Bitcoin ETF vs Direct Ownership 2026 Framework

When to choose an ETF wrapper, when to hold Bitcoin directly, and how the answer depends more on your account structure than on ideology. Covering tax wrappers, custody control, fees and tracking quality across US, EU and UK markets.

Introduction

Until January 2024, owning Bitcoin meant either holding the asset directly through a crypto exchange or self-custody wallet, or accepting indirect proxy exposure through Bitcoin-mining stocks and futures-based products.

The launch of US spot Bitcoin ETFs changed the structure. BlackRock's IBIT, Fidelity's FBTC, ARK 21Shares' ARKB and similar products from other major issuers now offer Bitcoin price exposure inside ordinary brokerage accounts, retirement wrappers and tax-advantaged structures. Both routes give you Bitcoin exposure. The trade-offs differ on tax wrapper, custody control, fees, accessibility and tracking quality.

The framing of this decision often produces unnecessary heat. ETF investors are accused of compromising on Bitcoin's self-custody ethos. Direct holders are accused of taking on operational risk that ETF investors avoid. Both characterisations miss the point. The right path depends on which account structures the investor has access to, what holding size they are working with, and what tax wrappers their jurisdiction makes available. Most experienced Bitcoin investors hold both — ETFs in tax-advantaged retirement accounts, direct Bitcoin in taxable accounts where the no-expense-ratio advantage compounds over decades.

This decision is not ideological. The right answer for most investors is account-structure-driven:

- ETFs in retirement and tax-advantaged accounts where direct Bitcoin is impractical or impossible

- Direct ownership for strategic conviction holdings where the lack of expense ratio compounds materially over multi-decade horizons

- Hybrid allocations for investors with capacity in both account types — typically 50/50 or weighted to whichever side has the most tax-advantaged headroom

The framework below walks through the comparison axis by axis, covers the regional wrapper differences across US, EU and UK markets, and ends with a decision matrix that maps account structures to the appropriate path. We give specific answers for representative investor profiles rather than generic principles, because account-structure decisions are typically more concrete than allocation philosophy.

One framing point before we start. The expense ratio difference between ETFs (0.20-0.25%) and direct Bitcoin (0.0% ongoing) is small in any single year. Over twenty years on a position that compounds materially, the difference reaches tens of thousands of dollars. The custody risk differential between regulated ETF custody and properly-executed self-custody is also small in expectation but high in tail-risk scenarios. Neither factor dominates in isolation. Together, the two factors are usually enough to make direct ownership preferable for the largest strategic holdings while ETFs remain preferable for retirement-account exposure regardless of position size.

If you arrived from our Bitcoin investment fundamentals hub, this satellite goes deeper on the ETF-versus-direct trade-offs that the hub covered at framework level.

The Spot Bitcoin ETF Landscape in 2026

The US spot Bitcoin ETF approval in January 2024 unlocked a structure that earlier rejected applications had been seeking for nearly a decade. Eleven products launched simultaneously on day one, with several more following over the next two years.

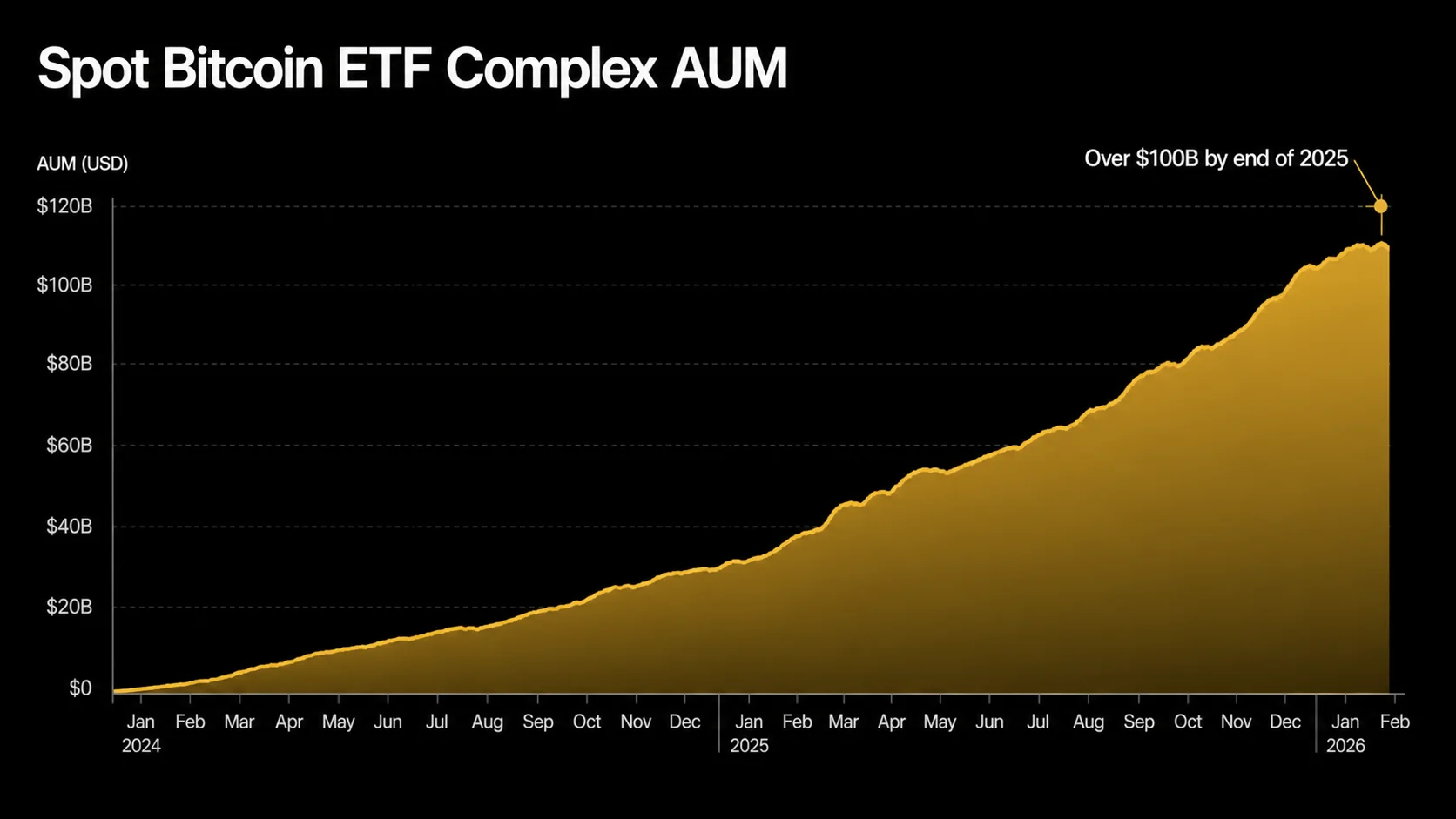

By the end of 2025, the collective US spot Bitcoin ETF complex had reached roughly $100 billion in assets under management — about $102 billion, or 6.5% of Bitcoin's market cap, by mid-2026 — a scale that significantly exceeded analyst expectations from before the approval and that materially affected Bitcoin's market structure.

The major US issuers

Three issuers dominate the US spot Bitcoin ETF market by AUM:

- BlackRock's iShares Bitcoin Trust (IBIT) — largest by a meaningful margin, holding on the order of 700,000+ BTC with net assets of roughly $48-50 billion as of mid-2026 (down from its 2025 peak as Bitcoin trades well below its October 2025 all-time high)

- Fidelity's Wise Origin Bitcoin Fund (FBTC) — second-largest with materially smaller but still substantial holdings

- ARK 21Shares Bitcoin ETF (ARKB), Bitwise BITB and Grayscale's converted GBTC — competing for third position with comparable but smaller AUM levels

The remaining issuers — Franklin Templeton, Invesco, VanEck, WisdomTree and Valkyrie — hold smaller positions but provide competitive options for investors prioritising specific issuer relationships or expense-ratio considerations.

Expense ratios and fee structures

Expense ratios across the major US spot Bitcoin ETFs cluster between 0.20% and 0.25% per year, with several issuers having waived fees temporarily during the launch period to compete for AUM.

By comparison, Grayscale's GBTC carried a 1.5% expense ratio at the time it converted from a closed-end trust to an ETF, which made it materially more expensive than its competitors and contributed to outflows from GBTC into lower-cost alternatives during the 2024-2025 period. Outside the US, European and UK Bitcoin ETPs have wider expense-ratio ranges, with several products in the 0.5-1.0% range and some closer to US levels.

European and UK products

European spot Bitcoin ETPs predate the US ETFs by several years and trade on exchanges in Switzerland, Germany, Sweden and other jurisdictions. 21Shares Bitcoin ETP, CoinShares Physical Bitcoin and several others have multi-year track records and remain available to UK and EU investors through brokers offering European exchange access.

UK-listed Bitcoin ETPs received FCA approval for retail access during 2024-2025, with brokers including Hargreaves Lansdown, IG and Trading 212 offering ISA-eligible products that did not exist for UK retail investors a year earlier.

Cumulative inflows and growth pattern

US spot Bitcoin ETFs accumulated roughly $54 billion in cumulative net inflows by mid-2026 (down from a ~$58 billion peak in April 2026 after flows turned net-negative through the spring), with daily flows that regularly exceeded $500 million during periods of strong sentiment.

The growth pattern affected Bitcoin's market structure. ETF flows on a typical trading day moved more capital than miners produce in a week, which mechanically shifted the supply-demand balance towards demand-driven price discovery. The cycle implications are covered in the cycle satellite in this cluster.

Direct Bitcoin Ownership

Direct Bitcoin ownership means holding the asset itself rather than a financial product that holds it on your behalf. The path runs from a regulated exchange purchase to either:

- Continued exchange custody (acceptable for small positions)

- Software wallet self-custody (transitional)

- Hardware wallet self-custody (the standard for serious holdings)

Direct ownership has fundamentally different properties from ETF wrappers, and the differences matter for specific use cases.

What direct ownership preserves

Direct Bitcoin holders control their own keys. There is no annual expense ratio. There is no issuer who can suspend redemptions during market stress, no custodian who can be compelled by government order to freeze funds, no fund-level liquidity gates during volatility shocks.

The Bitcoin can be moved across borders, sent outside business hours, used to settle transactions with counterparties anywhere in the world, and held indefinitely without any third-party dependency. These properties are the original use case Bitcoin was designed for, and ETF holders give them up entirely in exchange for the wrapper convenience.

The cost of direct ownership

Direct ownership has its own costs.

Initial setup is more involved than buying an ETF. The full sequence covers account creation on a regulated exchange, KYC verification, fiat deposit, the first Bitcoin purchase, hardware wallet acquisition, seed-phrase backup, transfer to self-custody, and recovery testing. The full setup takes several hours and requires careful attention to security details that ETF investors do not need to think about.

Recurring operations — sending Bitcoin, receiving Bitcoin, signing transactions on the hardware wallet — require ongoing operational discipline. Mistakes can be irrecoverable. A Bitcoin sent to the wrong address is gone forever, with no customer-service path for recovery.

Why direct ownership compounds favourably over long horizons

Over multi-decade horizons, the absence of an annual expense ratio compounds materially.

A $100,000 Bitcoin position in an ETF charging 0.25% annually pays $250 in the first year, but that figure scales with the position value. A position that grows to $500,000 over a decade pays $1,250 per year by year ten. The cumulative cost over the full decade can reach $10,000-$15,000 depending on the growth pattern.

Direct holdings pay none of that. The compound difference grows with both time and position size, which is why strategic conviction holdings often migrate to direct ownership even when initial smaller positions started as ETFs.

The practical setup for direct ownership

Direct ownership setup follows a standard pattern:

- Choose a regulated exchange — OKX outside the US, Coinbase or Kraken for US investors, with Bybit as a secondary option for advanced users

- Complete KYC verification — government-issued ID and proof of address depending on tier

- Deposit fiat — bank transfer for lowest fees, debit card for instant deployment

- Place a market or limit order for Bitcoin

- Set up a hardware wallet for positions exceeding approximately $1,000 (Ledger or Tangem are the standard recommendations for first-time setup)

- Generate a seed phrase and store it on metal backup hardware

- Transfer the Bitcoin to the hardware wallet address

- Run a recovery test before relying on the system

The full sequence takes 2-4 hours the first time and produces a permanent storage system.

Tax Wrapper Comparison by Region

Tax wrappers can produce return differences larger than the ETF-versus-direct trade-off itself over long horizons. The wrapper choice often dictates which path is appropriate before any other consideration enters the decision. The framework varies materially by jurisdiction and is the area where qualified professional advice produces the highest return on consultation cost for non-trivial positions.

United States

US investors have three primary tax structures available.

Standard taxable brokerage accounts treat both spot Bitcoin ETFs and direct Bitcoin as property for capital-gains purposes. Short-term gains (held under one year) are taxed at ordinary income rates of 10-37% federal. Long-term gains are taxed at 0%, 15% or 20% federal depending on income band, plus state tax in most states.

Standard brokerage IRAs (Traditional and Roth) can hold spot Bitcoin ETFs within the IRA wrapper. Traditional IRAs defer tax until distribution. Roth IRAs eliminate tax on qualified distributions. This is the simplest path for tax-advantaged Bitcoin exposure.

Self-directed IRAs through specialised cryptocurrency custodians (BitcoinIRA, iTrustCapital, Unchained) can hold direct Bitcoin tax-deferred. The $200-500 annual custodian fees often offset the wrapper benefit for positions under approximately $50,000.

The wash-sale rule that applies to securities does not currently apply to Bitcoin in the US, which allows tax-loss harvesting strategies on direct Bitcoin holdings that are not available with traditional securities or with Bitcoin ETFs (which are treated as securities for wash-sale purposes). This is a meaningful tax-management advantage for direct Bitcoin holdings in taxable accounts.

European Union

EU treatment varies substantially by member state under the broader MiCA framework that came into effect during 2024-2025:

- Germany — Bitcoin held more than 12 months is tax-free on disposal, which favours direct holdings over ETF wrappers (ETF disposals can trigger different tax treatment under securities rules even after the same 12-month period)

- France — flat 30% rate (single tax on capital income, "PFU") on most crypto disposals regardless of wrapper, making the wrapper choice relatively neutral in pure tax terms

- Portugal — 28% rate on disposals within one year of acquisition, 0% beyond (similar to Germany)

- Netherlands — Bitcoin taxed under wealth-tax rules ("box 3") rather than capital-gains rules, with annual taxation on assumed returns regardless of actual gains

Spain, Italy, Belgium, Sweden and other major EU jurisdictions each have distinct rules. Verify with a local accountant for any meaningful position.

United Kingdom

UK investors have the cleanest wrapper-driven decision amongst major jurisdictions.

HMRC treats Bitcoin disposals (including ETF disposals) as capital gains. The annual capital-gains tax allowance for the 2026/27 tax year is currently set at £3,000. Gains above the allowance are taxed at 18% (basic rate) or 24% (higher and additional rates), following the rate increase that took effect in October 2024.

Spot Bitcoin ETPs approved for the UK retail market are eligible for ISA wrappers through brokers including Hargreaves Lansdown, IG, Trading 212 and AJ Bell. Holdings inside an ISA shelter gains from CGT entirely up to the annual ISA allowance of £20,000, which can produce a meaningful long-term tax efficiency advantage over direct Bitcoin holdings outside any wrapper.

SIPPs (self-invested personal pensions) can also hold Bitcoin ETPs in many cases, providing further tax-advantaged Bitcoin exposure. Direct Bitcoin holdings remain subject to CGT on disposal and to detailed transaction reporting requirements that have grown stricter over recent years.

Practical implications by wrapper

The tax wrapper choice often outweighs the ETF-versus-direct choice in long-term return terms.

For US investors with tax-advantaged retirement capacity, ETFs in the IRA are usually the highest-after-tax-return path because the wrapper compounds gains tax-free or tax-deferred regardless of expense ratio.

For UK investors with ISA capacity, ISA-eligible Bitcoin ETPs can produce 20-30 percentage points of long-term return advantage over taxable direct holdings depending on tax band and holding period. The ISA wrapper benefit dwarfs the expense ratio cost over multi-decade horizons — a £20,000 annual ISA contribution to Bitcoin ETPs over five years builds £100,000 of permanently CGT-protected exposure that no direct-holding structure can match in equivalent tax efficiency.

EU investors face the most country-specific decisions:

- In Germany, the one-year holding rule favours direct holdings

- In France, the flat rate applies broadly so wrapper neutrality lets investors choose on operational grounds

- In the Netherlands, wealth-tax treatment changes the calculation entirely

For positions large enough to matter, the few hundred currency units spent on a qualified tax accountant before structuring the position pays back many times over.

Custody and Counterparty Risk Comparison

Custody risk profiles differ qualitatively between ETFs and direct ownership. Both approaches are safe enough for serious holdings if executed properly. The risks differ in nature rather than magnitude, and the right answer depends on which risk type fits your operational comfort.

ETF custody risk

Spot Bitcoin ETFs hold the underlying Bitcoin with institutional custodians. Coinbase Custody is the largest by AUM, with several smaller custodians serving specific issuers. The custodian holds Bitcoin in regulated cold storage with commercial crime-insurance cover on a portion of the assets, regular audit, and standard institutional risk controls.

The ETF itself adds a second layer. The issuer (BlackRock, Fidelity, ARK, etc.) operates the fund, manages share creation and redemption, handles regulatory reporting, and makes the Bitcoin available to shareholders through the ETF wrapper.

The risks at this layer are very low for major issuers but not zero:

- A custodian failure could affect multiple ETFs simultaneously, given the concentration with Coinbase Custody

- An issuer bankruptcy could create complications for share redemption even if the underlying Bitcoin is segregated and protected

- Regulatory action against the ETF structure or specific issuers could affect access

The 2022-2023 Coinbase legal disputes with the SEC, while resolved in Coinbase's favour, illustrated that even major custodians face structural risks. Most of these scenarios are tail risks that have not materialised, and the ETF structure has held up well through its first two years of operation.

Direct ownership operational risk

Direct ownership shifts the risk surface from counterparty to operational. Self-custody removes counterparty risk entirely — no exchange or custodian can fail, freeze, or restrict access to the Bitcoin.

The risks become operational:

- Lost or destroyed seed phrases

- Hardware wallet failure or supply-chain compromise

- Malware or phishing during transaction signing

- Irrecoverable transmission errors when sending Bitcoin to wrong addresses

- The small but real risk of physical theft or coercion targeting the holder

Operational risks are largely controllable through standard practice. Metal seed-phrase backups eliminate paper degradation and most fire/water risks. Multi-location backup distribution eliminates single-point-of-failure risks. Recovery testing before the first significant balance eliminates the most common backup-failure mode. Hardware wallets from established manufacturers eliminate most supply-chain risk. Transaction-signing discipline (verifying addresses on the hardware wallet display, not just the computer screen) eliminates most malware risks. The full operational discipline takes deliberate setup but is achievable for any motivated investor.

Where each approach fails

The historical pattern of large retail Bitcoin losses informs the comparison. Most major retail losses have come from custodial exchange failures (Mt Gox, QuadrigaCX, FTX, Celsius, BlockFi, Voyager) — a category that does not include either spot Bitcoin ETFs from major issuers or properly-executed self-custody.

The specific failure modes of major-issuer ETFs have been very rare and limited in scope. The specific failure modes of self-custody have been operational errors by individual holders, which scale with the number of holders rather than with position size and rarely make headlines.

The risk comparison is not "which is safer in absolute terms" but "which risk profile matches your operational comfort". Investors who would lose sleep over operational responsibility for self-custody often sleep better with major-issuer ETFs. Investors who would lose sleep over counterparty dependence often sleep better with direct ownership. Both are defensible.

Tracking Error and Premium-Discount Dynamics

Spot Bitcoin ETFs track the underlying Bitcoin price closely but not perfectly. The deviations matter for short-term traders and have minor implications for long-term investors. Understanding the tracking dynamics helps set expectations and reveals when tracking issues become large enough to affect the wrapper choice.

How tracking error arises

Tracking error in spot Bitcoin ETFs comes from three primary sources:

- Expense ratio drag — mechanically deducts a small amount each trading day, producing a small but predictable underperformance against perfect Bitcoin holding

- NAV calculation timing — the ETF's net asset value is calculated against a reference Bitcoin price (typically the CF Benchmarks Bitcoin Reference Rate or similar), which may differ slightly from spot prices on individual exchanges at any given moment

- Trading-hours pricing — the ETF share price during trading hours is set by market supply and demand, which can produce small premiums or discounts to NAV depending on creation/redemption flows

Premium and discount patterns

During normal market conditions, US spot Bitcoin ETFs trade within a few basis points of NAV — typically 0.05% to 0.15% in either direction during liquid trading hours.

During periods of stress (large flow days, after-hours moves in Bitcoin spot, or volatility shocks), premiums or discounts can widen to 0.5% or occasionally larger. The market-maker arbitrage mechanism that creates and redeems ETF shares to track NAV operates effectively during normal conditions, which keeps tracking tight. During stress, the arbitrage mechanism can be temporarily impaired, which is when wider deviations occur.

Impact on long-term investors

For investors holding Bitcoin ETFs for multi-year horizons, tracking error and premium-discount dynamics are essentially noise.

The expense ratio is the only systematic drag. Even at 0.25% annually the cumulative impact over a decade is in the 2-3% range — meaningful but not large enough to change the wrapper decision. For short-term traders or active rebalancers, the dynamics matter more. Trading during low-liquidity windows, on illiquid issuers, or during stress periods can result in execution prices materially different from the underlying Bitcoin spot price.

European and UK ETP dynamics

European and UK Bitcoin ETPs typically trade with somewhat wider tracking ranges than US spot ETFs because of lower liquidity, smaller market-maker presence and different trading hours that limit arbitrage windows.

Spreads of 0.2% to 0.5% are not uncommon during normal hours, and wider deviations can occur during US-hours volatility that does not directly affect European market makers. The trade-off for UK ISA-eligibility or specific European wrapper benefits often outweighs the tighter tracking of US products for investors with regional account structures.

Detailed Cost Comparison Across Holding Periods

The expense ratio versus self-custody trade-off looks small in any single year and substantial across multi-decade horizons. Quantifying the difference helps you make the wrapper decision with concrete numbers rather than abstract intuitions.

Year-by-year drag on a $50,000 position

Take a $50,000 Bitcoin position held for 20 years. Assume Bitcoin produces 12% annualised returns over that period — modest by historical Bitcoin standards but reasonable for a maturing asset. The ETF version runs the position through a 0.25% annual expense ratio. The direct version has a one-time hardware wallet cost (assume $200) and zero ongoing fees.

After year 1, the ETF position is worth approximately $55,860 versus $56,000 for direct ownership — a $140 difference, essentially noise. After year 5, the gap is approximately $1,200. After year 10, it widens to $5,500. After 20 years, the cumulative drag exceeds $35,000 — meaningful money even on a position that has compounded substantially.

Two takeaways. First, the wrapper decision genuinely matters for long-horizon strategic conviction holdings, not for short-horizon tactical exposure. Second, the math is non-linear: most of the cost differential accumulates in the late years of the holding period when the position has grown large enough that 0.25% applied annually represents real money.

The wrapper-benefit override

Why do most experienced investors still hold significant ETF exposure despite the long-term cost drag? Because tax-wrapper benefits typically override expense-ratio considerations by an order of magnitude.

Consider the same $50,000 position held 20 years inside a Roth IRA (US) versus a taxable account holding direct Bitcoin. The Roth IRA version produces zero tax on disposal — all $483,000 of compound gains (assuming 12% annualised) accrue to you. The taxable direct Bitcoin version produces approximately $96,000 of long-term capital gains tax at 20% on the same gains. The $35,000 expense ratio drag inside the Roth wrapper is dwarfed by the $96,000 tax savings the wrapper delivers. The same logic applies to UK ISA-wrapped Bitcoin ETPs versus taxable direct Bitcoin.

This is the practical reason most serious investors hold both wrappers. The ETF allocation captures wrapper benefits where they exist; the direct allocation captures cost efficiency where wrapper capacity is exhausted. The combined structure produces better after-tax outcomes than either approach alone.

Jurisdiction-specific worked examples

Three concrete examples illustrate the wrapper-driven decision logic for typical retail scenarios:

UK investor with £100,000 Bitcoin allocation target. The optimal structure typically uses ISA wrapper capacity first — £20,000 per year of ISA-eligible Bitcoin ETPs builds towards the target while sheltering gains from UK CGT. The remaining £80,000 sits in direct Bitcoin in a taxable account, where the no-expense-ratio advantage compounds over multi-decade horizons. By year 5, the structure has built £100,000 of ISA-protected ETP exposure that remains permanently CGT-free. The ETP expense ratio of 0.25% over 20 years on the £100,000 ISA portion costs approximately £8,000 — but the alternative (taxable direct Bitcoin) would cost approximately £30,000-40,000 in CGT on the same gains depending on tax band. The wrapper benefit is decisive.

US investor with $200,000 Bitcoin allocation target and Roth IRA capacity. Direct Bitcoin in retirement accounts requires specialised self-directed IRA structures that introduce annual custody fees (often $300-500/year) and operational complexity. For most US investors, ETF exposure inside the Roth IRA up to annual contribution limits, with direct Bitcoin in taxable accounts for the remainder, produces optimal after-tax outcomes. The Roth-wrapped portion compounds tax-free regardless of expense ratio; the taxable direct portion captures cost efficiency without sacrificing self-sovereignty.

EU investor in Germany with €75,000 Bitcoin allocation target. Germany's 12-month tax-free rule on Bitcoin holdings flips the typical calculation. Direct Bitcoin held over 12 months produces tax-free disposal — a benefit that ETF wrappers cannot replicate (ETFs are taxed as securities, not as Bitcoin). For German investors, the ETF wrapper provides regulatory familiarity but loses the most valuable tax benefit available in the jurisdiction. Direct Bitcoin with hardware wallet custody is typically the optimal approach for German investors with strategic conviction allocations.

How wrapper choice changes through life stages

The ETF-vs-direct decision is not static across an investor's life. Three life stages typically produce different optimal wrapper choices.

In early career (typically ages 25-40), most retail investors have unused tax-advantaged retirement capacity. Maximising contributions to that capacity through ETF exposure produces the highest after-tax compound growth, because decades of tax-deferred or tax-free growth dwarf the expense ratio drag. Direct Bitcoin in this stage typically serves as a smaller satellite holding rather than the primary allocation.

In mid-career (typically ages 40-55), retirement wrapper capacity has often been consumed and significant taxable wealth has accumulated. The wrapper choice shifts: continue maxing out retirement contributions for the remaining capacity, but increasingly direct new Bitcoin allocations into direct ownership in taxable accounts where the no-expense-ratio compounding starts to matter materially over 20+ year horizons.

Approaching retirement (typically ages 55-65), the wrapper choice shifts again. Sequence-of-returns risk becomes the dominant consideration. Concentrated Bitcoin holdings — whether ETF or direct — in this stage need careful sizing relative to total portfolio, with rebalancing protocols that protect against being forced to sell during drawdowns to fund retirement income. Many investors at this stage trim Bitcoin allocations to lower tiers (5% or below) regardless of wrapper, treating the position as completed accumulation rather than ongoing accumulation.

The hidden cost of switching wrappers mid-position

Once you have built a Bitcoin position in one wrapper, switching to another wrapper later typically involves taxable disposal of the original position. For a $100,000 position with substantial unrealised gains, the tax on disposal can easily exceed $20,000, which then becomes the cost of the wrapper switch.

This is why the wrapper decision deserves careful thinking at the outset rather than being treated as something you can adjust later. The reality is that "later adjustment" carries a real tax cost that often outweighs the perceived inefficiency of the original wrapper choice. Most investors who consider switching wrappers mid-position end up keeping the existing structure once they account for the disposal tax. Plan the wrapper structure as if it is permanent, because functionally it usually is.

Execution venue tradeoffs across wrapper options

Beyond wrapper structure, execution venue meaningfully affects realised investment outcomes through fees, spreads, slippage, withdrawal restrictions, regional regulatory frameworks, custodian arrangements, taxable-event timing, reporting integration, customer support quality, and platform stability through volatile market periods. Investors holding direct Bitcoin through major regulated exchanges typically experience smaller execution friction than investors transacting through smaller regional platforms, although larger platforms sometimes impose stricter withdrawal limits during periods of elevated network congestion.

Investors holding ETF wrappers through traditional brokerage accounts experience execution dynamics inherited from underlying equity markets — narrow bid-ask spreads during regular trading hours, wider spreads outside regular hours, tracking error during volatile periods. Comparing wrapper choices therefore requires comparing wrapper-specific execution profiles rather than treating execution friction as identical across structures. Investors transitioning between wrappers should carefully evaluate execution friction differential alongside taxable disposal costs already discussed above.

Decision Matrix: When ETF, When Direct

The ETF-versus-direct decision maps cleanly onto account structures and position characteristics. The matrix below reduces the choice to a small set of input questions and produces a defensible answer for most common scenarios. Edge cases benefit from professional tax advice, but the typical retail scenario fits one of the patterns below.

Choose ETF when

- The allocation lives inside a tax-advantaged retirement account (US IRA, UK SIPP, similar EU pension wrappers). Direct Bitcoin in these accounts requires specialised self-directed structures with annual fees that often exceed the ETF expense ratio drag.

- The allocation lives inside a UK ISA wrapper. ISA-eligible Bitcoin ETPs shelter gains from CGT entirely up to the £20,000 annual allowance — a tax efficiency that direct Bitcoin holdings cannot match.

- The position size is small relative to portfolio (under approximately 2-3% of investable assets). Operational complexity of self-custody is not justified for small positions.

- Operational responsibility for self-custody is uncomfortable. Investors who would lose sleep over key management often hold ETFs more durably than direct positions, which matters more than the small expense-ratio drag.

- The investor is not yet ready for hardware wallet setup. ETF exposure is preferable to leaving direct Bitcoin holdings on an exchange indefinitely.

- Frequent rebalancing inside a single account is the strategy. ETF shares trade in fractional units within standard brokerage workflows; direct Bitcoin rebalancing requires more deliberate transaction management.

Choose direct ownership when

- The allocation is a strategic conviction holding intended for multi-decade horizons. Cumulative expense-ratio drag becomes meaningful over long periods and on large positions.

- The position is large enough to justify the operational setup (typically over $5,000-$10,000, depending on personal time value).

- Self-sovereignty matters as a property of the holding. Bitcoin's original use case — keys you control, no intermediary, no business-hours dependency — is preserved only with direct ownership.

- Tax-loss harvesting on direct Bitcoin is part of the strategy (US-specific advantage given current wash-sale rule treatment).

- Cross-border mobility matters. Direct Bitcoin can move across borders without intermediary cooperation; ETF shares require an intermediary in each jurisdiction.

- The investor is comfortable with hardware wallet setup and the operational discipline of self-custody. Comfort with the responsibility is a precondition.

Many investors hold both

The most common serious-investor pattern in 2026 holds both. ETFs occupy the retirement and tax-advantaged accounts where direct Bitcoin is impractical. Direct Bitcoin holdings live in self-custody for the strategic conviction allocation.

Together, the structure captures the wrapper benefits of ETFs and the long-term cost efficiency of direct ownership without forcing a single choice. The portfolio allocation framework in our portfolio allocation guide covers the sizing logic across both wrapper structures.

Conclusion

The ETF-versus-direct decision is not a referendum on Bitcoin's nature or on financial system trust. It is an account-structure decision shaped by tax wrapper, position size, operational comfort and time horizon.

The framework reduces to a small set of questions:

- Does the allocation live inside a retirement or ISA wrapper?

- Is the position size meaningful enough to justify operational setup?

- Does self-sovereignty matter to you as a property rather than just a slogan?

The answers map cleanly onto the appropriate path, and most serious investors arrive at a hybrid structure where each path occupies the account types it serves best.

Practical next steps by investor profile

The framework converts into different concrete actions depending on investor profile:

- US investor with retirement account capacity — ETF allocation inside the IRA/401(k) is the highest-leverage decision. Open or use existing brokerage IRA, allocate to IBIT or FBTC based on expense ratio and AUM preference, and run the contribution as a standard portfolio allocation. Add direct Bitcoin in taxable accounts if conviction warrants the operational setup.

- UK investor with ISA capacity — Begin with ISA-eligible Bitcoin ETPs through Hargreaves Lansdown, IG, AJ Bell or Trading 212. ISA wrapper benefit dwarfs the expense-ratio drag over multi-decade horizons. Direct holdings sit in taxable accounts only after ISA capacity is fully utilised.

- EU investor — Country-specific. German and Portuguese investors typically benefit from direct holdings (12-month tax-free rule). French investors face neutral wrapper choice (flat 30% PFU). Dutch investors face wealth tax regardless of structure. Verify with local accountant before structuring.

- Investor with strategic conviction allocation above approximately $50,000 — Direct ownership becomes operationally justified at this threshold regardless of jurisdiction. The expense-ratio savings over multi-decade horizons pay back the operational complexity of self-custody many times over.

The execution detail for direct ownership — exchange selection, recurring purchases, hardware wallet setup, seed-phrase storage, recovery testing — sits in our DCA playbook.

For investors choosing the ETF path, the next step is opening a standard brokerage account in your jurisdiction and selecting an issuer based on expense ratio and AUM scale. For investors choosing direct ownership, the next step is exchange selection followed by hardware wallet setup. Either path is defensible. The cluster's framework supports both.

Sources

- U.S. Securities and Exchange Commission — spot Bitcoin ETF approval orders and ongoing oversight

- UK Financial Conduct Authority — UK retail Bitcoin ETP approval and ISA-eligibility framework

- HM Revenue and Customs — UK capital gains tax treatment of Bitcoin and ETP holdings

- Internal Revenue Service — US Bitcoin tax treatment as property and current wash-sale guidance

- EUR-Lex — EU MiCA framework affecting Bitcoin treatment across member states

- Bitcoin Investment Fundamentals: Post-Cycle Strategy Guide

- The Bitcoin Cycle in 2026: ETF Flows Reshape Halving Dynamics

- Bitcoin Portfolio Allocation

- Bitcoin DCA Strategy Playbook

- Bitcoin Review: Investment Analysis

- Crypto vs Stocks: Asset-Class Comparison

Frequently Asked Questions

- What is a spot Bitcoin ETF?

- A spot Bitcoin ETF is a regulated investment fund that holds actual Bitcoin in cold storage with an institutional custodian and issues shares that trade on traditional stock exchanges. Each share represents a proportional claim on the underlying Bitcoin. The price tracks the spot Bitcoin price closely, minus the fund's annual expense ratio. US-listed examples include BlackRock's IBIT, Fidelity's FBTC and ARK 21Shares' ARKB. Spot ETFs differ from earlier futures-based products that held Bitcoin futures contracts rather than the asset itself.

- Are Bitcoin ETF returns the same as holding Bitcoin directly?

- Returns track each other closely but are not identical. ETFs deduct an annual expense ratio (0.20-0.25% across most major US issuers) which compounds against direct holdings over multi-year horizons. ETFs also experience small tracking errors during volatile periods and trade at small premiums or discounts to NAV during stress. Direct Bitcoin has no expense ratio but does have transaction and custody friction. Over a 10-year horizon at typical expense ratios, ETF holders give up approximately 2-2.5% of cumulative return relative to perfect direct ownership.

- Which is safer: a Bitcoin ETF or self-custody?

- The risks differ rather than one being uniformly safer. ETFs carry custodian risk and issuer risk, which are very low for major issuers but not zero. Self-custody removes counterparty risk entirely but introduces operational risk — lost seed phrases, hardware failure, supply-chain compromise. Both are safe enough for serious holdings if executed properly. The historical pattern of large retail losses has come from custodial exchange failures rather than from major-issuer ETFs or properly-executed self-custody.

- Can I hold a Bitcoin ETF inside a UK ISA?

- Yes. Several UK-listed Bitcoin ETPs are eligible for ISA wrappers and can be held through brokers including Hargreaves Lansdown, IG, Trading 212 and AJ Bell. Holding Bitcoin exposure inside a Stocks and Shares ISA shelters gains from capital gains tax and dividend tax up to the annual ISA allowance, which can produce a meaningful long-term advantage over direct Bitcoin holdings that remain subject to CGT on disposal. Verify ISA eligibility with your broker before allocating, as product availability has shifted over time.

- Can I hold direct Bitcoin in a US retirement account?

- Yes, but only through a self-directed IRA with a specialised cryptocurrency custodian rather than through a standard brokerage IRA. Custodians including BitcoinIRA, iTrustCapital and Unchained offer self-directed accounts that can hold direct Bitcoin in custodial or multi-signature structures. Setup and annual fees range from $200-500, which often offsets the wrapper benefit for smaller positions. For most US investors, holding a spot Bitcoin ETF inside a standard brokerage IRA is the simpler path that captures most of the tax-deferral benefit.