DeFi Lending Complete Guide

What is DeFi Lending and Why It Matters

DeFi lending is a system where users lend and borrow cryptocurrency directly through smart contracts on blockchain networks — without banks, brokers, or intermediaries. Lenders deposit assets into protocol-managed pools and earn interest (typically 3–12% APY on stablecoins); borrowers post crypto collateral and draw loans against it. The two largest protocols, Aave ($8–10B TVL) and Compound ($2–3B TVL), operate on Ethereum and process billions in loans with no human approval process.

The collapse of centralised lending platforms in 2022 (Celsius, BlockFi, Voyager — collectively freezing $10B+ in customer funds) drove a structural shift towards DeFi lending. Unlike CeFi platforms where a company controls user deposits, DeFi protocols are governed by auditable smart contracts: collateral ratios are enforced algorithmically, interest rates adjust in real time based on supply and demand, and users retain custody of their assets until they actively deposit into a lending pool.

The promise is compelling: lend your cryptocurrency and earn interest rates that often exceed 5-10% annually on stablecoins, or borrow against your crypto holdings without selling them. But with this opportunity comes responsibility. DeFi lending requires understanding technical concepts like collateralisation ratios, liquidation thresholds, and smart contract risks.

The evolution of DeFi lending has been remarkable. What started as experimental protocols in 2018-2019 has grown into a multi-billion-dollar industry. The 2022 collapse of centralised lending platforms like Celsius, BlockFi, and Voyager—which froze billions in customer funds—served as a watershed moment. These failures highlighted the critical importance of self-custody and transparent, auditable systems. Users who had their funds locked in centralised platforms learnt a painful lesson: "not your keys, not your crypto" isn't just a slogan—it's a fundamental principle of cryptocurrency.

In contrast, DeFi lending protocols continued operating throughout the 2022 crisis. Users maintained full control over their assets, could withdraw at any time (subject to liquidity constraints), and benefited from complete transparency. Every transaction, every interest payment, every liquidation was visible on the blockchain. This resilience demonstrated the power of decentralised systems and accelerated the shift from CeFi to DeFi.

In 2026, the DeFi lending market has matured significantly. Leading protocols like Aave and Compound have processed billions of dollars in loans, undergone multiple security audits from top firms, and demonstrated resilience across multiple market cycles. The technology has evolved from simple overcollateralised lending to sophisticated features like flash loans, cross-chain functionality, and efficiency modes that maximise capital utilisation. Meanwhile, centralised alternatives like Nexo continue to serve users who prefer the convenience of traditional platforms whilst benefiting from crypto yields, though with the inherent custody risks.

The market size tells the story: DeFi lending protocols collectively manage $15-20 billion in total value locked (TVL) as of 2026, down from the 2021 peak of $50+ billion but representing a more sustainable, mature market. Aave alone accounts for $6-8 billion of this, whilst Compound maintains $2-3 billion. These aren't speculative bubbles—they're working financial systems processing real loans for real users every day.

This comprehensive guide will take you from complete beginner to confident DeFi lender. You'll learn how protocols like Aave and Compound work at a technical level, understand the risks involved, discover strategies to maximise your returns, and make informed decisions about whether DeFi lending is right for you. We'll cover everything from basic concepts to advanced strategies, ensuring you have the knowledge to participate safely and effectively.

Whether you're looking to earn passive income on your stablecoins, borrow against your Bitcoin without triggering a taxable event, leverage your positions for trading, or simply understand this revolutionary technology, this guide provides everything you need to navigate the DeFi lending landscape in 2026. We'll examine real-world examples, analyse actual interest rates, and provide step-by-step instructions for getting started.

The technology underlying DeFi lending is remarkably elegant. Smart contracts—immutable programs running on blockchain networks—automatically match lenders with borrowers, calculate interest rates based on supply and demand, manage collateral, and execute liquidations when necessary. No human intervention required. No credit checks. No paperwork. Just code executing exactly as programmed, 24/7, without holidays or downtime.

This automation creates unprecedented efficiency. Traditional banks maintain massive overhead—branches, staff, compliance departments, marketing—all funded by the spread between what they pay depositors and charge borrowers. DeFi protocols eliminate most of this overhead, passing the savings to users. When you lend USDC on Aave, you might earn 4-5% whilst borrowers pay 5-6%—a spread of just 1-2% compared to traditional banking spreads of 5-10% or more.

The transparency is equally revolutionary. Every transaction, every interest payment, every liquidation is recorded on the blockchain for anyone to verify. You can see exactly how much is deposited, how much is borrowed, the current interest rates, and how they're calculated. Compare this to traditional banking, where interest rate calculations are opaque, terms can change without notice, and you have no visibility into how your deposits are being used.

But perhaps most importantly, DeFi lending offers genuine financial inclusion. Anyone with an internet connection can participate, regardless of their location, credit history, or wealth. No minimum balance requirements. No credit checks. No discrimination. The protocol doesn't care if you're in New York or Nigeria, whether you're 18 or 80, or what your credit score is. If you have cryptocurrency to lend or collateral to borrow against, you can participate.

The composability of DeFi protocols creates additional opportunities. Your supplied assets on Aave can be used as collateral across multiple protocols simultaneously through integrations. Yield aggregators like Yearn Finance can automatically move your funds between protocols to maximise returns. Flash loans enable sophisticated arbitrage strategies that were impossible in traditional finance. This interconnected ecosystem of protocols, each building on the others, creates a financial system that's greater than the sum of its parts.

What you'll learn:

- How DeFi lending protocols work (smart contracts, liquidity pools, interest rates)

- Detailed analysis of Aave, Compound, and Nexo platforms

- Interest rate models and how to calculate your potential earnings

- Collateral requirements and loan-to-value ratios

- Risk management strategies (liquidation, smart contracts, oracles)

- Step-by-step guide to start lending or borrowing

- CeFi vs DeFi comparison (when to use which)

- Tax implications and reporting requirements

- Future trends and innovations in DeFi lending

Let's begin by understanding the fundamental mechanics of how DeFi lending actually works.

Understanding DeFi Lending Mechanics

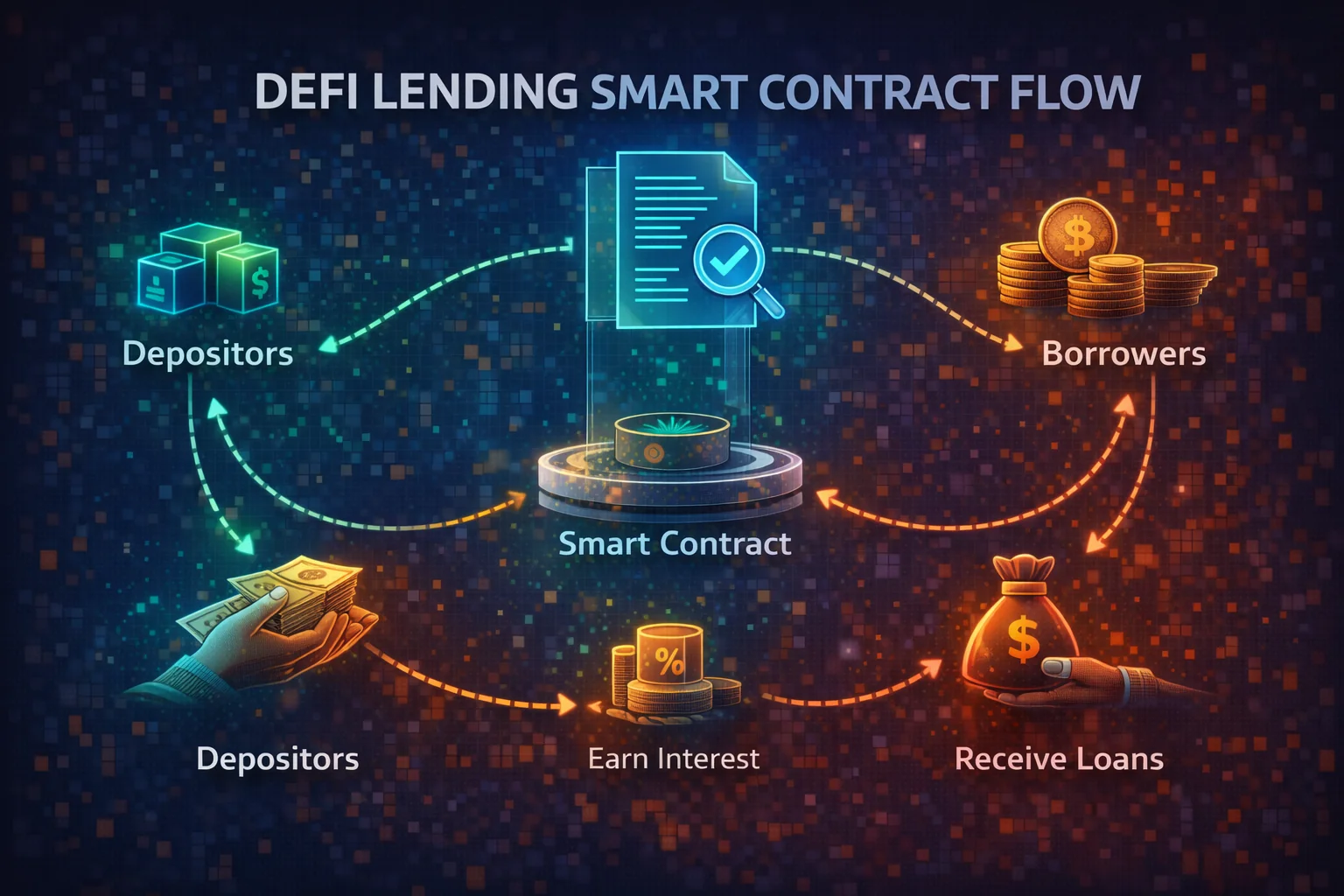

At its core, DeFi lending operates on a simple principle: users who have cryptocurrency they're not actively using can supply it to a protocol, where it becomes available for others to borrow. In return, lenders earn interest, whilst borrowers pay interest. Smart contracts automate everything—from calculating interest rates to managing collateral to executing liquidations when necessary.

The Basic Concept

Think of a DeFi lending protocol as a decentralised bank, but instead of a building with tellers and managers, it's code running on a blockchain. When you supply assets to a protocol like Aave or Compound, your cryptocurrency goes into a liquidity pool—essentially a smart contract that holds all the supplied assets of that type.

For example, if you supply 10,000 USDC to Aave, your tokens join the USDC liquidity pool alongside thousands of other users' USDC. In return, you receive aTokens (in Aave's case) or cTokens (in Compound's case)—special tokens that represent your share of the pool and automatically accrue interest.

Borrowers can then take loans from these liquidity pools, but there's a crucial difference from traditional lending: they must provide collateral worth significantly more than what they borrow. This overcollateralisation—typically requiring 150-200% collateral—protects lenders from default risk. If a borrower's collateral value drops too low, the protocol automatically liquidates their position to repay lenders.

Key Participants

The DeFi lending ecosystem involves four main types of participants, each playing a crucial role:

Lenders (Liquidity Providers): These users supply cryptocurrency to lending pools to earn interest. They can withdraw their funds at any time (assuming sufficient liquidity in the pool). Lenders take on smart contract risk and protocol risk, but generally face lower risk than borrowers since their funds are overcollateralised.

Borrowers (Collateral Providers): These users deposit cryptocurrency as collateral and borrow other assets against it. They might borrow to avoid selling their holdings (for tax efficiency), to leverage their positions (for trading), or to access liquidity for other purposes. Borrowers face liquidation risk if the value of their collateral drops.

Liquidators: These are specialised participants who monitor borrowers' positions and execute liquidations when collateral falls below the required threshold. Liquidators earn a bonus (typically 5-15% of the liquidated collateral) to incentivise maintaining protocol health. Many liquidators use automated bots to identify and execute liquidations quickly.

Protocol Governance (Token Holders): Users who hold governance tokens like AAVE or COMP can vote on protocol parameters such as which assets to support, collateral factors, interest rate models, and protocol upgrades. This decentralised governance ensures the protocol evolves in line with community needs.

Smart Contract Architecture

Understanding how smart contracts power DeFi lending helps you appreciate both the innovation and the risks involved.

When you supply assets to a protocol, you're interacting with a smart contract that:

- Accepts your deposit and mints interest-bearing tokens (aTokens or cTokens)

- Tracks your share of the liquidity pool

- Calculates interest in real-time based on utilisation rates

- Allows you to withdraw your funds plus accrued interest

When someone borrows, the smart contract:

- Verifies they have sufficient collateral

- Calculates their maximum borrowing capacity based on collateral factors

- Transfers the borrowed assets from the liquidity pool

- Continuously monitors their health factor (collateral value vs borrowed amount)

- Triggers liquidation if the health factor falls below 1.0

The beauty of this system is its transparency and automation. Every transaction is recorded on the blockchain; interest accrues every block (approximately every 12 seconds on Ethereum); and liquidations occur automatically without human intervention. However, this also means that bugs in the smart contract code can have serious consequences, which is why security audits are crucial.

Interest Rate Calculation

Unlike traditional banks that set interest rates based on credit scores and market conditions, DeFi protocols use algorithmic interest rate models based purely on supply and demand.

The key metric is the utilisation rate:

Utilisation Rate = Total Borrowed / Total SuppliedWhen utilisation is low (lots of supply, little demand), interest rates are low to incentivise borrowing. When utilisation is high (high demand, limited supply), rates increase to incentivise more lending and discourage borrowing.

For example, if a USDC pool has:

- Total Supplied: $100 million

- Total Borrowed: $70 million

- Utilisation Rate: 70%

The protocol might set:

- Borrow Rate: 5% APR

- Supply Rate: 3.15% APR (after accounting for the reserve factor)

- Reserve Factor: 10% (portion of interest retained by protocol)

This dynamic adjustment happens continuously, meaning rates can change significantly based on market conditions. During periods of high demand (like market volatility when traders want to leverage), rates can spike to 20-30% or higher.

Technical Depth: The interest rate formula typically follows a kinked model:

If Utilisation < Optimal:

Borrow Rate = Base Rate + (Utilisation / Optimal) × Slope1

If Utilisation >= Optimal:

Borrow Rate = Base Rate + Slope1 + ((Utilisation - Optimal) / (1 - Optimal)) × Slope2Where:

- Base Rate: Minimum interest rate (e.g., 0%)

- Optimal: Target utilisation (e.g., 80%)

- Slope1: Rate increase before optimal (e.g., 4%)

- Slope2: Rate increase after optimal (e.g., 60%)

This creates a "kink" in the rate curve at the optimal utilisation point, sharply increasing rates when utilisation exceeds the target to protect liquidity.

Understanding these mechanics is essential for making informed decisions about when to lend, when to borrow, and which protocols offer the best rates for your needs. In the next section, we'll examine the leading DeFi lending protocols in detail.

Leading DeFi Lending Platforms

The DeFi lending landscape in 2026 is dominated by several well-established protocols, each with unique features and trade-offs. Let's examine the three most important platforms you need to know about.

Aave Protocol

Aave has established itself as the leading DeFi lending protocol with over $6-8 billion in total value locked (TVL) as of 2026. Originally launched as ETHLend in 2017, the protocol rebranded to Aave in 2020 and has since become synonymous with DeFi lending innovation.

Aave V3 Features:

The latest version, Aave V3, introduced several groundbreaking features that set it apart from competitors:

Portal (Cross-Chain Functionality): Portal allows users to seamlessly move their supplied assets between different blockchain networks. For example, you can supply USDC on Ethereum and borrow against it on Polygon, all within the same protocol. This cross-chain capability significantly improves capital efficiency and reduces the need to manually bridge assets.

High Efficiency Mode (E-Mode): E-Mode is a game-changer for users working with correlated assets. When enabled, it allows loan-to-value ratios up to 97% for assets in the same category. For instance, you can deposit USDC and borrow USDT at 97% LTV, compared to the standard 75-80% LTV. This is particularly useful for stablecoin arbitrage and yield farming strategies.

Isolation Mode: This feature allows Aave to list newer or riskier assets without exposing the entire protocol to potential exploits. Isolated assets have debt ceilings and can only be used as collateral for borrowing specific stablecoins. This risk management innovation enables Aave to support a wider range of assets whilst maintaining security.

Flash Loans: Aave pioneered flash loans—uncollateralised loans that must be borrowed and repaid within a single transaction. These are primarily used by sophisticated traders for arbitrage, collateral swapping, and self-liquidation. Flash loans charge a 0.09% fee and have become a crucial tool in the DeFi ecosystem.

Supported Assets: Aave supports 30+ cryptocurrencies across multiple chains, including Ethereum, Polygon, Arbitrum, Optimism, Avalanche, and Base (see our per-L2 DeFi guide for the deposit-depth picture by chain). Major assets include ETH, WBTC, USDC, USDT, DAI, LINK, AAVE, and various other tokens.

Interest Rates (Current 2026 Ranges):

- USDC: 3.5-4.5% supply APY, 5.0-6.5% borrow APR

- ETH: 2.5-3.5% supply APY, 4.0-5.5% borrow APR

- WBTC: 1.5-2.5% supply APY, 3.0-4.5% borrow APR

Security Track Record: Aave has maintained an excellent security record with no major exploits since launch. The protocol has undergone multiple audits by leading firms, including OpenZeppelin, Trail of Bits, ABDK, and Certora. Aave also maintains a bug bounty programme offering up to $250,000 for critical vulnerabilities.

The AAVE token serves as both a governance token and a safety mechanism. Token holders can stake AAVE in the Safety Module, which acts as insurance for the protocol. In return, stakers earn rewards but take on the risk that their stake will be slashed if the protocol suffers a shortfall event.

Compound Protocol

Compound, launched in 2018, is one of the oldest and most established DeFi lending protocols. Whilst it has lower TVL than Aave ($2-3 billion in 2026), Compound remains highly respected for its simplicity, security, and pioneering role in DeFi.

Compound V3 (Comet) Features:

Compound V3, also known as Comet, represents a complete redesign of the protocol with a focus on capital efficiency and gas optimisation:

Single Borrowable Asset Per Market: Unlike V2, where users could borrow any supported asset, V3 markets each have one borrowable asset (typically USDC, ETH, or WBTC). This simplification improves capital efficiency and reduces complexity. For example, the USDC market on Ethereum allows borrowing only USDC, but accepts 15+ different assets as collateral.

Improved Capital Efficiency: V3 offers higher collateral factors than V2, meaning users can borrow more against the same collateral. This makes Compound more competitive with Aave's E-Mode for certain use cases.

50% Gas Savings: Through optimised smart contract design, Compound V3 reduces gas costs by approximately 50% compared to V2. This makes it more economical for smaller transactions and frequent interactions.

Enhanced Risk Management: Each V3 market is isolated, meaning issues in one market don't affect others. Supply and borrow caps provide additional safety, preventing any single market from growing too large relative to the protocol's capacity to manage risk.

COMP Governance Token: The COMP token gives holders voting power over protocol parameters. Compound's governance process is well-established, with proposals going through community discussion, voting, and a timelock period before implementation. Recent governance decisions have included adding new markets, adjusting interest rate models, and distributing COMP rewards.

Supported Markets: Compound V3 currently operates USDC markets on Ethereum, Polygon, Arbitrum, and Base, plus ETH and WBTC markets on Ethereum. Each market accepts 10-15 different collateral assets, including major cryptocurrencies and stablecoins.

Interest Rates (Current 2026 Ranges):

- USDC: 3.0-4.0% supply APY, 4.5-6.0% borrow APR

- ETH: 2.0-3.0% supply APY, 3.5-5.0% borrow APR

- WBTC: 1.0-2.0% supply APY, 2.5-4.0% borrow APR

Security Track Record: Compound has a strong security record with only minor historical issues. A 2020 bug affecting DAI liquidations was quickly identified and fixed. The protocol has been audited by OpenZeppelin, ChainSecurity, and Trail of Bits. Compound also maintains a bug bounty programme offering up to $150,000 for critical vulnerabilities.

The protocol's simplicity is both a strength and a limitation. Whilst Compound lacks some of Aave's advanced features, such as flash loans and E-Mode, its straightforward design makes it easier for beginners to understand and use. The single-borrowable-asset-per-market model also reduces complexity and potential attack vectors.

Nexo Platform (CeFi Alternative)

Whilst Aave and Compound represent the DeFi approach to lending, Nexo offers a centralised finance (CeFi) alternative that appeals to users seeking simplicity and traditional customer service.

Important Note: Nexo is not available to U.S. residents following a 2022 SEC settlement. U.S. users should consider Aave or Compound instead.

Nexo Platform Features:

Instant Crypto Credit Lines: Nexo allows users to borrow against their cryptocurrency holdings instantly, without credit checks or lengthy approval processes. Loans are available in both cryptocurrency and fiat, with funds deposited directly into your bank account if needed.

High Interest Rates: Nexo offers some of the highest interest rates in the industry, with stablecoins earning up to 16% APY for Platinum tier users. These rates are significantly higher than DeFi protocols, though they come with the trade-off of centralised custody.

Nexo Card: The Nexo Card is a crypto-backed Mastercard that allows spending without selling your cryptocurrency. Users can access up to 90% of their portfolio value as a line of credit, with no monthly fees and up to 2% cashback in NEXO tokens. The card is available in 40+ countries (excluding the U.S.).

Loyalty Tiers: Nexo operates a four-tier loyalty system based on NEXO token holdings:

- Base (0-9% NEXO): Standard rates

- Silver (10-14% NEXO): +0.5% earn, -0.5% borrow

- Gold (15-19% NEXO): +1% earn, -1% borrow

- Platinum (20%+ NEXO): +2% earn, -2% borrow (0% borrow rate possible)

Insurance Coverage: Nexo maintains $775 million in insurance coverage through BitGo Trust and Lloyd's of London, protecting custodial assets against hacks and theft. However, this insurance doesn't cover market risk or platform insolvency.

Regulatory Compliance: Nexo is regulated in multiple European jurisdictions and holds SOC 2 Type 2 and SOC 3 certifications. The platform conducts real-time attestations through Moore (via its TrustReserve suite), providing transparency into its reserves.

Interest Rates (Current 2026):

- Stablecoins: Up to 16% APY (Platinum tier)

- Bitcoin: Up to 8% APY

- Ethereum: Up to 7% APY

- Daily interest payouts

Security Considerations: Whilst Nexo has maintained a strong security record with no major hacks, users must trust the platform with custody of their assets. The collapse of Celsius and BlockFi in 2022 serves as a reminder that CeFi platforms carry counterparty risk that doesn't exist in non-custodial DeFi protocols.

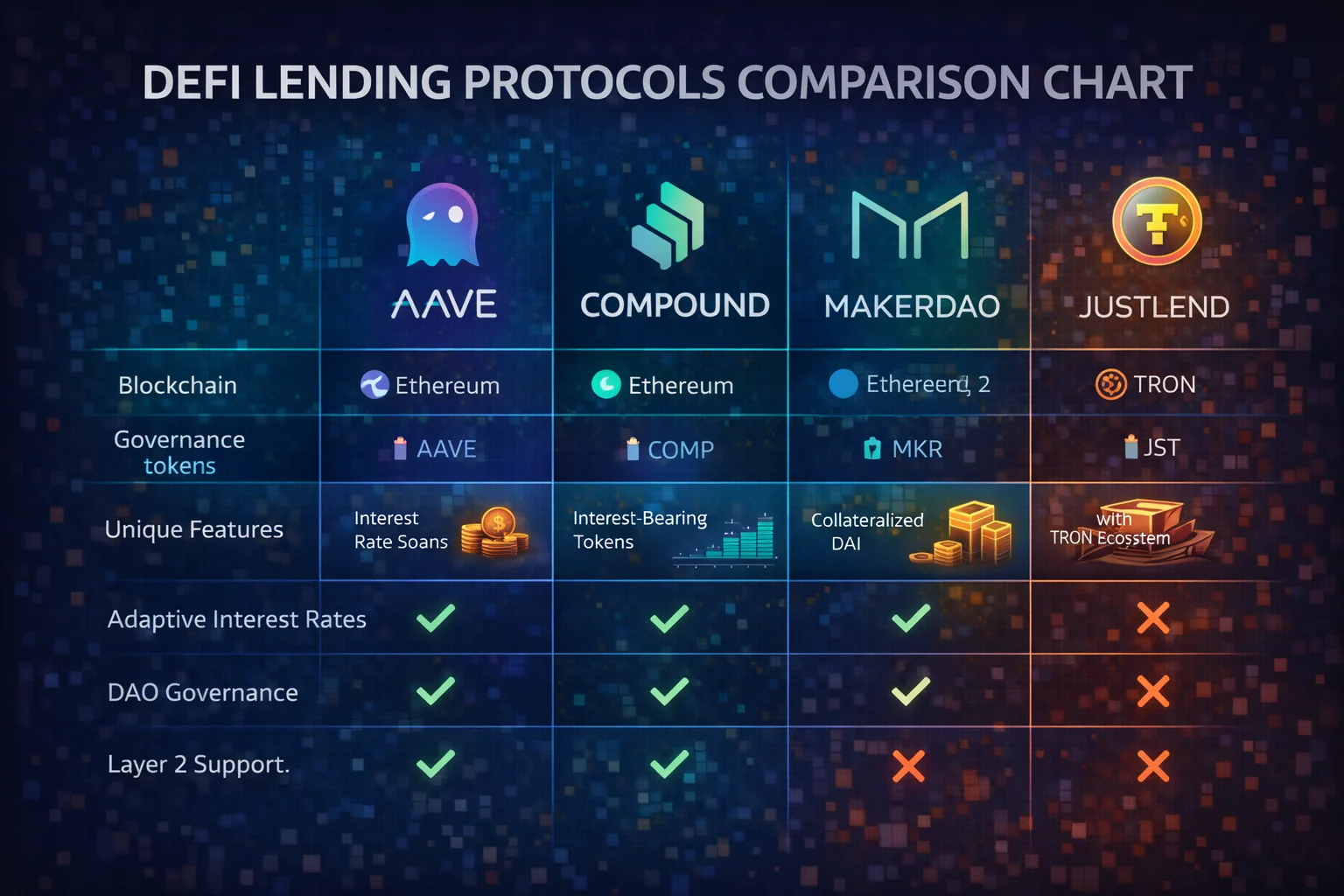

Comparison Table: Aave vs Compound vs Nexo

| Feature | Aave | Compound | Nexo |

|---|---|---|---|

| Type | DeFi | DeFi | CeFi |

| TVL (2026) | $6-8B | $2-3B | N/A (centralised) |

| Custody | Non-custodial | Non-custodial | Centralised |

| Interest Rates (USDC) | 3.5-4.5% | 3.0-4.0% | Up to 16% |

| Supported Assets | 30+ | 15+ | 40+ |

| Cross-Chain | Yes (6+ chains) | Yes (4+ chains) | N/A |

| Flash Loans | Yes | No | No |

| E-Mode | Yes (97% LTV) | No | N/A |

| Insurance | Protocol risk | Protocol risk | $775M coverage |

| U.S. Access | Yes | Yes | No |

| Beginner-Friendly | 7/10 | 8/10 | 9/10 |

| Security Rating | 4.5/5.0 | 4.0/5.0 | 4.0/5.0 |

| Overall Rating | 4.2/5.0 | 4.0/5.0 | 3.8/5.0 |

Which to Choose:

- Aave: Best for experienced users who need advanced features like flash loans, E-Mode, or cross-chain functionality

- Compound: Best for beginners who want simplicity and lower gas costs

- Nexo: Best for EU users who prioritise ease of use, high rates, and don't mind centralised custody

In the next section, we'll dive deep into how interest rates work in DeFi lending and how you can calculate your potential earnings.

How DeFi Lending Interest Rates Work

Understanding how DeFi interest rates are calculated is crucial for maximising your returns and making informed decisions about when to lend or borrow. Unlike traditional banks that set rates based on credit scores and central bank policies, DeFi protocols use purely algorithmic models driven by supply and demand.

For a detailed technical analysis of interest rate formulas and utilisation curves, see our guide on DeFi Interest Rate Models Explained.

Understanding Collateral Requirements

One of the most fundamental concepts in DeFi lending is overcollateralisation—the requirement to deposit assets worth significantly more than what you borrow. This mechanism makes trustless lending possible by eliminating counterparty risk for lenders.

For an in-depth comparison of different lending models, see our guide on Overcollateralised vs Undercollateralised Lending.

DeFi Lending Risks You Must Understand

DeFi lending offers attractive returns, but it's not without risks. Understanding these risks and how to manage them is crucial for protecting your capital.

Smart Contract Risk

Smart contract risk is the possibility that bugs or vulnerabilities in the protocol's code could lead to loss of funds. Despite extensive audits, smart contracts are complex software that can contain undiscovered flaws.

Liquidation Risk

For borrowers, liquidation risk is the most immediate and common danger. Market volatility can quickly erode your health factor, leading to costly liquidations.

Oracle Risk

DeFi protocols rely on price oracles—external data feeds that report asset prices to smart contracts. If an oracle provides incorrect price data, it can trigger unwarranted liquidations or allow manipulation.

For comprehensive risk management strategies and specific tools, see our detailed guide on DeFi Lending Risks Management 2026. To learn about security best practices and protecting your assets, read our DeFi Lending Security Best Practices 2026 guide.

How to Start DeFi Lending

This step-by-step guide walks you through the entire process.

Prerequisites

Before you begin, ensure you have:

- A Web3 wallet (MetaMask, Rabby, or Rainbow)

- Cryptocurrency to supply or use as collateral

- ETH (or native token) for gas fees

- Basic understanding of risks

Choosing the Right Protocol

Your first decision is which protocol to use. For beginners, we recommend starting with Aave on Polygon for several reasons: lower gas fees (often under $0.01), a user-friendly interface, and extensive documentation. Polygon's network is faster and cheaper than the Ethereum mainnet, making it ideal for learning without high cost.

If you prefer maximum simplicity, Compound offers a streamlined experience with fewer features but easier navigation. For EU users comfortable with centralised platforms, Nexo provides the highest interest rates and traditional customer support, though you'll sacrifice self-custody.

Setting Up Your Wallet

If you don't already have a Web3 wallet, download MetaMask from metamask.io. Create a new wallet, securely store your seed phrase (write it down on paper, never store it digitally), and add the Polygon network to your wallet. You can find network details on Polygon's official website or use MetaMask's built-in network selector.

Transfer some USDC, USDT, or other stablecoins to your Polygon wallet. Also, ensure you have a small amount of MATIC (Polygon's native token) for gas fees—$5 worth of MATIC will cover hundreds of transactions.

Supplying Assets (Lending)

Navigate to app.aave.com and connect your wallet. Select the Polygon network from the dropdown menu. Click "Supply" and choose the asset you want to lend (e.g., USDC). Enter the amount you wish to supply—start with $100-500 for your first transaction to familiarise yourself with the process.

Review the transaction details, including the current APY and gas fees. Approve the transaction in your wallet. You'll need to complete two transactions: one to approve the protocol to access your tokens, and another to actually supply them. Once confirmed, you'll immediately start earning interest, which accrues every block (approximately every 2 seconds on Polygon).

Your supplied assets are represented by aTokens (e.g., aUSDC for supplied USDC). These tokens automatically increase in value as interest accrues, so you don't need to claim rewards—simply hold them in your wallet.

Borrowing Assets

To borrow, you must first supply collateral. Navigate to the "Borrow" section and select the asset you want to borrow. The interface will show your maximum borrowing capacity based on your supplied collateral and the asset's collateral factor.

For your first borrow, use only 30-40% of your maximum capacity to maintain a healthy safety margin. Select between stable or variable interest rates—variable rates are typically lower but can fluctuate, whilst stable rates provide predictability. Confirm the transaction, and the borrowed assets will appear in your wallet.

Monitor your health factors daily. If it approaches 1.2 or lower, add more collateral or repay part of your loan immediately. Set up price alerts for your collateral assets to avoid surprise liquidations during market volatility.

Monitoring and Managing Your Positions

Check your positions regularly through the Aave dashboard. The interface displays your supplied assets, borrowed amounts, current APYs, and most importantly, your health factor. Enable email notifications if available, and consider using third-party monitoring tools like DeFi Saver or Instadapp for advanced alerts.

To withdraw supplied assets, navigate to your dashboard, click "Withdraw" next to the asset, and specify the amount. You can withdraw at any time, as long as the assets you supplied aren't being used as collateral for an active loan. If you have an active borrow position, you can only withdraw the portion not required to maintain your health factor above 1.0.

To repay a loan, click "Repay" next to your borrowed asset and choose the amount to repay. You can make partial repayments to improve your health factor or repay the full amount to close the position. Remember that you'll need to repay both the principal and accrued interest.

Centralised vs Decentralised Lending

The choice between CeFi (centralised finance) and DeFi (decentralised finance) lending isn't always clear-cut. Each approach has distinct advantages and trade-offs.

Key Differences

- Custody: DeFi = self-custody, CeFi = platform custody

- Transparency: DeFi = on-chain verification, CeFi = trust-based

- Interest Rates: DeFi = algorithmic (2-6%), CeFi = platform-set (up to 16%)

- User Experience: DeFi = technical, CeFi = beginner-friendly

DeFi Lending Advantages

DeFi protocols offer several compelling benefits that make them attractive for experienced users and those prioritising security and transparency. Self-custody means you maintain control of your private keys and assets at all times—no platform can freeze your funds or prevent withdrawals. Every transaction is recorded on the blockchain, providing complete transparency into protocol operations, reserves, and utilisation rates.

Permissionless access means anyone with an internet connection can participate, regardless of location, credit history, or identity. There are no KYC requirements, account approvals, or minimum balances. Smart contracts execute automatically without human intervention, eliminating counterparty risk and ensuring consistent, predictable behaviour.

CeFi Lending Advantages

Centralised platforms like Nexo offer advantages that appeal to beginners and users prioritising convenience over decentralisation. The user experience is significantly simpler—no need to manage private keys, understand gas fees, or navigate complex DeFi interfaces. Customer support is available via email, chat, or phone to assist when issues arise.

Interest rates are often higher in CeFi platforms (up to 16% vs 3-5% in DeFi) because platforms can deploy capital more efficiently and take on additional risk. Fiat on-ramps and off-ramps are integrated, allowing direct bank transfers without using cryptocurrency exchanges. Insurance coverage (though limited) provides some protection against platform hacks.

The Hybrid Approach

Many sophisticated users employ a hybrid strategy, allocating capital across both DeFi and CeFi platforms to optimise risk-adjusted returns. For example, you might keep 60% of lending capital in DeFi protocols (Aave, Compound) for security and transparency, whilst allocating 40% to CeFi platforms (Nexo) for higher yields. This diversification protects against both smart contract risk (DeFi) and platform insolvency risk (CeFi).

Consider your risk tolerance, technical expertise, and capital size when deciding your allocation. Larger positions ($50,000+) often benefit from DeFi's transparency and security, whilst smaller positions ($5,000 or less) may find CeFi's simplicity and higher rates more attractive after accounting for gas fees.

DeFi Lending Tax Considerations

Tax treatment of DeFi lending varies significantly by jurisdiction and is still evolving as regulators catch up with the technology. Understanding the general principles helps you plan appropriately and avoid costly mistakes.

Interest Income Taxation

In most jurisdictions, interest earned from lending cryptocurrency is treated as ordinary income and taxed at your marginal income tax rate. The complexity lies in determining when interest is "received" for tax purposes. Some tax authorities consider interest received as it accrues (every block), whilst others treat it as received only upon withdrawal. The IRS in the United States, for example, generally considers cryptocurrency interest as income when you have dominion and control over it.

For DeFi protocols where interest accrues automatically to your aTokens or cTokens, you technically have control over the interest immediately, suggesting it should be reported as income as it accrues. However, many taxpayers report it only upon withdrawal for practical reasons. Consult a tax professional familiar with cryptocurrency for guidance specific to your situation.

Borrowing and Loan Repayment

Borrowing cryptocurrency is generally not a taxable event in most jurisdictions because you're receiving a loan, not income. You have an obligation to repay the borrowed amount, so there's no realised gain. This is one reason why crypto-backed loans are popular for accessing liquidity without triggering capital gains taxes.

Repaying a loan is also typically not taxable, as you're simply fulfilling your loan obligation. However, if you repay a loan with cryptocurrency that has appreciated in value since you acquired it, the repayment may trigger a capital gains event. For example, if you borrowed 10,000 USDC and repaid it with 1 ETH that you originally purchased for $1,500 but is now worth $10,000, you may owe capital gains tax on the $8,500 appreciation.

Liquidation Tax Treatment

Liquidations can have complex tax implications. When your position is liquidated, you're effectively selling your collateral to repay your debt. This sale may trigger capital gains or losses depending on your cost basis in the collateral. Additionally, the liquidation penalty (typically 5-15% of the liquidated amount) is a realised loss that may be deductible.

Proper record keeping is essential for calculating your tax liability accurately. Track your cost basis for all supplied and borrowed assets, record all interest earned with timestamps, and maintain transaction records for all deposits, withdrawals, borrows, repayments, and liquidations.

General Principles:

- Interest earned is typically treated as ordinary income

- Borrowing is generally not a taxable event

- Liquidations may trigger capital gains/losses

- Proper record keeping is essential

DeFi Lending Trends and Beyond

The DeFi lending landscape continues to evolve rapidly. Understanding emerging trends helps you anticipate opportunities and position yourself advantageously.

Key Trends

- Undercollateralised Lending: Credit scoring and RWA collateral

- Cross-Chain Lending: Unified liquidity across blockchains

- Institutional Adoption: Regulatory clarity driving participation

- Yield Optimisation: Automated strategies and AI-powered management

- Regulatory Evolution: Compliance-first protocols emerging

The future of DeFi lending is bright, with innovations addressing current limitations whilst maintaining the core benefits of transparency, accessibility, and self-custody.

Getting Started with DeFi Lending

DeFi lending represents a fundamental shift in how we think about borrowing and lending money. By eliminating intermediaries and automating operations with smart contracts, protocols like Aave and Compound offer unprecedented transparency, accessibility, and control over your financial activities.

Throughout this guide, we've covered everything you need to know to start lending or borrowing in DeFi—from the fundamentals of how protocols work to detailed platform analysis, risk management strategies, and practical step-by-step instructions. We've explored the technical architecture that enables these protocols, examined real-world use cases, and provided comprehensive risk management frameworks to protect your capital.

The DeFi lending market has matured significantly since its inception. With over $20 billion in total value locked across major protocols, institutional adoption increasing, and regulatory frameworks beginning to take shape, we're witnessing the transformation of traditional finance. The 2022 CeFi collapse demonstrated the critical importance of transparency and self-custody—principles that DeFi lending embodies at its core.

Your Next Steps:

If you're ready to start, begin small. Supply $100-500 to Aave on Polygon to test the process without significant risk or gas fees. Experience how interest accrues, practise withdrawing, and familiarise yourself with the interface. Once comfortable, you can scale up your position. This hands-on experience will teach you more than any guide can convey.

For borrowers, start by supplying collateral and borrowing a small amount—perhaps 30-40% of your maximum borrowing capacity. Monitor your health factor daily and practise adding collateral or repaying debt. Understanding liquidation mechanics through small-scale testing is far better than learning the hard way through a costly liquidation event.

Consider diversifying across multiple protocols to reduce smart contract risk. Don't put all your capital in a single protocol, regardless of how established it appears. The DeFi ecosystem is still evolving, and whilst protocol failures are rare, they do occur. A diversified approach across Aave, Compound, and potentially CeFi alternatives like Nexo provides better risk-adjusted returns.

Stay informed about protocol updates, governance proposals, and market conditions. Join the protocol's Discord servers, follow the official Twitter accounts, and participate in governance discussions. The DeFi community is remarkably transparent and collaborative—take advantage of these resources to deepen your understanding.

Remember: DeFi lending offers attractive returns, but it's not without risks. Never invest more than you can afford to lose; always maintain a healthy balance when borrowing; and continuously educate yourself as the ecosystem evolves. The protocols we've discussed have proven track records, but past performance doesn't guarantee future results.

Liquid staking tokens (stETH, rETH) are increasingly used as collateral on Aave and Compound, combining staking yield with borrowing capacity. For a detailed breakdown of slashing risk, depeg scenarios, and how to evaluate LST collateral safely, see our liquid staking yield strategies guide.

Keep a practical checklist for staking interactions, consensus events, and validator performance — these factors influence collateral liquidity during stress periods.

You should review tokenomics updates before increasing size, and you should define hard slippage limits for every rebalance to avoid poor execution.

If your strategy includes AMM exposure, you should track impermanent loss explicitly and separate it from lending APY and borrowing APR.

You should treat NFT-linked collateral as high-volatility capital and keep tighter risk limits than for major assets.

The regulatory landscape is evolving rapidly. Whilst DeFi protocols remain permissionless and decentralised, governments worldwide are developing frameworks to address cryptocurrency activities. Stay informed about regulatory developments in your jurisdiction, maintain proper tax records, and consider consulting with legal and tax professionals as your involvement grows. Compliance today protects your ability to participate tomorrow.

Technology continues advancing at a remarkable pace. Cross-chain lending, real-world asset tokenisation, undercollateralised lending through credit protocols, and integration with traditional finance are all emerging trends that will shape the next generation of DeFi lending. By understanding the fundamentals covered in this guide, you'll be well-positioned to evaluate and adopt these innovations as they mature.

The DeFi lending revolution is just beginning. By understanding these protocols and participating responsibly, you're positioning yourself at the forefront of financial innovation. Whether you're earning passive income through lending or accessing capital through borrowing, you're part of a movement that's reshaping global finance—one smart contract at a time.

Sources & References

This comprehensive guide draws on official protocol documentation, security audits, academic research, and industry analysis to provide accurate, up-to-date information about DeFi lending in 2026.

- Aave V3 Technical Documentation - Official Aave protocol documentation

- Compound V3 Documentation - Comprehensive Compound protocol documentation

- Nexo Platform Documentation - Official Nexo support documentation

- OpenZeppelin Audits - Security audit reports for major DeFi protocols

- DeFi Llama - Real-time TVL data and protocol analytics

- Messari Research - In-depth protocol analysis and market research

Disclaimer: Cryptocurrency lending involves significant risk. This guide is for educational purposes only and does not constitute financial advice. Always conduct your own research and consult with qualified financial advisors before making investment decisions.

Frequently Asked Questions

- Is DeFi lending safe?

- DeFi lending carries risks including smart contract vulnerabilities, liquidation risk, and oracle failures. However, established protocols like Aave and Compound have strong security track records with multiple audits and years of operation. To minimise risk, use well-established protocols, start with small amounts, maintain conservative health factors when borrowing, and never invest more than you can afford to lose.

- How much can I earn lending cryptocurrency?

- Returns vary based on the asset and market conditions. As of 2026, typical rates are: stablecoins (USDC, USDT) earn 3-5% APY in DeFi protocols or up to 16% in CeFi platforms like Nexo; Ethereum earns 2-4% APY; Bitcoin earns 1-3% APY. Rates fluctuate based on supply and demand, sometimes spiking to 20-30%+ during periods of high volatility.

- What happens if I get liquidated?

- If your health factor drops below 1.0, liquidators can repay up to 50% of your debt in exchange for your collateral plus a liquidation bonus (typically 5-15%). This means you lose more collateral than you repay in debt. To avoid liquidation, maintain a health factor above 2.0 and monitor it daily.

- Can I lose money lending in DeFi?

- Yes, though it's less common than with borrowing. Risks include smart contract exploits (rare but possible) and opportunity costs if rates drop significantly. However, if you're simply supplying assets to Aave or Compound, your principal is protected by overcollateralisation—borrowers must deposit more value than they borrow.

- Do I need to pay taxes on DeFi lending?

- Yes, in most jurisdictions. Interest earned from lending is typically treated as ordinary income and taxed in the year it is received. The complexity is determining when interest is "received"—some tax authorities consider it received as it accrues (every block), whilst others treat it as received only upon withdrawal. Consult a tax professional familiar with cryptocurrency for guidance specific to your jurisdiction.

- What's the difference between Aave and Compound?

- Aave offers more advanced features, including flash loans, E-Mode (up to 97% LTV for correlated assets), and cross-chain functionality. It supports 30+ assets across 6+ blockchains. Compound focuses on simplicity, with a single borrowable asset per market and 50% lower gas costs. Aave typically has higher TVL ($6-8B vs $2-3B) and slightly better rates.

- How do interest rates work in DeFi lending?

- Interest rates in DeFi are determined algorithmically based on utilisation rate (percentage of supplied assets that are borrowed). When utilisation is low (50%), rates are low (2-3% APY). When utilisation approaches optimal (80-90%), rates increase moderately (4-5% APY). Above optimal utilisation, rates spike dramatically (20-50%+ APY) to protect protocol liquidity. Rates update automatically every block (approximately every 12 seconds).

- What is a health factor and why does it matter?

- Health factor measures the safety of your borrowing position. It's calculated as (Collateral Value × Liquidation Threshold) / Borrowed Value. A health factor above 1.0 means your position is safe. Below 1.0 triggers liquidation. Maintain a health factor of 2.5-3.0 minimum to survive 60-67% collateral price drops. Monitor it daily and add collateral or repay debt if it drops below 2.0.

- Can I withdraw my supplied assets anytime?

- Usually yes, but it depends on protocol utilisation. If utilisation is below 95%, withdrawals are instant. If utilisation exceeds 95%, you may need to wait for borrowers to repay before withdrawing. This is rare because high utilisation triggers higher interest rates, which quickly bring utilisation back down. To ensure liquidity, avoid protocols with consistently high utilisation (above 90%).

- What are the main risks of DeFi lending?

- The four main risks are: (1) Smart contract risk—bugs or exploits in protocol code, mitigated by using audited protocols like Aave and Compound; (2) Liquidation risk—losing collateral if health factor drops below 1.0, mitigated by maintaining high health factors; (3) Oracle risk—incorrect price feeds causing unfair liquidations, mitigated by protocols using Chainlink; (4) Systemic risk—market-wide events like stablecoin depegs or liquidity crises, mitigated by diversification and conservative position sizing.

Should I use DeFi or CeFi for lending?

Choose DeFi (Aave, Compound) if you value self-custody, transparency, have larger positions ($10,000+), or need advanced features. Choose CeFi (Nexo) if you prioritise simplicity, want higher yields (up to 16% vs 3-5%), have smaller positions (under $5,000), or value customer support. Many users employ a hybrid approach to diversify risk and optimise returns.

How do I start DeFi lending with no experience?

Start by setting up a Web3 wallet like MetaMask, then acquire some cryptocurrency (USDC is easiest for beginners) and ETH for gas fees. Choose a Layer 2 network like Polygon for low fees. Navigate to app.aave.com, connect your wallet, and supply a small amount ($100-500) to test the process. Monitor how interest accrues over a few days. Once comfortable, you can increase your position.

What is a health factor and why does it matter?

Your health factor is a numerical representation of the safety of your borrowed position, calculated as (Collateral × Liquidation Threshold) / Total Borrowed. A health factor above 1.0 means your position is safe; below 1.0 triggers liquidation. Maintain a health factor above 2.0 to provide a safety buffer against market volatility. You can improve your health factor by adding more collateral or repaying part of your loan.

Can I withdraw my supplied assets at any time?

Yes, you can withdraw supplied assets at any time, provided they're not being used as collateral for an active loan. If you have borrowed against your supplied assets, you can only withdraw the portion not required to maintain your health factor above 1.0. There are no lock-up periods or withdrawal penalties in DeFi lending protocols, though you'll need to pay gas fees for the withdrawal transaction.

What are flash loans, and should I use them?

Flash loans are uncollateralised loans that must be borrowed and repaid within a single transaction (typically within seconds). They're primarily used by developers and traders for arbitrage, collateral swaps, and liquidations. Unless you're an experienced developer or trader with specific use cases, you don't need flash loans for standard lending or borrowing activities. Aave offers flash loans, whilst Compound does not.

How do gas fees affect my returns?

Gas fees can significantly impact returns, especially for smaller positions. On the Ethereum mainnet, a single supply transaction might cost $10-50 during peak times, making it uneconomical for positions under $5,000. This is why we recommend using Layer 2 networks like Polygon (gas fees under $0.01) or Arbitrum for smaller positions. Calculate your break-even point: if gas fees are $20 and you're earning 4% APY on $1,000, you need 5 months just to recover the gas costs.

What is the minimum amount needed to start DeFi lending?

Technically, there's no minimum, but practical considerations apply. On the Ethereum mainnet, gas fees make positions under $5,000 uneconomical. On Layer 2 networks like Polygon or Arbitrum, you can start with as little as $100-500 and still earn meaningful returns after gas costs. For CeFi platforms like Nexo, you can start with $10-50, as there are no gas fees. We recommend starting with $500-1,000 to test the process whilst keeping risk manageable.

How often is interest paid in DeFi lending?

Interest accrues continuously with every Ethereum block (approximately every 12 seconds). Your balance increases in real-time as interest compounds automatically. You don't need to claim or withdraw interest—it's automatically added to your supplied balance and begins earning additional interest immediately. This continuous compounding is one of DeFi's key advantages over traditional finance, where interest is typically paid monthly or quarterly.

Can I use DeFi lending from any country?

DeFi protocols like Aave and Compound are permissionless and accessible globally—you only need an internet connection and a Web3 wallet. There are no KYC requirements or geographic restrictions. However, some countries restrict cryptocurrency usage, and you're responsible for complying with local laws. CeFi platforms like Nexo have geographic restrictions (notably excluding U.S. residents) and require KYC verification. Always verify your jurisdiction's legal status before participating.

What's the difference between APY and APR in DeFi lending?

APR (Annual Percentage Rate) is the simple interest rate without compounding. APY (Annual Percentage Yield) includes the effect of compounding. In DeFi, interest compounds continuously (every block), so APY is always higher than APR. For example, a 5% APR becomes approximately 5.13% APY with continuous compounding. Most DeFi interfaces display APY because it more accurately represents your actual returns. The difference becomes more significant at higher rates—a 20% APR becomes approximately 22.14% APY.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.