Yield Optimisation Strategies

Master advanced DeFi yield optimisation through Pendle yield tokenisation, ve-tokenomics governance, and auto-compounding aggregation. Compare protocol mechanics, risk profiles, and practical strategies for maximising returns in 2026.

Introduction: The Yield Optimisation Landscape

Yield optimisation in decentralised finance has matured far beyond simple liquidity mining, and you should understand what separates the survivors from the failures. The protocols that endured the 2022-2023 bear market generate real yield from genuine economic activity rather than relying on unsustainable token emissions. In 2026, you can build your yield portfolio on three interconnected pillars — yield tokenisation through Pendle Finance, vote-escrow governance across Curve, Pendle, and Balancer, and automated yield aggregation through Yearn Finance and Convex Finance.

This guide is for you if you are an intermediate to advanced DeFi participant who wants to move beyond basic yield farming. If you already understand how liquidity pools, lending protocols, and governance tokens work, this guide picks up where those fundamentals leave off. For foundational concepts, see our DeFi lending guide and our liquid staking yield strategies guide.

What makes 2026 different? First, Pendle Finance has grown to over $5 billion in total value locked, making yield tokenisation a mainstream DeFi primitive. You can now split any yield-bearing asset into principal and yield components — locking in fixed rates, speculating on yield direction, or creating structured products. Second, ve-tokenomics models have proven their durability across multiple market cycles. Third, auto-compounding through Yearn V3 vaults and Convex CRV boosting has become commoditised, letting you focus on strategic allocation rather than mechanical harvesting.

A critical distinction you must understand is the difference between real yield and inflationary yield. Real yield comes from genuine protocol revenue — trading fees on Curve, yield trading fees on Pendle, borrowing interest on Aave. Inflationary yield comes from newly minted governance tokens. You should build your core positions around real yield sources and treat inflationary incentives as temporary bonuses. For a deeper analysis, see our article on real yield versus inflationary rewards.

Before you implement any strategy here, remember that higher yields always correspond to higher risks. Smart contract vulnerabilities, impermanent loss, governance attacks, and composability failures can all result in partial or total loss of your capital. Never allocate more than you can afford to lose, and start with small positions to understand the mechanics before scaling up.

Yield figures throughout this guide reflect conditions as of early 2026. Rather than memorising specific rates, focus on understanding the mechanisms that generate yield and the frameworks for evaluating risk-adjusted returns. Whether you are allocating $5,000 or $500,000, the principles remain the same — only the position sizes change.

A note on the protocols covered here: Pendle Finance, Curve Finance, Yearn Finance, and Convex Finance were selected because they represent the most established and battle-tested yield infrastructure in DeFi as of 2026. Each has survived at least one full market cycle, maintained significant total value locked through bear market conditions, and demonstrated genuine product-market fit through sustained usage rather than temporary incentive programmes. Newer protocols may offer higher yields, but the risk-adjusted returns from established infrastructure consistently outperform speculative allocations over multi-month horizons. You should evaluate any new yield protocol against these benchmarks before committing meaningful capital. Our Pendle vs Yearn vs Convex comparison provides a detailed side-by-side analysis of these protocols across security, yield performance, and fee structures.

Yield Tokenisation: How Pendle Splits Yield from Principal

Yield tokenisation is the process of separating a yield-bearing asset into two distinct tradeable components: the Principal Token (PT) and the Yield Token (YT), and Pendle Finance pioneered this approach in DeFi. You should care about this mechanism because it allows you to trade future yield independently from the underlying principal, unlocking strategies that are fundamentally impossible with traditional yield farming.

When you deposit a yield-bearing asset such as stETH, GLP, or a Yearn vault token into Pendle, the protocol mints two tokens. The PT represents your claim on the underlying principal at maturity — if you deposit 1 stETH, you can redeem 1 ETH worth of stETH when the market expires. The YT represents your claim on all yield generated until maturity. Both tokens trade freely on Pendle's specialised AMM, and their combined value always equals your underlying asset.

The mechanics work through a standardised yield token (SY) wrapper that normalises different yield-bearing assets into a common interface. When you wrap stETH into SY-stETH and split it, Pendle's smart contracts track yield accrual and distribute it to YT holders in real time. At maturity, you redeem your PT tokens for the underlying principal.

Pendle AMM Design and Pricing Mechanics

Pendle's AMM uses a modified constant-product formula specifically designed for yield trading. Unlike Uniswap that prices two independent assets, Pendle's AMM prices PT against its underlying with the knowledge that PT converges to face value at maturity. This time-decay awareness reduces your impermanent loss compared to standard AMM designs. You can derive the implied yield rate from the PT discount — for example, if PT-stETH trades at 0.965 ETH with six months to maturity, your implied fixed yield is approximately 7% annualised.

Supported Yield-Bearing Assets on Pendle

As of early 2026, Pendle supports a broad range of yield-bearing assets across multiple chains, and you should focus on the most liquid markets first. The most liquid options include stETH and wstETH from Lido, eETH from Ether.fi, sDAI from MakerDAO, GLP from GMX, and various Aave and Compound lending positions. Each asset has multiple maturity dates, typically ranging from one month to one year, giving you flexibility to match your investment horizon.

Your choice of underlying asset significantly affects your strategy. Stablecoin-based markets like sDAI suit predictable yields with minimal price risk, while ETH-based markets like stETH provide higher yields but expose your principal to ETH price movements. Select underlying assets that align with your existing portfolio exposure rather than taking on unintended directional bets.

Maturity Mechanics and Rollover Strategies

Every Pendle market has a fixed maturity date. At maturity, PT holders redeem tokens for the underlying asset at a 1:1 ratio, and YT holders receive any final yield distribution. After maturity, the market closes, so you must plan your exit or rollover beforehand. Rollover strategies involve closing your position in an expiring market and opening a new one in a later-dated market, with costs depending on the yield curve shape across maturities.

- Principal Tokens (PT) provide fixed-rate yield exposure with predictable returns

- Yield Tokens (YT) enable leveraged yield speculation without liquidation risk

- Pendle AMM uses time-decay pricing that converges PT to face value at maturity

Principal Token Strategies: Locking in Fixed Rates

Purchasing PT is the simplest and most conservative Pendle strategy available to you. When you buy PT at a discount to the underlying asset, you effectively lock in a fixed yield equal to that discount annualised over the remaining time to maturity. This is conceptually similar to buying a zero-coupon bond in traditional finance — you pay less than face value today and receive the full face value at maturity.

For example, if you buy PT-stETH at 965 ETH per 1,000 ETH face value with six months to maturity, your fixed yield is approximately 7% annualised. Regardless of whether stETH's variable staking yield rises to 8% or falls to 2% over those six months, your return stays locked. This certainty should appeal to you if your priorities include treasury management, risk-averse allocations, and hedging against yield compression.

Fixed-Income Strategies with PT

You can construct a fixed-income portfolio entirely within DeFi using PT positions across different underlying assets and maturities. A diversified PT portfolio might include PT-stETH for ETH-denominated fixed yield, PT-sDAI for USD-denominated fixed yield, and PT-GLP for higher-risk fixed yield with exposure to GMX trading fees. By laddering maturities — holding PTs expiring at one month, three months, and six months — you create regular redemption events that provide liquidity and opportunities to reinvest at prevailing rates.

You should recognise that the key risk with PT strategies is opportunity cost. If variable yields spike significantly above your locked rate, you miss the upside. However, this is precisely the trade-off that makes PT attractive — you sacrifice potential upside for downside protection. In volatile yield environments, the certainty premium of PT positions can be substantial.

PT Arbitrage and Discount Opportunities

PT occasionally trades at discounts that exceed fair value due to temporary liquidity imbalances. When the implied yield on PT significantly exceeds the historical average yield of the underlying asset, you should investigate whether it represents an arbitrage opportunity. Monitor the spread between PT implied yields and underlying asset historical yields across all Pendle markets — sudden spikes typically represent temporary dislocations that revert.

Using PT as Collateral in Lending Protocols

Several lending protocols now accept Pendle PT as collateral, enabling leveraged fixed-yield strategies. By depositing PT-stETH as collateral, borrowing ETH, and purchasing more PT-stETH, you can amplify your fixed yield exposure. The net yield equals your PT fixed rate multiplied by your leverage minus the borrowing cost. You must carefully manage your health factor — maintain conservative leverage ratios of 2-3x with health factors above 1.5 to provide a reasonable buffer against yield volatility.

Yield Token Strategies: Speculating on Variable Rates

Yield Tokens represent the opposite side of the yield tokenisation spectrum from your perspective. When you purchase YT, you are buying the right to receive all yield generated by the underlying asset from now until maturity. YT is inherently leveraged — a small capital outlay gives you yield exposure on a much larger notional amount. If the underlying asset yields more than the market expected when you purchased the YT, your returns are amplified. If yields disappoint, your YT can expire worthless.

The leverage embedded in YT comes from its pricing structure. If PT trades at 96% of face value, YT trades at roughly 4% — giving you exposure to all yield on 1 ETH for a fraction of the cost. Should the asset yield 5% over the remaining period, you receive more than your initial YT investment, delivering a 25% return on your capital. This leverage works in both directions, making YT suitable only if you have strong yield conviction.

Yield Speculation and Directional Bets

YT enables you to express directional views on yield rates without holding the underlying asset. If you believe Ethereum staking yields will increase due to rising network activity and MEV opportunities, buying YT-stETH gives you leveraged exposure to that thesis. Conversely, if you hold stETH and want to hedge against yield decline, selling YT (or equivalently, buying PT) locks in your current yield expectations.

The most profitable YT trades occur when you correctly anticipate yield regime changes — before major protocol upgrades, governance votes that redirect emissions, or macroeconomic shifts. Participants who position in YT before these events capture outsized returns. However, timing yield movements is extremely difficult, and you should size YT positions as speculative allocations rather than core holdings.

YT as an Income Stream

Unlike PT which pays at maturity, YT distributes yield continuously as it accrues, creating a real-time income stream. For income-focused strategies, compare the cost of YT against expected total yield over the remaining period. If YT-sDAI costs 2% of the underlying exposure with three months to maturity, you need the underlying to yield more than 8% annualised to break even. Build a margin of safety by only purchasing YT when your expected yield exceeds the break-even rate by at least 20-30%.

Providing Liquidity for YT Markets

Pendle's AMM requires liquidity providers to facilitate YT trading. Your LP positions earn trading fees plus PENDLE incentives directed by vePENDLE governance. The impermanent loss profile differs from standard AMMs because the time-decay-aware pricing curve reduces divergence loss as maturity approaches. The combination of trading fees, PENDLE emissions, and reduced impermanent loss can produce attractive risk-adjusted returns, especially in the most liquid stETH and sDAI markets.

ve-Tokenomics: Vote-Escrow Governance and Boosted Rewards

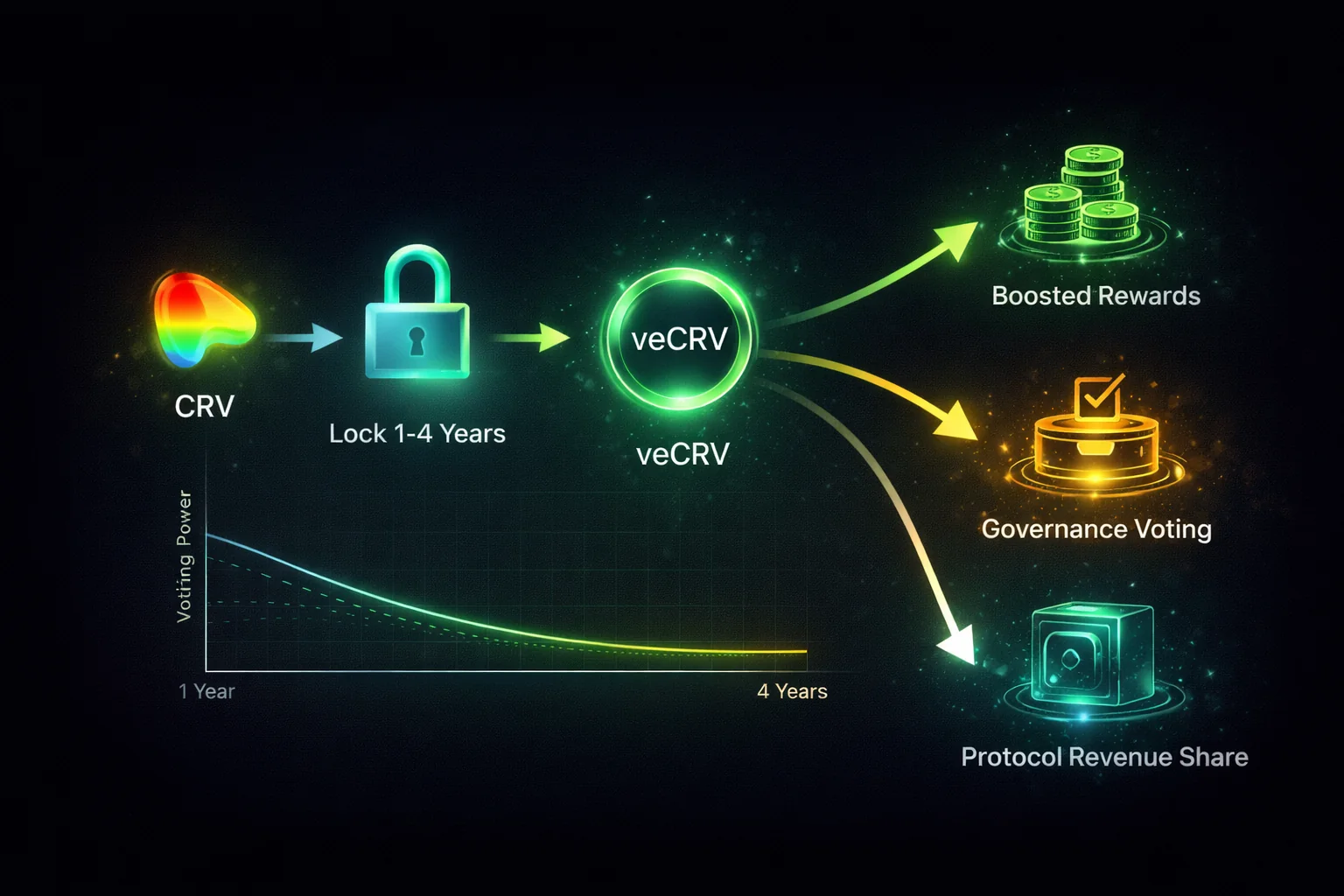

Vote-escrow tokenomics represent one of the most successful incentive alignment mechanisms in DeFi, and you should understand how the model works before committing capital. Pioneered by Curve Finance with veCRV, it requires you to lock governance tokens for a fixed period to receive voting power and boosted rewards, solving the fundamental problem of governance token sell pressure by creating genuine utility for holding and locking your tokens. For a comprehensive deep dive, see our dedicated ve-tokenomics explained guide.

The core mechanism works as follows: you lock your governance tokens (CRV, PENDLE, or BAL) for a period ranging from one week to four years, and longer locks grant you proportionally more voting power. This voting power serves two purposes — directing protocol emissions towards specific liquidity pools through gauge voting, and earning you a share of protocol trading fees. Your voting power decays linearly as your lock approaches expiry, incentivising you to extend your lock or accept diminishing influence.

veCRV: The Original Vote-Escrow Model

Curve Finance's veCRV system remains the benchmark for ve-tokenomics. When you lock CRV for four years, you receive the maximum veCRV balance, granting up to two-and-a-half times boost on your CRV rewards from Curve pools. Without the boost, your farming yields can be 60% lower than boosted participants. The gauge voting mechanism lets you direct CRV emissions towards specific Curve pools each week, creating a competitive dynamic where protocols actively seek your veCRV voting power. You also earn a share of all trading fees generated across Curve's pools, distributed weekly in 3CRV — real yield from actual trading activity.

vePENDLE: Yield Market Governance

When you lock PENDLE tokens, you gain voting power to direct PENDLE incentives towards specific yield markets. Markets that receive more vePENDLE votes attract higher PENDLE emissions, increasing the effective APY for liquidity providers. As a vePENDLE holder, you also receive a share of yield trading fees generated across all Pendle markets, adding 5-12% annualised on top of your base PENDLE rewards. Directing incentives to markets where you provide liquidity creates a powerful flywheel that compounds your returns from multiple sources.

veBAL: Balancer Governance and 80/20 Pools

veBAL requires you to lock an 80/20 BAL/ETH LP token rather than the governance token alone, reducing the pure governance token concentration risk present in veCRV and vePENDLE. The veBAL ecosystem is smaller, which means less competition for voting power — if you lock $5,000 in veBAL, your proportional voting influence is typically greater than the same amount locked in veCRV, potentially providing better bribe returns per dollar locked.

- Vote-locking CRV for veCRV provides boosted rewards up to 2.5x on Curve pools

- vePENDLE holders direct PENDLE emissions to specific yield markets via gauge voting

- Bribe markets on platforms like Votium and Hidden Hand monetise voting power

Bribe Markets and Vote Incentive Ecosystems

How can you earn extra yield simply by voting? Bribe markets emerged as a natural extension of ve-tokenomics, creating a secondary market for your voting power. Protocols and DAOs that want to attract liquidity to their pools pay you to vote for their gauges. These payments, commonly called bribes or vote incentives, represent an additional yield layer on top of your base ve-token rewards.

Votium, Hidden Hand, and Paladin

Which bribe platform should you use? Votium focuses primarily on veCRV and vlCVX, processing millions of dollars in weekly bribes from protocols seeking your Curve gauge votes. Hidden Hand serves a broader ecosystem including veCRV, veBAL, and several smaller ve-token systems. Paladin offers something different — a lending market for your voting power, allowing you to delegate votes in exchange for yield without transferring token custody.

You can understand the economics through a straightforward calculation. A protocol estimates the CRV emissions required to attract liquidity, then determines the cost of bribing enough veCRV holders to direct those emissions. You profit when bribe payments exceed the opportunity cost of directing your votes to a specific gauge.

Calculating Bribe Yield and Optimal Voting

Your bribe yield depends on the ratio of total bribes offered to total voting power directed at each gauge. Direct your votes to the highest-paying gauges each voting period. Bribe yields for veCRV holders typically range from 10-30% annualised on the value of locked CRV, varying with market conditions. Track historical bribe yields on Llama Airforce and DefiWars to time your locking decisions.

Risks and Considerations in Bribe Markets

Smart contract risk exists in the bribe platforms themselves — verify audit status before depositing. Governance attack risk arises when a single entity accumulates enough voting power to manipulate emissions. You should also consider bribe yield sustainability — protocols paying bribes from treasury reserves will eventually exhaust their budgets. Sustainable bribe demand comes from protocols with genuine need for liquidity, such as stablecoin issuers and lending protocols.

Auto-Compounding and Yield Aggregation Protocols

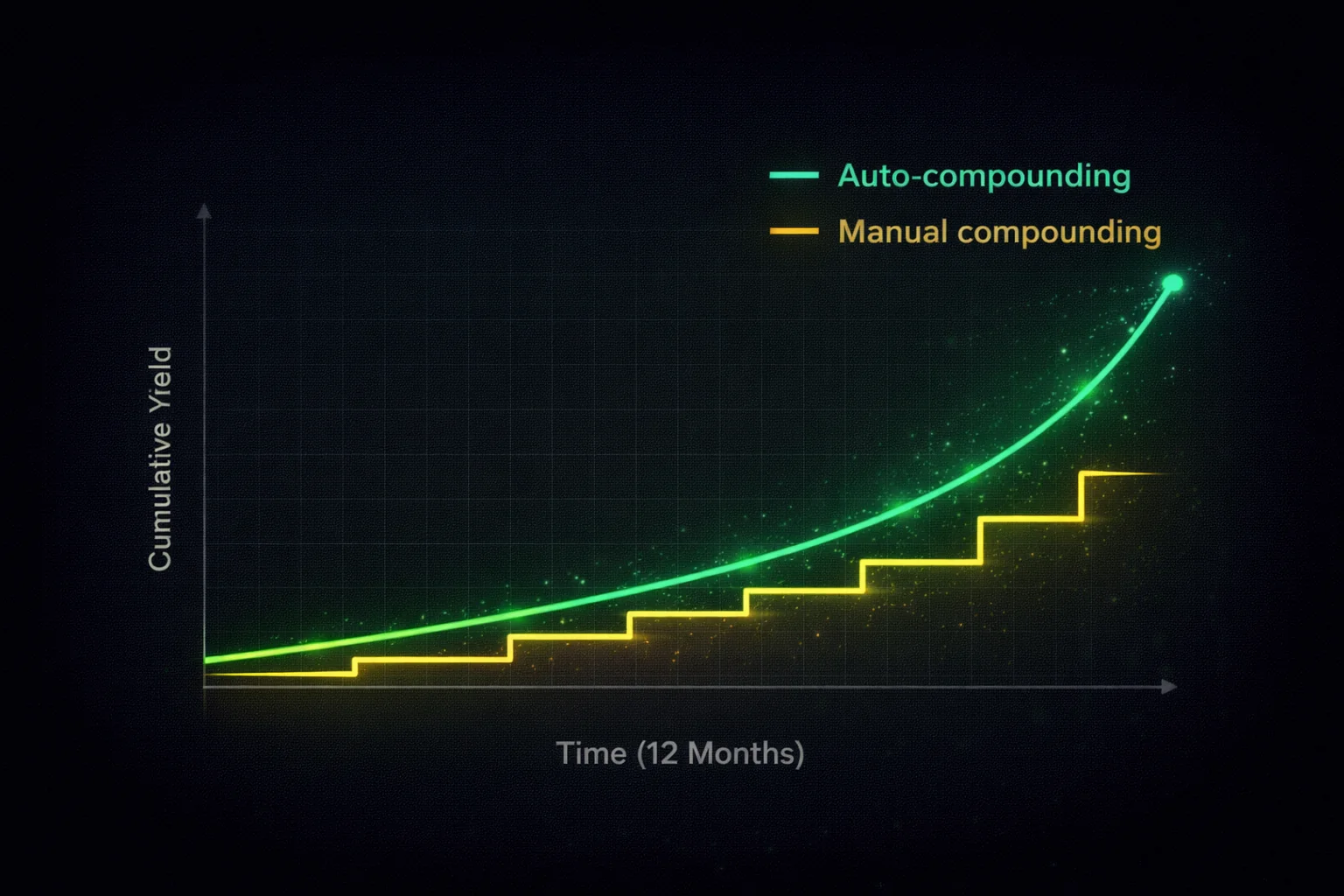

Auto-compounding protocols automate the process of harvesting earned rewards and reinvesting them back into yield-generating positions. This automation converts simple interest into compound interest, significantly boosting effective returns over time. For a detailed exploration of auto-compounding mechanics and yield aggregator architecture, see our auto-compounding and yield aggregation guide.

How much difference does auto-compounding make for your returns? Consider a position earning 20% APR with no compounding — it returns exactly 20% over one year. With daily compounding, your effective APY jumps to roughly 22% annually. At higher base rates, the advantage grows dramatically for you: 50% APR becomes approximately 65% APY with daily compounding. For example, if you deposit $50,000 at 50% APR, daily compounding earns you an extra $7,450 compared to simple interest over one year.

You cannot compound manually without significant cost because each harvest-and-reinvest cycle requires a blockchain transaction with associated gas costs. If your position earns $10 per day in rewards but each harvest costs $5 in gas, daily compounding destroys half your yield. Auto-compounding protocols solve this problem for you by batching harvests across all depositors, spreading gas costs over a much larger capital base.

Optimal Compounding Frequency

Your optimal compounding frequency balances the mathematical benefit of more frequent compounding against the gas cost of each harvest transaction. On Ethereum mainnet, harvesting every 4-12 hours is typical. On Layer 2 networks like Arbitrum where gas costs are orders of magnitude lower, harvesting can occur every few minutes. The advertised APY on auto-compounding vaults already accounts for the compounding effect — the underlying APR before compounding is lower.

Yield Aggregator Architecture

Modern yield aggregators like Yearn Finance operate through a vault-strategy architecture. When you deposit into a vault, your capital is deployed across one or more strategies — modular smart contracts that interact with external protocols. The vault controller can reallocate your capital between strategies to optimise returns. Strategy diversification reduces the impact of any single protocol failure, automated rebalancing captures yield opportunities you would miss manually, and gas cost socialisation makes sophisticated strategies economical even for smaller deposits.

- Yearn vaults auto-compound harvested rewards back into the base asset

- Convex aggregates veCRV voting power to provide maximum boost without individual locks

- Gas-optimised compounding frequency depends on TVL and reward accumulation rate

Yearn Finance V3 Vault Architecture

Why should you consider Yearn Finance for yield aggregation? Yearn has established itself as the leading yield aggregator in DeFi, and its V3 vault architecture represents a significant evolution from earlier versions. When you deposit into a V3 vault, your capital is deployed across multiple independent strategies simultaneously, with automated rebalancing based on real-time yield performance. For a comprehensive review of Yearn's platform, security history, and fee structure, see our Yearn Finance review.

How does the V3 architecture work for you? It separates the vault contract (handling your deposits, withdrawals, and accounting) from the strategy contracts (interacting with external protocols to generate yield). This separation allows strategy developers to create and deploy new strategies without modifying the core vault logic. Each strategy has a configurable debt ratio that determines what percentage of your vault assets it can deploy, and management adjusts these ratios to respond to changing market conditions.

Strategy Types and Yield Sources

Yearn V3 vaults access multiple strategy types: lending strategies deploy assets into Aave and Compound for borrowing interest, liquidity provision strategies deploy capital into Curve and Balancer pools for trading fees, and governance farming strategies accumulate locked governance tokens for boosted rewards and bribe income. The most sophisticated strategies combine multiple yield sources — for example, depositing stablecoins into a Curve pool, staking LP tokens on Convex for boosted CRV and CVX rewards, harvesting periodically, and redepositing the proceeds.

Fee Structure and Net Returns

Yearn V3 charges a 10% performance fee on generated yield, with no management fee on deposited assets and no deposit or withdrawal fees. If a vault produces 10% gross APY, the effective cost is 1 percentage point, leaving you with 9% net. For complex multi-protocol strategies involving multiple harvest cycles and gas optimisation, Yearn's automation typically delivers higher net returns than manual execution, even after this fee.

Risk Profile and Security Considerations

Yearn's risk profile is a composite of the vault contract risk and the individual strategy risks. The vault contracts have been extensively audited and battle-tested with billions in deposits. Strategy contracts carry additional risk because they interact with external protocols — a vulnerability in Aave or Curve could affect your Yearn position even if Yearn's own contracts are secure. Yearn mitigates this through strategy debt limits (no single strategy receives more than 20-40% of vault assets), emergency withdrawal functions, and continuous security monitoring.

Convex Finance: Democratising CRV Boost

Convex Finance solves a fundamental problem you face in the Curve ecosystem: earning maximum CRV rewards requires locking substantial CRV as veCRV, which is impractical for most liquidity providers. For a $100,000 Curve LP position, you might need $50,000 or more in locked CRV to achieve maximum boost. Convex aggregates CRV from many users, locks it as veCRV, and passes the boosted rewards back to you. For a detailed analysis, see our Convex Finance review.

The protocol operates through a straightforward mechanism that you can understand in three steps. You deposit your Curve LP tokens into Convex, which stakes them on Curve using its massive veCRV position to earn boosted CRV rewards. In return, you receive the boosted CRV rewards minus Convex's platform fee, plus additional CVX token incentives. The net effect is that you earn significantly more than you would by staking directly on Curve without your own veCRV position.

cvxCRV Staking and CRV Conversion

If you hold CRV tokens and want to earn yield without providing liquidity, Convex offers the cvxCRV staking option. When you deposit CRV into Convex, it is permanently converted to cvxCRV — a liquid wrapper that represents CRV locked as veCRV within Convex's system. Staked cvxCRV earns a share of Convex's veCRV rewards including Curve trading fees, a portion of CRV farming rewards, and additional CVX incentives. The permanent conversion is important — you can sell cvxCRV on secondary markets, but it typically trades at a slight discount to CRV.

vlCVX: Vote-Locked CVX Governance

Convex's own governance token CVX can be vote-locked as vlCVX, granting you the ability to direct Convex's massive veCRV voting power. Since Convex controls over 50% of all veCRV, vlCVX is one of the most powerful governance positions in DeFi. Bribe yield on vlCVX has historically ranged from 15-25% annualised during periods of high demand. The lock period is 16 weeks plus 3 days — significantly shorter than veCRV's maximum four-year lock. For a detailed analysis, see our Convex Finance review.

Convex versus Direct Curve Staking

If you hold enough veCRV to achieve maximum boost on your LP positions, direct staking avoids Convex's platform fee and gives you full control over gauge votes. If you lack sufficient veCRV for maximum boost — which is the case for most individual users — Convex provides higher net returns despite its fee because the boosted rewards exceed what you could earn unboosted.

Impermanent Loss Management for Yield Optimisers

Impermanent loss remains the most misunderstood and underestimated risk you face in yield optimisation. Any strategy that involves providing liquidity to an AMM pool exposes you to impermanent loss — the difference between holding your assets and providing them as liquidity. For both the foundational concepts and advanced management techniques specific to yield optimisation contexts, see our dedicated impermanent loss management guide.

The magnitude of impermanent loss depends on the price divergence between assets in your pool and the pool's invariant curve design. How much IL should you expect? Standard constant-product AMMs like Uniswap V2 expose you to the highest IL for a given price movement. Curve's StableSwap invariant dramatically reduces your IL for assets that trade near parity. Pendle's time-decay-aware AMM reduces your IL for yield token trading by incorporating maturity convergence into its pricing.

IL in Curve StableSwap Pools

Curve's StableSwap invariant concentrates liquidity around the 1:1 peg, making it extremely capital-efficient for correlated asset pairs. For stablecoin pools, impermanent loss is negligible under normal conditions. For LST pools (stETH/ETH, rETH/ETH), IL is minimal as long as the LST maintains its peg. However, depeg events can cause significant IL — during the June 2022 stETH depeg, liquidity providers experienced meaningful losses as stETH traded at a 5-7% discount to ETH.

IL in Pendle AMM Positions

Pendle's AMM has a unique IL profile because PT prices converge to the underlying asset value at maturity. This convergence means IL from Pendle LP positions decreases as maturity approaches, regardless of yield rate movements. Pendle LP positions held to maturity experience less IL than equivalent positions in standard AMMs. Match your Pendle LP duration to your actual liquidity needs.

Hedging Strategies for IL Mitigation

Several approaches can reduce your IL exposure. Concentrated liquidity ranges on Uniswap V3 allow you to provide liquidity within a specific price range. Options protocols like Lyra and Premia offer put options that can hedge against adverse price movements. Delta-neutral strategies combine LP positions with short perpetual positions to offset directional exposure. For most yield optimisers, the simplest approach is providing liquidity to pools of highly correlated assets — stablecoin pairs, LST/ETH pairs, or wrapped/unwrapped token pairs. For advanced techniques, see our impermanent loss management guide.

Risk Framework for Yield Optimisation

Every yield optimisation strategy carries risks that you must systematically evaluate before committing capital. The DeFi yield space has experienced numerous incidents — from the Cream Finance exploits to the Curve pool reentrancy vulnerability in 2023 — that demonstrate how quickly positions can lose value. A structured risk framework helps you identify, quantify, and mitigate these risks across your portfolio.

Smart Contract Risk Assessment

Smart contract risk is the foundational risk in all DeFi yield strategies. Evaluate smart contract risk along several dimensions: audit history, time in production, total value locked, bug bounty programmes, and code complexity. Multi-protocol strategies compound smart contract risk — if your strategy involves Curve, Convex, and Aave simultaneously, you face vulnerabilities in all three protocols. Limit your strategy complexity to the minimum number of protocol interactions needed to achieve your target yield.

Governance and Centralisation Risk

Many DeFi protocols retain administrative functions that can modify protocol parameters, upgrade contracts, or pause operations. Before committing capital, review the governance structure of every protocol in your yield strategy — verify who controls the admin keys, what timelock delay exists, and whether there is an emergency multisig. Favour protocols with longer timelocks and distributed multisig signers.

Liquidity and Exit Risk

Some yield strategies involve locking your capital for fixed periods or depositing into positions with limited exit liquidity. Your veCRV locks can last up to four years with no early withdrawal. Pendle PT positions are liquid on the AMM but may experience slippage during market stress. Always model your worst-case exit scenario before entering a position — never lock capital that you may need before the lock expires.

Composability and Cascade Risk

DeFi's composability creates cascade risk where a failure in one protocol propagates through interconnected positions. Map the dependency chain of your yield strategies and identify single points of failure — specific stablecoins, oracles, or bridges. Diversifying across independent protocol stacks provides the most robust protection against cascade failures.

Portfolio Construction and Capital Allocation

How should you structure your yield capital? You need a portfolio approach rather than concentrating capital in a single strategy. Your allocation should reflect your risk tolerance, time horizon, liquidity needs, and the correlation between different yield sources. A well-constructed yield portfolio balances your high-conviction positions with diversification across protocols, chains, and strategy types.

Core-Satellite Allocation Framework

A practical framework divides your yield capital into core and satellite allocations. Your core allocation (60-70% of capital) should be deployed in lower-risk, higher-liquidity strategies that provide stable base returns. Examples include stablecoin lending on Aave, Curve stablecoin LP positions auto-compounded through Yearn, and PT positions on Pendle for fixed-rate exposure. These positions form your yield foundation and should be resilient to moderate market stress.

Your satellite allocation (30-40% of capital) targets higher returns through more aggressive strategies. Examples include YT speculation on Pendle, ve-token locking for bribe income, leveraged LP positions, and newer protocol opportunities. These positions carry higher risk but also higher return potential. You should be prepared to lose your entire satellite allocation without affecting your financial stability or core yield generation.

Diversification Across Multiple Dimensions

Diversify your yield capital across several dimensions: protocol diversification limits single-protocol exposure, chain diversification deploys capital across Ethereum mainnet, Arbitrum, and Optimism, strategy diversification combines lending, LP provision, governance farming, and yield tokenisation, and asset diversification uses both stablecoin-denominated and ETH-denominated positions. Set maximum allocation limits per protocol (no more than 20-25%), per chain (no more than 50%), and per strategy type (no more than 40%).

Rebalancing and Ongoing Monitoring

Your yield portfolio requires regular monitoring because yield rates change constantly. Review your portfolio at least weekly, comparing current yields against your target returns. Key rebalancing triggers include yield dropping below your minimum acceptable rate, protocol security incidents, significant TVL changes, and new opportunities with better risk-adjusted returns.

Yield Strategy Comparison Overview

The following table summarises the key characteristics of the major yield optimisation strategies covered in this guide, helping you compare risk-return profiles at a glance.

| Strategy | Typical APY Range | Risk Level | Liquidity | Complexity | Min Capital |

|---|---|---|---|---|---|

| Pendle PT (fixed yield) | 4-12% | Low-Medium | High (AMM) | Low | $500+ |

| Pendle YT (yield speculation) | -100% to 200%+ | High | High (AMM) | Medium | $1,000+ |

| veCRV locking + bribes | 10-30% | Medium | Low (4yr lock) | Medium | $5,000+ |

| Convex LP staking | 5-20% | Low-Medium | High | Low | $500+ |

| Yearn V3 vaults | 3-15% | Low-Medium | High | Low | $100+ |

| Curve stablecoin LP | 3-10% | Low | High | Low | $500+ |

| Leveraged PT strategies | 8-25% | High | Medium | High | $10,000+ |

| Pendle LP provision | 8-25% | Medium | High | Medium | $2,000+ |

Conclusion

Yield optimisation in 2026 rewards you when you combine technical understanding with disciplined risk management. The three pillars covered here — yield tokenisation through Pendle, ve-tokenomics governance across Curve, Pendle, and Balancer, and automated aggregation through Yearn and Convex — represent the most battle-tested approaches to generating sustainable DeFi returns. How should you combine them? Build your core around real yield sources and treat inflationary incentives as temporary bonuses.

You should approach yield optimisation as an ongoing practice. Market conditions, protocol parameters, and governance decisions evolve continuously. Start with simpler strategies — Yearn vaults, Curve stablecoin LP, Pendle PT positions — and progressively add complexity as your understanding deepens. Size your positions conservatively, diversify across protocols and chains, and never allocate more than you can afford to lose. If yield optimisation is your first crypto-side income exposure, our passive income foundations before optimisation tactics covers the savings-budget, custody and risk-tolerance decisions this hub assumes are already settled.

For deeper exploration, our satellite guides cover each area comprehensively. See our Pendle yield tokenisation guide, our ve-tokenomics guide, our auto-compounding guide, and our Pendle vs Yearn vs Convex comparison.

From the yield tokenisation pillar, your key takeaway is that yield is no longer a fixed attribute of a position — it is a tradeable asset. Pendle PT positions give you fixed-rate certainty comparable to traditional bonds, while YT positions let you express directional views on yield with built-in leverage. The ability to separate principal risk from yield risk fundamentally expands your strategic toolkit beyond what was possible with first-generation yield farming.

From the ve-tokenomics pillar, remember that governance participation is not merely a philosophical commitment to decentralisation — it is a concrete yield source. Bribe income on veCRV and vlCVX has consistently delivered 10-30% annualised returns, and vePENDLE holders earn a share of all yield trading fees across Pendle markets. The protocols that reward long-term commitment through vote-escrow mechanics have demonstrated the strongest resilience across market cycles, precisely because their incentive structures discourage short-term speculation.

From the aggregation pillar, the practical lesson is that automation and gas optimisation matter enormously for your net returns. Yearn V3 vaults and Convex boosted staking handle the operational complexity of multi-protocol strategies, compounding rewards at optimal frequencies and socialising gas costs across all depositors. For most participants, the net yield after Yearn's performance fee or Convex's platform fee exceeds what you could achieve through manual execution.

Risk management ties all three pillars together. Diversify across protocols, chains, and strategy types. Set maximum allocation limits per protocol at 20-25% of your yield capital. Maintain a core-satellite structure where 60-70% of your capital sits in lower-risk positions like stablecoin lending, Curve LP, and Pendle PT, while 30-40% targets higher returns through YT speculation, ve-token locking, and newer opportunities. Review your portfolio weekly, and be prepared to exit positions quickly when risk parameters change. The yield optimisation landscape in 2026 rewards disciplined, informed participants who treat DeFi yield as a serious practice rather than a passive activity. Your edge comes not from chasing the highest advertised APY, but from understanding the mechanics behind each yield source and sizing your positions according to the risks you can genuinely afford to take.

Sources and References

- Pendle Finance — Official Documentation

- Curve Finance — veCRV (Voting Escrow) Documentation

- Yearn Finance — V3 Vault Documentation

- Convex Finance — Protocol Documentation

- DefiLlama — DeFi Yield Dashboard and TVL Analytics

- Hardware Wallet Security Guide - Protect yield positions with hardware wallet signing

Frequently Asked Questions

- What is yield tokenisation and how does Pendle enable it?

- Yield tokenisation is the process of splitting a yield-bearing asset into two separate components: a Principal Token (PT) that represents the underlying capital and a Yield Token (YT) that represents the future yield stream. Pendle Finance pioneered this approach in DeFi, allowing users to trade these components independently on its specialised AMM. PT holders lock in a fixed yield by purchasing the principal at a discount, while YT holders speculate on variable yield rates. This separation enables strategies impossible with traditional yield farming, such as hedging yield exposure or leveraging yield expectations without additional capital risk.

- How do ve-tokenomics models like veCRV and vePENDLE work?

- Vote-escrow tokenomics require users to lock governance tokens for a fixed period to receive voting power and boosted rewards. In the veCRV model, locking CRV tokens for up to four years grants maximum voting power to direct gauge emissions towards specific liquidity pools, earning boosted CRV rewards of up to 2.5x. vePENDLE follows a similar structure where locked PENDLE directs incentives to specific yield markets. Voting power decays linearly as the lock period approaches expiry, incentivising longer commitments. Bribe markets like Votium and Hidden Hand have emerged where protocols pay ve-token holders to vote for their pools, creating an additional yield layer.

- What is auto-compounding and why does it improve yield?

- Auto-compounding automatically harvests earned rewards and reinvests them back into the same yield-generating position at regular intervals. This converts simple interest into compound interest, significantly boosting effective APY over time. For example, a position earning 20% APR with daily compounding produces approximately 22.1% APY. Protocols like Yearn Finance automate this process through vault strategies that batch harvests across all depositors, spreading gas costs and optimising harvest timing. Without auto-compounding, users must manually claim and reinvest rewards, paying individual gas fees each time and often missing optimal compounding intervals.

- What is the difference between real yield and inflationary yield?

- Real yield comes from genuine economic activity such as trading fees, borrowing interest, and protocol revenue that is distributed to participants. Inflationary yield comes from newly minted governance tokens distributed as incentives, which dilute existing token holders. Real yield is sustainable because it reflects actual demand for the protocol's services, while inflationary yield depends on continued token emissions and can collapse when incentive programmes end or token prices decline. In 2026, protocols generating real yield include Curve Finance through trading fees, Pendle through yield trading fees, and GMX through perpetual trading fees. You should prioritise strategies built on real yield foundations.

- How does Convex Finance boost Curve yields without locking CRV?

- Convex Finance aggregates CRV deposits from many users and locks them as veCRV to achieve maximum boost on Curve liquidity pools. Individual liquidity providers deposit their Curve LP tokens into Convex and receive boosted CRV rewards plus CVX token incentives without needing to lock any CRV themselves. Convex holds over 50% of all veCRV supply, giving it enormous voting power to direct Curve emissions. Users who deposit CRV into Convex receive cvxCRV, a liquid wrapper that earns a share of Convex platform fees, veCRV rewards, and additional CVX incentives. This model democratises access to boosted yields that would otherwise require substantial individual CRV holdings.

- What are the main risks of DeFi yield optimisation strategies?

- The primary risks include smart contract vulnerabilities, impermanent loss from volatile trading pairs, governance attacks, oracle manipulation, and composability risk where failures cascade through interconnected positions. Ve-token locking also creates illiquidity risk since locked tokens cannot be withdrawn early. You should diversify across multiple protocols, start with small positions, use only audited protocols, and never allocate more than you can afford to lose.

- Can beginners use yield optimisation strategies safely?

- Yes, but you should start simple and add complexity gradually. First, deposit stablecoins into Aave for 3-5% APY to learn DeFi mechanics. Next, try auto-compounding vaults on Yearn Finance. Then explore Curve stablecoin LP with minimal impermanent loss. Only after several months of experience should you consider ve-tokenomics, Pendle yield tokenisation, or multi-protocol strategies.

- What tools should I use to monitor my yield positions?

- DefiLlama provides comprehensive yield monitoring with APY data across hundreds of protocols. Zapper and DeBank consolidate your positions into a single portfolio view. For Pendle, use the official dashboard for implied yield rates and PT discounts. For ve-tokenomics, check Votium and Hidden Hand dashboards for bribe income tracking. You should review your positions at least weekly.

- How much capital do you need to start yield optimisation?

- You can begin with as little as $500 on Layer 2 networks like Arbitrum or Optimism where gas costs are minimal. Yearn V3 vaults accept deposits from $100, and Pendle PT positions on Arbitrum are practical from $500. However, certain strategies require more capital to be economical — veCRV locking with meaningful bribe income typically needs $5,000 or more in CRV, and leveraged PT strategies on Ethereum mainnet require $10,000 or more to justify the gas costs of multiple transactions. Start on Layer 2 with simple vault deposits, then scale to mainnet strategies as your capital and experience grow. The core-satellite framework works at any scale: allocate 60-70% to stable yield sources and 30-40% to higher-return opportunities regardless of your total portfolio size.

- What is the difference between APR and APY in DeFi yield contexts?

- APR (Annual Percentage Rate) represents the simple interest rate over one year without accounting for compounding — if you earn 20% APR, you receive exactly 20% of your principal over twelve months. APY (Annual Percentage Yield) includes the effect of compounding, where earned rewards are reinvested to generate additional returns. The same 20% APR becomes approximately 22.1% APY with daily compounding because each day's rewards earn their own rewards for the remainder of the year. The gap between APR and APY widens at higher rates and more frequent compounding intervals. When comparing yield opportunities, always check whether the quoted figure is APR or APY — protocols sometimes advertise APY to make yields appear higher. Auto-compounding vaults like Yearn typically quote APY since compounding is built into the vault mechanics, while lending protocols like Aave often quote APR for their base supply rates.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.