cost of slightly more operational complexity. Kraken has periodically run promotions waiving Recurring Buy fees on specific assets including Bitcoin, which can make the standard interface competitive when active.

Kraken Pro recurring orders

For investors prioritising lowest fees, Kraken Pro supports automated recurring orders through its order-management interface. The setup is more involved than the standard Recurring Buy and requires understanding of limit and market order types, but produces fees in the 0.0-0.26% range that approach OKX levels. This path is appropriate for investors comfortable with the Pro interface and running DCA programmes large enough to justify the fee optimisation.

Frequency Selection: Weekly vs Monthly

The frequency choice in a DCA programme affects three dimensions: averaging quality, transaction friction and behavioural alignment with income cadence. The differences between common frequencies are smaller than most investors assume — within reasonable bounds, the consistency of execution matters more than the precise frequency.

Daily DCA

Daily DCA produces the smoothest averaging mathematically but has practical drawbacks. Each purchase incurs a transaction (with associated fees), which adds up to 365 transactions per year.

On exchanges with per-transaction fees this can erode returns. On exchanges with flat fee structures it is approximately neutral. Daily cadence also produces 365 individual cost-basis records, which complicates tax reporting in jurisdictions where each disposal must be matched against specific acquisitions. For most retail investors, daily DCA is unnecessarily granular relative to weekly or monthly.

Weekly DCA

Weekly DCA captures most of the volatility-smoothing benefit of daily cadence with materially lower transaction count (52 per year) and simpler tax reporting.

The standard practice is choosing a fixed weekday and committing to that day. Monday after weekend volatility settles works well, as does Friday before weekend uncertainty. Weekly aligns with bi-weekly salary cadences in jurisdictions where that is common, allowing automatic transfer of fixed amounts from each pay cheque into the recurring buy. Weekly is the recommended cadence for most retail DCA programmes that have low transaction fees.

Monthly DCA

Monthly DCA captures approximately 70-80% of the volatility-smoothing benefit of weekly cadence with materially lower transaction count (12 per year) and simpler operational tracking.

Monthly aligns with most salary cadences and is the most common DCA frequency amongst retail investors. The trade-off is reduced sensitivity to short-term volatility — a weekly programme that catches a mid-month dip captures more averaging benefit than a monthly programme that buys at month-end regardless of price action. For most investors, the simpler operational profile makes monthly the correct choice.

Quarterly DCA

Quarterly DCA is the minimum useful frequency for capturing volatility-smoothing benefit. Below quarterly, the strategy starts to look more like four annual lump-sum purchases than DCA, with corresponding behavioural and mathematical disadvantages. Quarterly works for investors with quarterly bonus structures or other quarterly income components, but is otherwise rarely the optimal choice.

The practical recommendation

Choose monthly DCA aligned to the day after your primary income deposit unless you have specific reasons to prefer weekly. Monthly captures most of the mathematical benefit, aligns with most salary cadences, simplifies operational tracking and tax reporting, and produces a behavioural rhythm that most investors sustain better than higher-frequency alternatives. If transaction fees on your chosen exchange are genuinely zero on recurring buys, weekly is a defensible upgrade.

Amount Selection: Percentage vs Fixed

The amount-per-purchase decision interacts with overall portfolio sizing in ways that are often underappreciated. The right amount depends on target allocation, time-to-target, income stability and operational sustainability. Two framing approaches dominate retail DCA practice.

Fixed currency amount

The simplest approach commits to a fixed currency figure per recurring purchase — $300/month, £200/month, €250/month. The figure is chosen based on disposable income at programme start and held constant unless deliberately revised.

Fixed amounts are easy to set up, easy to track, and easy to sustain mechanically. The drawback is that the figure does not adjust with income changes — a salary increase 18 months into the programme does not automatically increase the contribution unless you explicitly revise the schedule.

Percentage of disposable income

The percentage approach commits to a fixed share of disposable income — 5%, 10%, 15% — and recalculates the absolute figure with each income change. Percentage targets scale automatically with salary growth and adjust downwards during income shocks.

The drawback is operational. Most exchange recurring-buy interfaces require a fixed currency input, which means the percentage must be translated to a currency amount and revised manually when income changes.

The hybrid approach

Most sustainable DCA programmes follow a hybrid pattern:

- Choose a fixed currency amount that represents a sustainable percentage of current disposable income (typically 5-10%)

- Set the recurring buy to that amount

- Review annually — typically aligned to tax-year boundaries or salary review dates

- Adjust the fixed amount upwards or downwards to maintain the target percentage

This captures the percentage-approach benefit of scaling with income while preserving the operational simplicity of a fixed exchange configuration.

The 24-month sustainability test

Whatever amount you choose, apply the 24-month sustainability test before committing. Would this contribution be sustainable for 24 consecutive months even through income reductions, unexpected expenses, or temporary job loss?

If the answer is no, the amount is too high regardless of how attractive the upside looks. The behavioural cost of pausing or terminating a DCA programme during a Bitcoin drawdown often exceeds the benefit of starting at a higher amount. Smaller amounts sustained through full cycles outperform larger amounts that get paused at bottoms.

Scaling up over time

The cleanest scaling pattern starts with a sustainable amount and increases it after demonstrated behavioural sustainability — typically after the programme has run through at least one Bitcoin drawdown of 30% or more without pause.

Investors who get through a drawdown with the schedule intact have demonstrated the discipline to handle a larger amount safely. Investors who pause or panic at the first drawdown should consider that information when deciding whether to resume at the original amount or at a smaller one.

Execution Scenarios: How DCA Plays Out in Practice

The abstract DCA logic is straightforward. The interesting question for most investors is what the discipline actually produces across realistic market conditions. Three execution scenarios illustrate the typical pattern.

Scenario 1: Steadily rising market

Imagine you start a $500/month DCA programme on Bitcoin in January, with Bitcoin at $40,000. By December, Bitcoin reaches $80,000. What happens to your average cost?

Each month, your $500 buys progressively less Bitcoin as price rises. In January you accumulate 0.0125 BTC at $40,000; by December you accumulate 0.00625 BTC at $80,000. Across the twelve months, you have invested $6,000 and accumulated approximately 0.105 BTC — an average cost basis of approximately $57,000 per BTC. Lump-sum entry at January's $40,000 would have produced 0.15 BTC for the same $6,000 — better than DCA in this rising scenario.

Should you regret the DCA approach in this case? No. You would have needed perfect foresight to know January was the local low. The DCA programme produced a reasonable outcome without that foresight. The lump-sum case looks better in hindsight, which is exactly the kind of judgement that produces panic selling during the next drawdown.

Scenario 2: Volatile sideways market

Now imagine Bitcoin is $60,000 in January, drops to $35,000 in March, recovers to $55,000 in June, drops to $40,000 in September, and ends December at $50,000 — a typical volatile but ultimately flat year.

Your $500/month DCA programme accumulates more Bitcoin during the drops (when each $500 buys more BTC) and less during the highs. Across the year you accumulate approximately 0.135 BTC for $6,000 invested — an average cost of approximately $44,400 per BTC. Lump-sum at January's $60,000 would have produced just 0.10 BTC for the same money — DCA outperforms by approximately 35% on quantity accumulated.

This is where DCA mathematically shines. Volatile sideways markets reward the discipline because the strategy buys more when prices are low and less when they are high, mechanically tilting the average cost downwards.

Scenario 3: The drawdown-and-recovery cycle

Most consequentially, consider a year where Bitcoin opens at $70,000, declines to $30,000 mid-year, and ends at $80,000 — a complete cycle within the holding period. What happens to your DCA?

Your monthly purchases at $30,000 in the middle of the year produce more than double the Bitcoin per dollar than your purchases at $70,000 or $80,000 at the boundaries. Across twelve months your average cost lands somewhere in the $45,000-50,000 range. By year-end at $80,000, your accumulated position is meaningfully in the green even though parts of the year felt unproductive.

The pattern is the most important one for retail investors to internalise. Bitcoin produces drawdown-and-recovery cycles regularly. Investors who maintain DCA discipline through the trough end up with substantially better cost bases than those who pause when prices fall and resume when they recover. The behavioural temptation runs exactly opposite to the optimal action.

What these scenarios mean for your setup

The execution scenarios reinforce three operational priorities. First, choose a DCA amount you can sustain through the trough phase of any cycle, not just the comfortable phases. If $500/month feels easy at current prices but would feel unsustainable during a 60% Bitcoin drawdown, $500 is too high. Second, set your recurring-buy date and forget it — checking the price the day before each purchase invites timing manipulation that undermines the discipline. Third, track only the cumulative Bitcoin accumulated, not the unrealised P&L on each individual purchase. Position-by-position P&L tracking creates anxiety that pure quantity tracking does not.

If Your DCA Programme Has Paused: How to Recover

Most retail DCA programmes break at some point. Income changes, market drawdowns, life events, or simply forgetting to top up the funding account all produce gaps in the schedule. The question is not whether your DCA will pause — it is whether you can resume it well when it does.

Diagnose the cause honestly

Pauses fall into three categories, and the recovery path depends on which one you are facing:

- Operational pause — funding account ran low, payment failed, exchange account got temporarily restricted. The programme itself is still appropriate; you just need to fix the operational issue and resume.

- Financial pause — your income dropped, an expense came up, or your overall financial situation changed. The original DCA amount is no longer sustainable, but a smaller amount might be.

- Behavioural pause — you stopped because Bitcoin dropped and the discipline felt wrong, or because Bitcoin rallied and you decided to wait for a better entry. The programme is still appropriate; you stopped for emotional reasons that the discipline was meant to override.

The diagnosis matters because the fix differs. Operational pauses get resolved by fixing the operational issue. Financial pauses get resolved by lowering the amount to something sustainable. Behavioural pauses get resolved by acknowledging the failure of discipline and resuming at the original amount, with the understanding that next time the same temptation will appear and you will need to act differently.

Resume rules of thumb

Three rules cover most resume scenarios:

- Resume immediately, not "when the time is right" — waiting for an ideal entry price has the same problems as initial timing attempts. The longer you delay resumption, the more likely the programme dies permanently.

- Restart at sustainable amount, not original ambition — if the original $500/month proved unsustainable through the pause, restarting at $300/month and maintaining discipline beats restarting at $500/month and pausing again within months.

- Skip the missed contributions — do not try to "make up" missed months by deploying lump sums to catch up. The lump-sum-style catch-up reintroduces timing risk that the DCA discipline was meant to remove. Just resume the recurring schedule from today.

The honest answer about DCA programmes is that consistency through 5-10 years is rare, and most investors who claim long-running DCA programmes have actually paused multiple times. What separates investors who end up with strong Bitcoin positions from those who don't is not perfect execution — it is recovery from imperfect execution. The discipline you should aim for is the ability to resume after a pause, not the impossible standard of never pausing.

Tracking your DCA programme without checking prices

The most counterintuitive operational suggestion for DCA discipline is to deliberately avoid checking Bitcoin's price between purchase dates. Daily price-checking produces emotional pressure that undermines the discipline the schedule was meant to enforce. The investor who checks prices daily is significantly more likely to pause during drawdowns than the investor who checks monthly or quarterly.

What should you track instead? Three operational metrics matter:

- Cumulative Bitcoin accumulated — your total BTC balance after each purchase. This metric grows monotonically as long as you continue accumulating and resist selling. The shape of accumulation curve over time tells you the story of your discipline more honestly than P&L charts ever will.

- Average cost basis — your dollar-weighted average purchase price. This figure moves slowly and reflects the value DCA actually produces. Track it quarterly rather than after each purchase.

- Funding source consistency — confirm that the recurring buy is executing on schedule and that your funding source is reliable. Failed payments due to bank-side rejections happen occasionally and need addressing within the same week.

None of these metrics require checking Bitcoin's current price. They focus your attention on the parts of the DCA programme you actually control — execution and accumulation — rather than the parts you do not control, which is price.

Annual review process

Once per year, sit down with your DCA programme and answer four questions. Is the contribution amount still sustainable for your current income? Does your accumulated Bitcoin position still fit your overall allocation framework? Has your hardware wallet workflow been tested for recovery in the past 12 months? Have you encountered any phishing attempts or operational issues that suggest tightening security?

These four questions take 30 minutes to answer and protect against the slow drift that breaks DCA programmes over multi-year horizons. Most investors who abandon DCA do so not because of any single bad experience but because cumulative small frictions made the programme feel unsustainable. The annual review catches the frictions before they compound.

Funding source resilience and operational redundancy

Long-running DCA programmes occasionally encounter funding interruptions completely unrelated to investor preferences — banking provider switches funding policies, exchange counterparty modifies recurring purchase availability, automated payment processor experiences technical incidents preventing scheduled execution, regional banking regulations shift particular relationships unexpectedly. Investors maintaining single dependency between bank account and exchange account therefore face programme interruption when either dependency experiences disruption.

Defensible operational practice introduces minor redundancy across funding mechanisms. Maintain backup payment relationships covering primary exchange — secondary banking relationship enabling alternative funding channel, additional regulated exchange supporting comparable purchase functionality, occasional manual purchases providing operational familiarity outside automated workflows. Investors implementing redundancy specifically gain ability to maintain accumulation discipline through specific operational disruptions affecting primary funding channels, recovering original cadence within several days rather than experiencing extended programme interruptions during periods banking infrastructure unexpectedly proves unreliable.

When NOT to DCA: Lump-Sum Scenarios

DCA is the right answer for most retail Bitcoin investors most of the time. It is not the right answer for everyone in every scenario. A small set of conditions favour lump-sum deployment, and recognising them prevents over-application of the DCA framework where it is not optimal.

Windfall scenarios

Investors deploying a windfall — inheritance, business sale proceeds, signing bonus — face a genuine lump-sum-versus-DCA decision rather than a choice between DCA and waiting.

The classic finance literature finds lump-sum investing produces higher expected returns than DCA across most asset classes when measured over long horizons because markets trend up more often than they trend down. Bitcoin partially breaks that pattern through its higher volatility, but the fundamental dynamic still applies. For windfall scenarios, deploying immediately with a smaller initial allocation (say 50% on day one) followed by a 6-12 month DCA programme for the remainder captures most of the lump-sum benefit while protecting against worst-case timing.

Small allocations relative to total wealth

An allocation that is small enough not to materially affect the household balance sheet does not benefit from DCA risk management.

A $1,250 (£1,000) Bitcoin position in a $625,000 (£500,000) portfolio is 0.2% of total wealth. A 50% drawdown on that position costs roughly $625 — most retail investors can absorb that behaviourally without forced selling. For small allocations, the operational simplicity of a single lump-sum purchase outweighs the regret-risk reduction that DCA provides.

Demonstrated discipline through prior drawdowns

Investors who have previously held Bitcoin through a 50%+ drawdown without selling have demonstrated behavioural calibration that survives poorly-timed lump-sum entries. The risk DCA primarily mitigates — selling at the bottom after a poorly-timed entry — is largely absent in investors with that track record. For experienced Bitcoin holders adding to existing positions, lump-sum deployment is often the more efficient choice.

Time-pressured deployment

Specific tax or regulatory scenarios sometimes favour faster deployment than DCA naturally provides:

- Capital gains events that need offsetting in the current tax year

- ISA or IRA contribution windows that close on specific dates

- Regulatory changes that may restrict future access

These are edge cases for most retail investors but matter for the cases where they apply.

The hybrid decision

For investors uncertain between lump-sum and DCA, a 50/50 hybrid often produces the best risk-adjusted outcome. Deploy 50% of the intended position immediately and DCA the remaining 50% over 6-12 months. The structure captures most of the lump-sum expected-return benefit while providing meaningful protection against worst-case entry timing. For most windfall scenarios, this is the recommended approach.

Conclusion

Bitcoin DCA execution has become straightforward in 2026. Each of the three major venues — OKX outside the US, Coinbase and Kraken for US investors — provides recurring-buy automation that requires 5-10 minutes to set up and runs without further intervention.

The frequency choice (weekly or monthly), amount-sizing logic (percentage of disposable income translated to a sustainable fixed amount), and the small set of scenarios where lump-sum deployment makes more sense than DCA are the parameters that matter. Within those parameters, consistency of execution outweighs precision of configuration.

Common DCA pitfalls to avoid

Five patterns produce most of the DCA-programme failures we see retail investors generate, even after correct initial setup:

- Stopping during drawdowns — the moment when DCA mathematically does the most work is precisely when emotional pressure to stop is strongest. Investors who pause DCA during 50%+ drawdowns and resume "when conditions improve" capture less of the volatility-smoothing benefit than the discipline is designed to deliver.

- Increasing amounts during euphoria — the mirror image of the previous mistake. Investors who increase DCA amounts during strong rallies end up overweighting purchases at high prices, exactly the opposite of what disciplined DCA is meant to achieve.

- Letting accumulated Bitcoin sit on the exchange indefinitely — DCA is accumulation; self-custody is preservation. Investors who run DCA programmes for years without ever moving funds to hardware wallets eventually accumulate exchange custody risk that dwarfs the DCA programme's protective benefit.

- Optimising fees at the cost of execution — switching exchanges or rebuilding the recurring-buy setup to save 0.2% in fees, when the operational disruption to discipline costs more than the fee saving over a multi-year programme.

- Treating DCA as price prediction — DCA is not a bet that prices will recover. Investors who internalise it as a "buy the dip" strategy and stop buying when prices rise misunderstand the mechanism. DCA works because it removes prediction from the path of execution, not because it produces prediction itself.

Once your DCA programme is running

The next operational decision is custody. Bitcoin accumulating on an exchange becomes a custody risk past approximately $1,000 in holdings. At that point, the standard practice is moving accumulated Bitcoin to a hardware wallet on a periodic basis — typically quarterly or whenever holdings exceed a threshold.

The portfolio sizing framework that determines your overall allocation target sits in our portfolio allocation guide. The full Bitcoin investment framework that places DCA in context sits in our Bitcoin investment fundamentals hub.

Sources

- UK Financial Conduct Authority — registration framework for crypto exchanges operating in the UK

- U.S. Securities and Exchange Commission — US oversight of cryptocurrency exchanges

- Kraken — Recurring Buy and Kraken Pro documentation

- Coinbase Learn — Auto-Invest setup documentation and DCA strategy primer

- Bitcoin Investment Fundamentals: Post-Cycle Strategy Guide

- Bitcoin Portfolio Allocation

- Spot Bitcoin ETF vs Direct BTC

- DCA Crypto Strategy Setup Guide

- Your First 30 Days on a Crypto Exchange

Frequently Asked Questions

- What is dollar-cost averaging for Bitcoin?

- Dollar-cost averaging (DCA) means buying a fixed currency amount of Bitcoin on a recurring schedule regardless of price. Instead of attempting to time market entries, you commit to buying $100, £200 or another fixed amount every week or month and let market fluctuations average out over time. The strategy reduces regret risk after large drawdowns, smooths the entry price across market noise, and matches typical income cadence for retail investors.

- Should I DCA weekly or monthly?

- Monthly DCA captures approximately 70-80% of the volatility-smoothing benefit of weekly DCA at lower transaction friction. Weekly is preferable when fees are minimal and when you prefer smoother averaging. Monthly aligns with typical salary cadence and minimises transaction count. Quarterly is the minimum useful frequency. The choice between weekly and monthly is largely a matter of operational preference within a similar return profile.

- How much should I DCA into Bitcoin per month?

- Pick a percentage of disposable income you can sustain for 24 months without strain rather than a fixed currency amount. A common starting point is 5-10% of monthly disposable income. The position size matters more than the per-purchase amount. Your final allocation should match your portfolio target — typically 1-5% conservative, 5-15% balanced, or 15-30% aggressive of total investable assets. DCA continues until you reach the target allocation, then rebalances around it.

- When does lump-sum investing beat DCA for Bitcoin?

- Lump-sum investing has higher expected returns than DCA across most asset classes when measured over long horizons because markets trend up more often than they trend down. The exception for Bitcoin specifically is behavioural: a poorly-timed lump-sum entry into a 50%+ drawdown produces emotional pressure that often leads to selling at the bottom. Lump-sum makes sense when you have prior demonstrated discipline through Bitcoin drawdowns, when the position size is small relative to total wealth, or when you have a windfall that can be deployed without affecting cash-flow stability.

- Which exchange is best for Bitcoin DCA?

- OKX offers the lowest combination of fees and friction for Bitcoin DCA outside the US, with built-in recurring-buy automation, low spread on BTC pairs and proof-of-reserves audits. For US investors, Coinbase Auto-Invest and Kraken DCA are the standard options. Coinbase has the most polished UX for first-time DCA setup. Kraken has lower fees on advanced order types. The choice often comes down to jurisdiction (OKX does not serve the US directly) and operational preference rather than significant return differences.