ve-Tokenomics Explained

Understand vote-escrow tokenomics across Curve, Pendle, and Balancer. Analyse lock mechanics, gauge voting strategies, bribe markets, and liquid wrapper protocols for maximising governance yields in 2026.

Introduction: The ve-Token Revolution in DeFi Governance

Vote-escrow tokenomics — commonly called ve-tokenomics — has become the dominant governance model across major DeFi protocols. Pioneered by Curve Finance with veCRV in 2020, the model requires users to lock governance tokens for extended periods to receive voting power, boosted rewards, and protocol revenue sharing. The elegance of the ve-model lies in its economic alignment — by requiring participants to lock tokens for up to four years, the system ensures that governance decisions are made by stakeholders with genuine long-term commitment to the protocol's success rather than short-term speculators seeking to extract value.

This lock-based alignment mechanism has proven remarkably resilient across multiple market cycles, maintaining robust protocol stability even during severe bear market conditions when unlocked governance tokens would typically have been sold aggressively. By 2026, ve-tokenomics still governs the majority of governance-locked DeFi TVL across Curve, Balancer, and dozens of protocols that adopted the framework — making it the most widely deployed and thoroughly battle-tested governance mechanism in decentralised finance, though no longer unchallenged.

A flagship adopter just left the model. Pendle Finance — historically one of the canonical ve-token implementations alongside Curve and Balancer — retired vePENDLE in January 2026 and migrated to sPENDLE, a 14-day liquid staking position that routes up to 80% of protocol revenue to PENDLE buybacks rather than distributing it directly to lockers. The ve-model is not dead, but the Pendle exit is the first time a top-tier adopter has concluded that the multi-year lock created more friction than alignment for its specific revenue profile. For DeFi participants evaluating ve-token strategies in mid-2026, this is the relevant context: ve-tokenomics remains dominant at Curve and Balancer, the vePENDLE technical descriptions later in this guide describe the prior mechanism that ran on Pendle until January 2026, and any new protocol picking a governance design is now weighing locks against liquid-staking alternatives like sPENDLE.

This guide provides a technical deep dive into how ve-token systems work, comparing the three most significant implementations: veCRV (Curve Finance), vePENDLE (Pendle Finance), and veBAL (Balancer). You will learn the lock mechanics, voting power decay mathematics, gauge voting strategies, and the bribe market ecosystems that have emerged around each system. Whether you are currently evaluating whether to lock tokens directly, use liquid wrappers like Convex or Aura, or participate in bribe markets as a voter, this guide provides the technical foundation for making informed decisions about ve-token participation. For the broader yield optimisation context, see our yield optimisation strategies hub.

The economic significance of ve-tokenomics extends well beyond governance. Locked tokens reduce circulating supply, creating natural buy pressure as protocols grow and more participants seek voting power. The gauge voting mechanism directs token emissions towards specific liquidity pools, creating a competitive market for liquidity incentives that has spawned an entire ecosystem of bribe platforms including Votium, Hidden Hand, and Paladin. These bribe markets allow protocols to pay ve-token holders to direct emissions towards their pools, effectively creating a marketplace for liquidity that operates through decentralised governance rather than centralised business development. Understanding how to navigate this ecosystem — when to lock, which gauges to vote for, and how to maximise bribe income — has become an essential skill for DeFi participants seeking to optimise their yield across ve-tokenomics protocols in 2026.

Core ve-Token Lock Mechanics

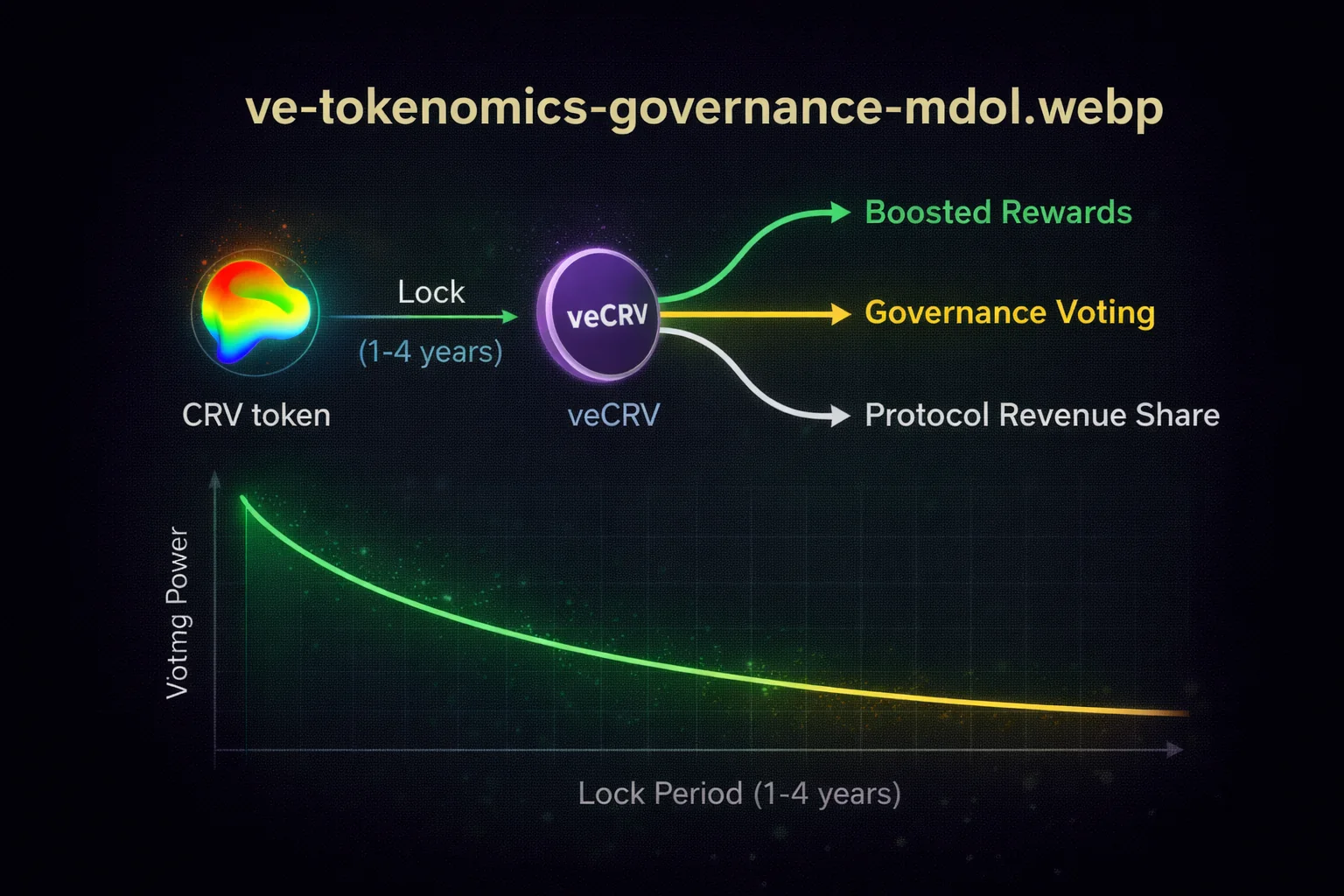

All ve-token systems share a common foundation: users lock governance tokens for a chosen duration and receive a non-transferable voting token whose balance determines their governance power, reward boost, and revenue share. The longer the lock, the more voting power you receive.

Lock Duration and Voting Power Calculation

The voting power formula is consistent across implementations: ve-balance equals the locked token amount multiplied by the remaining lock duration divided by the maximum lock duration. If you lock 1,000 CRV for four years (the maximum), you receive 1,000 veCRV. If you lock the same amount for two years, you receive 500 veCRV. This linear relationship between duration and power incentivises maximum-length locks.

Voting power decays linearly from the moment of locking. Your 1,000 veCRV from a four-year lock decreases by approximately 250 veCRV per year. After three years, you hold only 250 veCRV. At expiry, your balance reaches zero and you can withdraw the original 1,000 CRV. You can counteract decay by extending your lock at any time, which resets the decay curve based on the new end date.

Lock Irreversibility and Commitment Design

ve-token locks are irreversible by design. Once locked, tokens cannot be withdrawn before the lock period expires. This irreversibility is not a limitation but a core feature — it ensures that governance participants cannot exit their positions immediately after voting, forcing them to live with the consequences of their decisions. The commitment mechanism creates a natural filter where only participants with genuine long-term interest in the protocol's success acquire significant voting power.

Voting Power Decay Mathematics

The linear decay model means your effective governance influence diminishes predictably over time. Consider a practical example: locking 10,000 CRV for four years yields 10,000 veCRV initially. After one year, your balance drops to 7,500 veCRV. After two years, 5,000 veCRV remains. This decay affects both your gauge voting weight and your share of protocol fee distributions. Strategic participants monitor their decay schedules and extend locks periodically — typically when their voting power drops below 50% of maximum — to maintain meaningful governance influence without committing to perpetual maximum locks.

The decay mechanism also creates interesting market dynamics. Protocols seeking gauge votes prefer to bribe holders with longer remaining lock durations because those holders command more voting power per token locked. This creates a premium for freshly locked or recently extended positions in bribe markets, incentivising active lock management rather than passive holding.

Cross-Chain ve-Token Implementations

By 2026, several ve-token systems have expanded beyond Ethereum mainnet. Curve deployed gauge voting on Arbitrum, Optimism, and Polygon, allowing veCRV holders on mainnet to direct emissions across multiple chains through cross-chain messaging. Pendle operates natively on Ethereum and Arbitrum with separate vePENDLE instances on each chain. Balancer's veBAL system similarly spans multiple networks through Layer Zero cross-chain governance. These multi-chain deployments introduce additional complexity — you must decide which chain to lock on, considering gas costs, bribe availability, and the liquidity depth of pools on each network.

Protocol Fee Sharing Mechanics

Every ve-token system distributes a portion of protocol-generated fees to locked token holders. The distribution mechanics differ across implementations. Curve allocates 50% of trading fees as 3CRV tokens through weekly distributions, requiring holders to claim manually. Pendle distributes swap fees proportionally to vePENDLE balances with automatic accrual visible in the dashboard. Balancer routes 75% of protocol fees through the fee collector contract, distributing them as bb-a-USD (boosted Aave stablecoin pool tokens) to veBAL holders. Understanding these distribution mechanics matters because the fee token composition affects your portfolio exposure — receiving 3CRV gives stablecoin exposure, while receiving protocol-native fee tokens adds governance token correlation to your position.

Lock Extension Strategies and Timing

Extending your lock resets the decay curve and restores voting power without requiring additional token deposits. The optimal extension timing depends on your strategy. Passive holders typically extend when voting power drops below 60% of maximum, maintaining reasonable governance influence with minimal transaction frequency. Active bribe farmers extend more frequently — often monthly — because higher voting power translates directly to larger bribe allocations. Each extension transaction costs gas, so Ethereum mainnet participants should batch extensions with other on-chain activities. On Layer 2 networks where gas costs are negligible, weekly extensions become practical even for smaller positions.

- Maximum lock duration (4 years for veCRV) provides maximum voting power and fee share

- Voting power decays linearly over the remaining lock period towards zero at expiry

- Relocking or extending resets the decay curve and restores full voting power

veCRV: The Original Vote-Escrow System

Curve Finance launched veCRV in August 2020, creating the template that all subsequent ve-token systems follow. The system has three pillars: governance voting on gauge weights, boosted CRV rewards for liquidity providers, and protocol fee distribution to veCRV holders.

CRV Boost Mechanics

Liquidity providers on Curve earn base CRV rewards that can be boosted up to 2.5x based on their veCRV holdings relative to the total veCRV supply and the specific pool's liquidity. The boost formula considers your share of veCRV against your share of the pool's liquidity — holding a larger proportion of veCRV relative to your LP position yields a higher boost multiplier. Achieving maximum 2.5x boost on large positions requires substantial veCRV holdings, which is why aggregators like Convex Finance emerged to pool veCRV and share the boost across all depositors.

Protocol Fee Distribution

Curve distributes 50% of all trading fees to veCRV holders, paid in 3CRV (a stablecoin LP token representing DAI, USDC, and USDT). Fee distributions occur weekly and are proportional to your veCRV balance at the time of the snapshot. With Curve processing billions in monthly trading volume across hundreds of pools, the fee income provides a meaningful yield on locked CRV independent of CRV token price movements. In 2026, weekly fee distributions typically range from $2-5 million depending on market activity.

Governance Power and Gauge Weight Voting

veCRV holders vote bi-weekly on gauge weights, which determine how CRV emissions are distributed across Curve's liquidity pools. Pools that receive more gauge weight attract higher CRV rewards, which in turn attracts more liquidity and generates more trading fees. This creates a competitive dynamic where protocols and liquidity providers lobby for gauge votes to boost their preferred pools — the foundation of the bribe market ecosystem covered later in this guide.

veCRV Supply and Lock Statistics

As of early 2026, approximately 600 million CRV tokens are locked as veCRV, representing roughly 40% of the circulating CRV supply. The average lock duration exceeds three years, indicating strong long-term commitment from the holder base. Convex Finance controls the largest single veCRV position at over 300 million veCRV, followed by Yearn Finance and Stake DAO. Individual whale wallets holding more than one million veCRV number fewer than 200, demonstrating significant concentration of governance power amongst institutional-scale participants and aggregator protocols.

veCRV Smart Contract Whitelist System

Curve implements a whitelist mechanism that restricts which smart contracts can lock CRV as veCRV. Only contracts approved through Curve governance can create veCRV positions, preventing unauthorised protocols from building liquid wrappers or aggregation layers without community consent. This whitelist has historically been a contentious governance topic — new protocols seeking to build on veCRV must pass a governance vote, which established aggregators like Convex may oppose to protect their competitive position. The whitelist creates a meaningful barrier to entry for new liquid wrapper protocols and contributes to the concentration of veCRV amongst a small number of approved aggregators.

vePENDLE: Yield Market Governance

Pendle Finance adopted ve-tokenomics with vePENDLE, adapting the model for yield market governance. The maximum lock duration is two years (compared to Curve's four), reflecting the faster-moving nature of yield markets where conditions change more rapidly than in stablecoin liquidity provision.

vePENDLE Boost and Revenue Share

vePENDLE holders receive up to 2.5x boosted PENDLE rewards on their LP positions across Pendle's yield markets. The boost calculation mirrors veCRV's approach — your boost depends on your vePENDLE share relative to your LP share. Additionally, vePENDLE holders receive a share of Pendle's protocol revenue from swap fees across all markets. As Pendle's TVL and trading volume have grown substantially through 2025-2026, the revenue share has become an increasingly attractive component of the vePENDLE value proposition.

Yield Market Gauge Voting

vePENDLE holders vote weekly to direct PENDLE incentive emissions towards specific yield markets. Unlike Curve where gauges correspond to liquidity pools for different token pairs, Pendle's gauges correspond to yield markets for different underlying assets and maturity dates. This means voting decisions directly influence which yield-bearing assets attract the most liquidity on Pendle, shaping the protocol's market landscape. For a detailed guide on Pendle's yield tokenisation mechanics, see our Pendle yield tokenisation guide.

vePENDLE Expiry and Maturity Alignment

A distinctive feature of vePENDLE is the interaction between lock expiry and yield market maturity dates. Pendle's yield markets have fixed expiry dates, and the optimal vePENDLE lock duration should extend beyond the maturity of the markets you intend to provide liquidity for. If your vePENDLE lock expires before a yield market matures, you lose your boost on that market's LP rewards during the remaining period. Strategic participants align their vePENDLE lock expiry with the longest-dated yield market they actively participate in, then extend as new markets with later maturities launch.

vePENDLE Revenue Channels and Fee Structure

vePENDLE holders earn revenue through three distinct channels. First, they receive a proportional share of the swap fees generated across all Pendle yield markets — typically 0.1% to 0.35% per trade depending on the market. Second, they earn a portion of the yield accrued by expired Principal Tokens that remain unclaimed after maturity, creating a passive income stream from abandoned positions. Third, vePENDLE holders who actively vote on gauges receive bribe payments from protocols seeking to attract liquidity to their yield markets. The combined yield from these three channels typically ranges from 20% to 45% APR depending on market activity, bribe volumes, and the total vePENDLE supply. Monitoring each revenue channel separately helps you understand which component drives your returns and whether shifting your strategy between direct voting and bribe farming would improve your overall yield.

veBAL: Balancer Governance and Incentives

Balancer's veBAL system requires locking 80/20 BAL/WETH LP tokens (not raw BAL) for up to one year. This unique design ensures that veBAL holders maintain liquidity exposure alongside their governance commitment, aligning incentives between liquidity providers and governance participants more tightly than systems that lock raw governance tokens.

The 80/20 LP Lock Structure

To obtain veBAL, you first provide liquidity to Balancer's canonical 80% BAL / 20% WETH pool, receiving BPT (Balancer Pool Tokens). You then lock these BPT for your chosen duration up to one year. This structure means veBAL holders are simultaneously liquidity providers and governance participants, earning trading fees on the BAL/WETH pool while directing BAL emissions through gauge votes. The one-year maximum lock is shorter than veCRV's four years, reflecting Balancer's design philosophy of lower commitment barriers.

Balancer Ecosystem Integration

veBAL governs gauge weights across Balancer's diverse pool types including weighted pools, stable pools, and boosted pools. The ecosystem includes Aura Finance as the primary liquid wrapper (analogous to Convex for Curve), which aggregates veBAL voting power and provides boosted yields to depositors. Balancer's integration with protocols like Aave through boosted pools creates unique yield opportunities where pool assets simultaneously earn trading fees and lending interest.

veBAL versus veCRV Design Trade-offs

The fundamental design difference between veBAL and veCRV lies in what gets locked. veCRV locks a single governance token, exposing holders purely to CRV price risk. veBAL locks an 80/20 liquidity position, meaning holders maintain exposure to both BAL and ETH price movements while earning trading fees on the underlying pool. This dual exposure reduces the governance token concentration risk but introduces impermanent loss between BAL and ETH. The shorter maximum lock duration of one year versus four years reflects a philosophical difference — Balancer prioritises accessibility and lower commitment barriers, while Curve prioritises deep long-term alignment. For participants uncertain about multi-year commitments, veBAL provides a lower-risk entry point into ve-tokenomics with meaningful governance participation and yield generation.

Gauge Voting: Directing Protocol Emissions

Gauge voting is the mechanism through which ve-token holders direct governance token emissions towards specific liquidity pools or yield markets. The process operates on a regular cycle — bi-weekly for Curve, weekly for Pendle and Balancer — where holders allocate their voting power across available gauges.

How Gauge Weight Elections Work

Each gauge corresponds to a specific pool or market. During each voting period, ve-token holders distribute their voting power across one or more gauges. The total votes received by each gauge determine its share of the next period's token emissions. A gauge receiving 10% of total votes receives 10% of the emission budget. You can split your votes across multiple gauges or concentrate on a single one, and you can change your allocation each period.

Strategic Voting Considerations

Optimal gauge voting requires balancing multiple factors: the direct benefit of boosted rewards on your own LP positions, the bribe income available for voting on specific gauges, and the broader protocol health implications of your vote. Voting for gauges where you hold LP positions maximises your personal boost, but voting for gauges with the highest bribes may generate more total income. Sophisticated participants model the expected returns from each approach and allocate votes to maximise their combined income from LP rewards, bribes, and protocol fees.

Gauge Killing and Emergency Governance

Protocols maintain the ability to kill gauges — permanently removing them from the emission schedule — through emergency governance actions. Gauge killing typically occurs when a pool's underlying assets lose their peg, suffer an exploit, or when the pool no longer serves the protocol's strategic interests. Killed gauges cannot receive new votes and their existing emission allocation drops to zero in the next epoch. This mechanism protects the protocol from directing emissions towards compromised or abandoned pools. Understanding gauge kill risk matters for bribe farmers because voting for gauges associated with higher-risk assets carries the possibility of sudden bribe income loss if the gauge gets killed mid-epoch.

Vote Delegation and Proxy Voting

Some ve-token systems support vote delegation, allowing holders to assign their voting power to another address without transferring the underlying locked tokens. Delegation is particularly useful for institutional participants who want professional vote managers to optimise their gauge allocations. Snapshot-based governance votes for protocol upgrades commonly support delegation, while on-chain gauge votes have more limited delegation support. Convex's vlCVX system functions as an implicit delegation mechanism — CVX lockers delegate their effective veCRV voting power to Convex's governance process, which then allocates votes based on vlCVX holder preferences expressed through Votium bribes.

- Gauge votes determine the distribution of protocol token emissions across pools

- Weekly gauge weight snapshots determine the following epoch reward allocations

- Strategic gauge voting can significantly increase LP returns on targeted pools

Bribe Markets and Vote Incentive Ecosystems

Bribe markets emerged as a natural consequence of gauge voting systems. Protocols that want to attract liquidity to their pools discovered that paying ve-token holders to vote for their gauges is often more capital-efficient than providing liquidity incentives directly. This created a multi-billion dollar ecosystem of vote incentive platforms.

Votium: The veCRV Bribe Market

Votium is the dominant bribe platform for veCRV gauge votes. Protocols deposit bribe tokens (usually their native governance tokens or stablecoins) into Votium contracts, specifying which gauge they want votes directed towards. veCRV holders (primarily through Convex's vlCVX system) vote for the bribed gauges and claim their proportional share of the bribes after the voting period ends. Votium has processed over $500 million in cumulative bribes since launch, making it one of the most significant DeFi infrastructure platforms by economic throughput.

Hidden Hand and Multi-Protocol Bribes

Hidden Hand by Redacted Cartel operates as a cross-protocol bribe marketplace supporting veCRV, veBAL, vePENDLE, and other ve-token systems. The platform aggregates bribe offers across multiple protocols, allowing ve-token holders to compare bribe rates and allocate votes to the highest-paying opportunities. Hidden Hand's multi-protocol approach provides a unified interface for participants who hold ve-tokens across several systems, simplifying the process of maximising bribe income.

Bribe Economics and Efficiency

The economics of bribing are straightforward: a protocol pays $X in bribes to attract $Y in additional liquidity through boosted gauge emissions. If the value of the attracted liquidity (in terms of trading fees, TVL growth, and token utility) exceeds the bribe cost, the bribe is economically rational. In practice, bribe efficiency varies widely — established protocols with deep liquidity needs consistently offer competitive bribes, while smaller protocols may offer unsustainably high bribes during initial liquidity bootstrapping phases that decline over time.

Bribe Claiming and Gas Optimisation

Claiming bribes requires on-chain transactions that consume gas. On Ethereum mainnet, claiming from Votium typically costs $15-40 per claim depending on network congestion. If you hold bribes across multiple rounds or platforms, batch claiming reduces per-unit gas costs. Some bribe platforms offer auto-claiming services or allow accumulation across multiple rounds before a single claim transaction. For smaller veCRV or vePENDLE positions (under $10,000 in locked value), the gas costs of weekly bribe claiming can meaningfully erode returns — in these cases, liquid wrappers that handle claiming internally offer better net yields.

- Votium and Hidden Hand aggregate bribes from protocols seeking gauge votes

- Bribe yields often exceed direct staking returns for ve-token holders

- Delegating votes to bribe aggregators simplifies the voting process

Liquid Wrappers: Convex, Aura, and Penpie

Liquid wrappers solve the fundamental tension in ve-tokenomics between the benefits of locking and the cost of illiquidity. By aggregating locked positions and issuing tradeable wrapper tokens, these protocols democratise access to ve-token benefits while providing exit liquidity.

Convex Finance and cvxCRV

Convex Finance is the largest veCRV aggregator, holding over 50% of all veCRV supply. When you deposit CRV into Convex, it is permanently locked as veCRV, and you receive cvxCRV — a liquid ERC-20 token that trades on secondary markets. cvxCRV holders earn a share of Convex's veCRV rewards, platform fees, and additional CVX incentives. The vlCVX system allows CVX token holders to lock CVX for 16 weeks to direct Convex's massive veCRV voting power, creating a meta-governance layer where vlCVX votes effectively control Curve's gauge emissions.

Aura Finance and auraBAL

Aura Finance performs the same function for Balancer that Convex performs for Curve. Aura aggregates veBAL voting power and provides boosted BAL rewards to depositors. auraBAL is the liquid wrapper for locked veBAL positions, and vlAURA allows AURA token holders to direct Aura's veBAL votes. The Aura ecosystem is smaller than Convex but growing steadily as Balancer's TVL expands through boosted pool integrations with lending protocols.

Penpie and mPENDLE

Penpie is the emerging liquid wrapper for vePENDLE, aggregating PENDLE locks and providing boosted yields to depositors. mPENDLE represents locked PENDLE positions and trades on secondary markets. The Penpie ecosystem is newer than Convex or Aura, reflecting Pendle's more recent adoption of ve-tokenomics, but it is growing rapidly as Pendle's TVL and bribe market activity increase through 2026.

Comparing Liquid Wrapper Economics

Each liquid wrapper charges fees that reduce your net yield compared to direct locking. Convex takes a 16% performance fee on CRV rewards earned through its platform, plus a 1% withdrawal fee on cvxCRV unstaking. Aura Finance charges a similar performance fee structure on BAL rewards. Penpie's fee structure is competitive at 12-15% of PENDLE rewards. When evaluating whether to use a liquid wrapper versus direct locking, calculate the break-even point: the fee cost must be offset by the higher boost achieved through the aggregator's pooled voting power and the liquidity premium of holding a tradeable wrapper token.

For positions under $50,000 in locked value, liquid wrappers almost always provide superior net returns because individual holders cannot achieve meaningful boost levels without substantial ve-token holdings. For positions exceeding $200,000, direct locking becomes increasingly competitive because the holder's own ve-balance provides sufficient boost, and avoiding wrapper fees compounds meaningfully over multi-year lock durations.

Liquid Wrapper Depeg and Redemption Risk

Liquid wrapper tokens like cvxCRV, auraBAL, and mPENDLE trade on secondary markets where their price can deviate from the underlying token value. During market stress events, wrapper tokens often trade at discounts of 5-15% as holders rush to exit positions. The cvxCRV peg has historically fluctuated between 0.85 and 1.02 relative to CRV, with deeper discounts during broad market selloffs. These depegs create both risk and opportunity — buying wrapper tokens at significant discounts provides enhanced yield if the peg recovers, but selling during a depeg crystallises losses. Understanding the redemption mechanics of each wrapper helps assess depeg risk: cvxCRV cannot be redeemed for CRV (the lock is permanent), meaning the peg relies entirely on secondary market liquidity and arbitrage incentives rather than a hard redemption floor.

ve-Token Strategies

Effective ve-token participation requires choosing between direct locking and liquid wrapper approaches, then optimising your voting strategy to maximise combined returns from protocol fees, boosted rewards, and bribe income.

Direct Locking versus Liquid Wrappers

Direct locking gives you full control over your votes and maximum flexibility in gauge allocation, but locks your capital for the full duration with no exit option. Liquid wrappers sacrifice some voting control (your votes are directed by the wrapper protocol's governance) but provide immediate exit liquidity through secondary market trading. For most participants, liquid wrappers offer a better risk-adjusted proposition because the liquidity premium outweighs the governance control premium. Direct locking is primarily advantageous for large holders who want to direct votes towards their own LP positions or who participate actively in protocol governance beyond gauge voting.

Bribe Income Optimisation

Maximising bribe income requires monitoring bribe rates across platforms and allocating votes to the highest-paying gauges each period. The optimal strategy changes weekly as bribe offers fluctuate based on protocol needs and market conditions. Tools like Llama Airforce for veCRV and Pendle's built-in bribe dashboard help you compare rates and estimate returns before committing your votes. You should factor in gas costs for claiming bribes — on Ethereum mainnet, claiming from multiple bribe sources can cost $20-50 in gas, which may erode returns on smaller positions.

Portfolio Allocation Across ve-Token Systems

Diversifying across multiple ve-token systems reduces protocol-specific risk while maintaining exposure to the broader ve-tokenomics yield opportunity. A balanced allocation might dedicate 40-50% to veCRV (through Convex) for its mature bribe ecosystem and stable fee income, 30-35% to vePENDLE for its higher growth potential and yield market exposure, and 15-25% to veBAL (through Aura) for its shorter lock duration and Aave-boosted pool integration. Rebalancing between systems should occur quarterly based on relative bribe yields, protocol TVL trends, and governance token price performance. Avoid concentrating more than 60% of your ve-token portfolio in any single system regardless of current yield attractiveness.

Risks and Limitations of ve-Tokenomics

Despite the proven effectiveness of ve-tokenomics, the model carries specific risks that you must understand before committing capital to locked positions.

Illiquidity and Opportunity Cost

The most significant risk is illiquidity. Locked tokens cannot be withdrawn before expiry regardless of market conditions. If the governance token price drops 80% during your lock period, you cannot sell to limit losses. The opportunity cost of locking also compounds over time — capital locked in veCRV cannot be deployed to new opportunities that may offer superior risk-adjusted returns. You should only lock tokens that you are comfortable holding for the full duration under adverse market conditions.

Governance Centralisation Concerns

Liquid wrappers like Convex have concentrated enormous voting power in the hands of relatively few protocols. Convex controls over 50% of veCRV, meaning that vlCVX governance effectively controls Curve's emission schedule. While this concentration has not led to malicious governance actions to date, it creates systemic risk — a compromise of Convex's governance could redirect Curve's emissions in harmful ways. Diversifying your ve-token exposure across multiple protocols and wrapper systems helps mitigate this concentration risk.

Governance Token Price Exposure

ve-token returns are denominated in the governance token and protocol fees. If CRV price declines 50% during your lock period, your veCRV position loses 50% of its USD value even if the CRV-denominated returns are attractive. Bribe income partially hedges this risk when bribes are paid in stablecoins or other tokens, but protocol fee distributions and boosted rewards are typically in the native governance token. You should evaluate ve-token positions based on your conviction in the underlying protocol's long-term value, not just the current APR figures.

Smart Contract and Protocol Risk

Locking tokens in ve-contracts introduces smart contract risk that persists for the entire lock duration. While Curve's veCRV contract has operated without exploit for over five years, newer ve-implementations carry higher uncertainty. Liquid wrappers add additional smart contract layers — using cvxCRV means trusting both Curve's veCRV contract and Convex's wrapper contracts simultaneously. The compounding of smart contract risk across multiple protocol layers is a frequently underestimated danger. Before locking significant capital, verify that the ve-contract has been audited by reputable firms, has operated without incident for at least six months, and holds a bug bounty programme proportional to its TVL.

Regulatory and Compliance Considerations

The regulatory landscape for ve-token systems remains uncertain across major jurisdictions. Governance tokens that provide revenue sharing through fee distributions may be classified as securities under certain regulatory frameworks, particularly in the United States where the Howey test evaluates whether an asset constitutes an investment contract. The bribe market ecosystem adds further regulatory complexity — payments for governance votes could attract scrutiny from financial regulators concerned about market manipulation or undisclosed conflicts of interest. European participants should monitor the Markets in Crypto-Assets Regulation framework, which introduces licensing requirements for crypto-asset service providers that may affect how ve-token platforms operate within the European Union. Prudent participants maintain awareness of their local regulatory environment and consider the jurisdictional risk of the protocols they interact with.

The Future of ve-Tokenomics

The ve-token model continues to evolve as protocols experiment with modifications to the original Curve design. Several emerging trends are reshaping how vote-escrow systems function and how participants interact with them.

ve-NFT Implementations and Transferable Locks

Protocols like Velodrome and Aerodrome on Optimism and Base introduced ve-NFT models where locked positions are represented as non-fungible tokens rather than non-transferable balances. These veNFTs can be traded on secondary markets, providing native liquidity without requiring separate liquid wrapper protocols. The veNFT approach preserves the commitment mechanism — the lock duration and voting power remain attached to the NFT — while enabling position transfers between wallets. This innovation addresses the illiquidity problem at the protocol level rather than relying on third-party wrappers, potentially reducing the smart contract layering risk that characterises the Convex and Aura ecosystems.

Governance Minimisation and Automated Voting

As ve-token ecosystems mature, governance participation increasingly shifts from manual voting to automated strategies. Protocols are developing on-chain voting agents that automatically allocate gauge votes based on predefined optimisation criteria — maximising bribe income, supporting ecosystem-aligned pools, or maintaining balanced emission distributions. This automation trend reduces the governance burden on individual holders while potentially improving capital efficiency across the ecosystem. However, automated voting also raises concerns about governance centralisation if a small number of voting agents control the majority of gauge allocations.

Conclusion

ve-Tokenomics has proven itself as the most effective governance model in DeFi, aligning long-term incentives between protocol participants through irreversible token locking. The three major implementations — veCRV, vePENDLE, and veBAL — each adapt the core model to their protocol's specific needs while maintaining the fundamental principles of commitment-based governance and reward distribution. The success of these systems is evidenced by their longevity and the billions of dollars voluntarily locked by participants who recognise the value of governance participation and boosted yield access.

The bribe market ecosystem that has emerged around ve-token governance represents one of the most innovative developments in DeFi economics. Platforms like Votium, Hidden Hand, and Paladin have created transparent marketplaces where protocols compete for liquidity by offering incentives to ve-token holders who direct emissions towards their pools. This market-driven approach to liquidity allocation has proven more efficient than traditional liquidity mining programmes, as it channels incentives precisely where demand exists rather than distributing them uniformly across all pools.

For yield optimisers in 2026, ve-token participation offers a compelling combination of protocol revenue sharing, boosted LP rewards, and bribe market income. The choice between direct locking and liquid wrappers depends on your capital size, governance involvement preferences, and liquidity needs. Start with liquid wrappers like Convex or Aura to gain exposure with exit flexibility, then consider direct locking as your understanding deepens and your conviction in specific protocols strengthens. The key insight is that ve-token participation rewards patience and commitment — the longer your lock duration, the greater your voting power, boost multiplier, and overall share of total accumulated protocol revenue. Diversify across multiple ve-token ecosystems to reduce protocol-specific concentration risk while maintaining broad exposure to this proven governance and yield generation framework. For the complete yield optimisation framework, return to our yield optimisation strategies hub.

Sources and References

Frequently Asked Questions

- What happens to my voting power as the lock period expires?

- Voting power decays linearly from the moment you lock until the lock expiry date. If you lock 1,000 CRV for four years, you receive the maximum veCRV balance immediately, but that balance decreases by approximately 25% each year. After two years, you hold roughly half your original voting power. At expiry, your voting power reaches zero and you can withdraw your unlocked tokens. You can counteract this decay by extending your lock duration at any time, which resets the decay curve and restores your voting power to the level corresponding to the new lock end date.

- Can I unlock my tokens before the lock period ends?

- No, vote-escrow locks are irreversible by design. Once you lock CRV, PENDLE, or BAL tokens, they cannot be withdrawn until the lock period expires. This irreversibility is a core feature that ensures long-term commitment and prevents short-term manipulation of governance votes. However, liquid wrappers like cvxCRV from Convex Finance and sdCRV from Stake DAO provide tradeable representations of locked positions, allowing you to exit your economic exposure through secondary markets at a potential discount to the underlying value.

- How do bribe markets work and are they safe?

- Bribe markets are platforms where protocols pay ve-token holders to vote for their liquidity pools in gauge weight elections. Platforms like Votium for veCRV and Hidden Hand for multiple ve-tokens aggregate bribe offers and distribute payments to voters who direct their gauge votes accordingly. Established bribe markets like Votium have processed billions in cumulative bribes without major incidents. You should verify that bribe tokens are from legitimate protocols and claim bribes promptly to minimise smart contract exposure.

- What is the difference between veCRV and cvxCRV?

- veCRV is the native vote-escrow token obtained by locking CRV directly with Curve Finance, granting voting power, boosted rewards, and protocol fee sharing. cvxCRV is a liquid wrapper created by Convex Finance that represents permanently locked CRV. When you convert CRV to cvxCRV through Convex, the CRV is locked as veCRV forever, and you receive a tradeable cvxCRV token that earns a share of Convex platform fees, veCRV rewards, and CVX incentives. The key difference is liquidity: veCRV is locked until expiry, while cvxCRV can be traded on secondary markets at any time, though often at a slight discount to the underlying CRV value.

- Which ve-token system offers the best returns in 2026?

- Returns vary significantly based on market conditions, bribe volumes, and your participation strategy. veCRV offers the most mature ecosystem with the deepest bribe markets through Votium, typically yielding 15-30% APR from combined protocol fees, bribes, and CRV emissions. vePENDLE benefits from Pendle's rapid growth and can yield 20-40% APR through protocol revenue sharing and bribe income, though with higher volatility. veBAL provides moderate returns of 10-20% APR with strong Balancer ecosystem integration. You should evaluate returns net of the opportunity cost of locking your tokens and the governance token's price risk over the lock duration.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.