Bitcoin Cycle 2026: Post-Halving Reality Explained

The four-year halving cycle that worked from 2012 to 2024 has weakened. Spot ETF flows now dominate price discovery. This satellite walks through the evidence, the mechanism, what it means for your investment approach, and the limitations of the thesis honestly.

Introduction

Bitcoin's four-year halving cycle was the most reliable price-prediction model in the asset's history. From November 2012 through May 2020, three completed cycles produced a recognisable pattern: post-halving year strength, peak in the year after halving, drawdown of 70-85% over the following two years, accumulation through the next halving.

Investors who internalised the model and timed entries and exits accordingly outperformed both buy-and-hold investors and active traders. The model worked because miner-issued supply was the dominant new-Bitcoin flow, and demand growth was relatively steady year over year. Few asset-specific price models in any market have produced three out of three confirmation cycles with a clean mechanism. Bitcoin's halving cycle was an exceptional model in a field full of failed ones.

The model has weakened. The fourth halving in April 2024 was preceded by the launch of US spot Bitcoin ETFs in January 2024. The ETFs immediately began absorbing Bitcoin at scales unprecedented in the asset's history. Within a year of launch, the ETF complex held more Bitcoin than typical annual mining issuance produces.

The supply-demand math no longer holds the same way. When demand-side institutional flows can move more BTC in a quarter than miners produce in a year, the supply-side halving signal becomes a smaller part of the price equation. The 2025 calendar year produced the first empirical confirmation that something has shifted: it was the first post-halving year in Bitcoin's history to finish negative, contradicting every prior pattern.

Why does this matter for the individual investor? Because most Bitcoin commentary you read in 2026 is still operating under the older cycle assumptions. Predictions of "the cycle peak in late 2025" came and went without a peak. Strategies built around halving-dated entry and exit produced no statistical edge in 2024-2025. Investors who had positioned for the historical post-halving rally either gave back gains during the 2025 chop or sat in cash waiting for a top that never came.

This satellite analyses the shift in detail. We cover what worked from 2012 to 2024, what changed in 2024, the mathematical comparison between ETF flows and mining supply, the 2025 evidence, the demand-driven framework that may replace the cycle model, the investor implications, and an honest section on what could disprove the thesis. By the end you should be able to read 2026 Bitcoin commentary critically and distinguish framework-aware analysis from analysis still operating under the older assumptions.

If you arrived from our Bitcoin investment fundamentals hub, this satellite gives the analytical depth on the cycle thesis the hub introduces at framework level. The investor-implications section connects back to the allocation framework in our portfolio allocation satellite.

Traditional Halving Cycle Recap (2012-2024)

Bitcoin's first three completed cycles followed a remarkably consistent pattern that underpinned a decade of price-prediction analysis. Block reward halvings in November 2012, July 2016 and May 2020 each cut new BTC issuance by 50%, mechanically tightening supply against steady or growing demand. Each halving was followed within 12 to 18 months by a price peak, then a multi-year drawdown of 70-85% before the next cycle began.

Why the model worked

Three factors made the four-year cycle reliable.

First, the halving's effect on new supply was mechanically large relative to total demand. At the 2012 halving, the daily issuance reduction was a meaningful share of daily Bitcoin demand.

Second, demand growth was relatively steady year over year, dominated by retail accumulation rather than by lumpy institutional flows.

Third, the four-year duration was long enough for supply tightening to compound through multiple market participants' rebalancing decisions. The model worked because the halving was the largest single flow event in Bitcoin's market, occurring on a predictable schedule.

The three completed cycles

The 2012-2014 cycle saw Bitcoin rise from approximately $12 at the November 2012 halving to above $1,100 in late 2013. It was followed by an 85%+ drawdown to roughly $200 by early 2015.

The 2016-2018 cycle saw Bitcoin rise from roughly $650 at the July 2016 halving to approximately $20,000 in December 2017. It was followed by an 84% drawdown to roughly $3,200 by December 2018.

The 2020-2022 cycle saw Bitcoin rise from roughly $8,500 at the May 2020 halving to approximately $69,000 in November 2021. It was followed by a 77% drawdown to roughly $15,500 by November 2022.

What investors learnt

Investors who internalised the four-year cycle developed accumulation and distribution strategies aligned to the schedule:

- Accumulation in the post-drawdown years (2015, 2019, 2023)

- DCA through the halving year (2016, 2020, 2024)

- Distribution in the year following halving (2017, 2021, expected in 2025)

- Re-accumulation through the next drawdown

The strategy outperformed buy-and-hold because Bitcoin's drawdowns were deep enough that timing the rotation between holding and trimming meaningfully improved compound returns. It outperformed active trading because the four-year duration was long enough that most retail traders gave back gains through transaction friction and timing errors.

The model's track record

Through 2024, the four-year cycle thesis had three out of three confirmation cycles, no failed cycles, and a clear mechanism. Few asset-specific price models in any market have that confirmation rate.

The model's strength was also its vulnerability. Its perfect track record encouraged investors to weight the thesis heavily. Evidence of the model breaking would carry meaningful surprise weight in the market when it arrived.

What Changed: The 2024 ETF Approval

The single largest structural change to Bitcoin's market dynamics in its history occurred on 10 January 2024. The US Securities and Exchange Commission approved eleven spot Bitcoin ETFs simultaneously.

The approval ended a near-decade of rejected applications and unlocked institutional Bitcoin demand that had been partially blocked by the lack of an ordinary brokerage-account vehicle. The market response was immediate and unprecedented.

The institutional unlock

Before the ETF approval, US institutional investors faced significant friction in obtaining Bitcoin exposure. Fiduciary responsibilities prevented many pension funds, endowments and wealth managers from holding direct Bitcoin or from using crypto-native exchanges as custodians. Bitcoin futures-based products existed but had structural problems — contango, roll yield, tracking error — that limited adoption.

The 2024 spot ETF approval removed these frictions. Institutional investors could now obtain Bitcoin exposure through standard brokerage accounts with regulated custodians, ordinary fiduciary structures and standard ETF reporting. Institutional flow entered Bitcoin at scales that dwarfed earlier retail-driven accumulation.

The first-year accumulation

The eleven launch ETFs and several products that followed accumulated cumulative net inflows that significantly exceeded analyst expectations. Cumulative inflows reached the tens of billions of dollars during 2024 alone, with daily flows on strong-sentiment days exceeding $500 million.

BlackRock's IBIT emerged as the dominant issuer, surpassing $50 billion in AUM within roughly a year of launch (by 2024-2025) — a growth rate that no prior ETF in any asset class had matched at the same stage.

The market structure implications

The institutional flow had three immediate effects on Bitcoin's market structure.

First, daily liquidity deepened materially as ETF market-makers added to the order book on both sides during normal trading hours.

Second, volatility patterns shifted from retail-driven sentiment swings towards institutional-rebalancing-driven flows aligned to traditional financial markets.

Third, price discovery shifted from being dominated by crypto-native exchanges to being increasingly influenced by US trading-hours flows in the ETF complex. Crypto-native exchanges adjusted to the ETF reference rather than leading it.

The cumulative position

By early 2026, the US spot Bitcoin ETF complex held a position that represents a meaningful share of Bitcoin's liquid supply. BlackRock's IBIT alone holds on the order of 770,000 BTC as of mid-2026, representing roughly 4% of total Bitcoin supply ever to be created (out of the 21 million maximum).

The full ETF complex including all major issuers holds materially more. The concentration represents a structural change in Bitcoin's holder distribution that did not exist in any previous cycle.

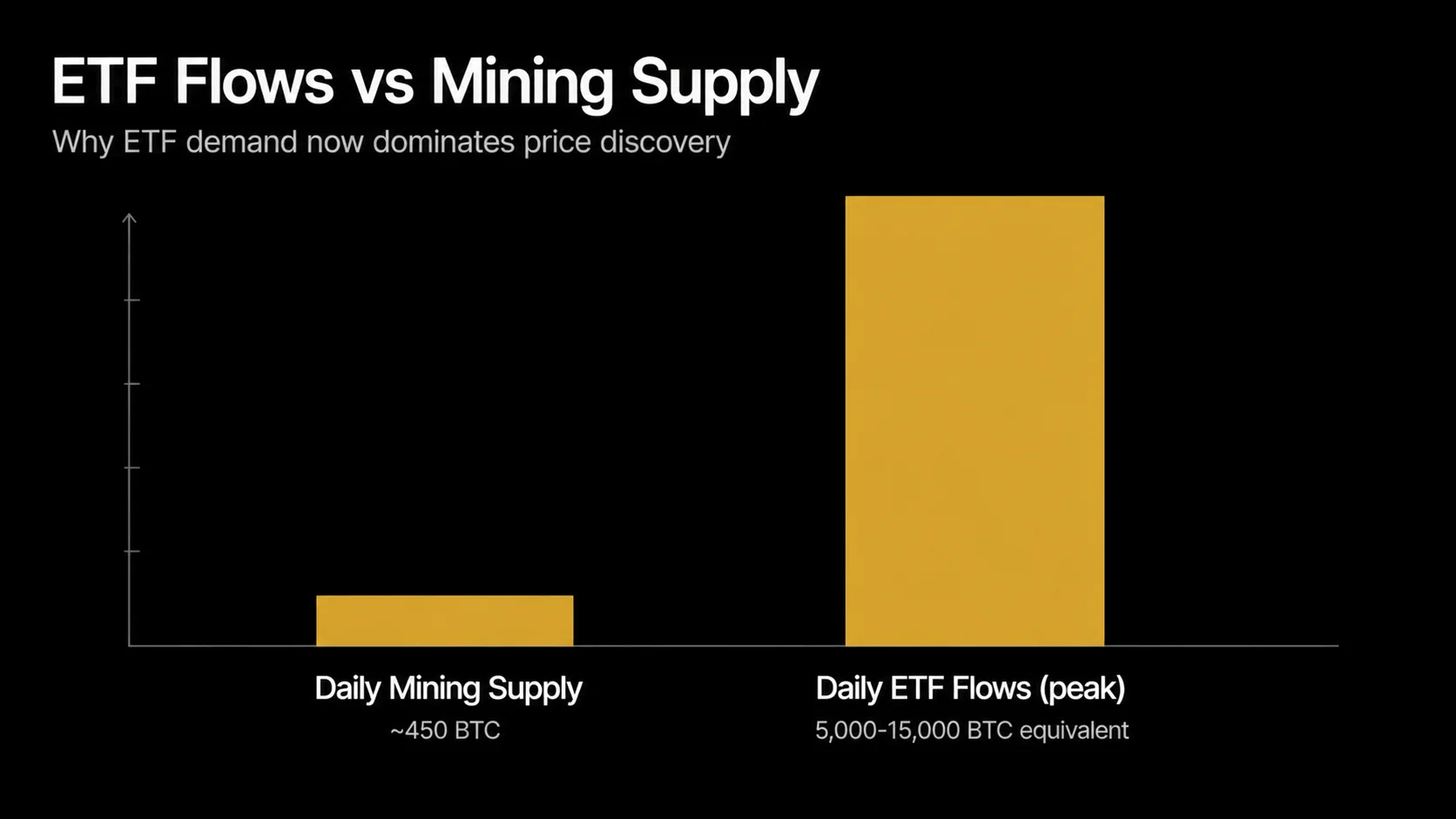

ETF Flows vs Mining Supply

The mathematical comparison between ETF flows and mining supply is the foundation of the cycle-shift thesis. Understanding the magnitudes makes the price-discovery shift concrete rather than abstract.

Daily mining issuance after April 2024

The April 2024 halving reduced Bitcoin's block reward from 6.25 BTC per block to 3.125 BTC per block. With approximately 144 blocks produced per day, daily mining issuance after April 2024 runs at approximately 450 BTC per day.

At a Bitcoin price of around $63,000 (the mid-2026 level; the actual price varies), 450 BTC represents roughly $28 million of new supply entering the market each day. This is the fundamental supply flow that the four-year cycle thesis was built around.

Daily ETF flows in the post-approval era

US spot Bitcoin ETF daily net flows during 2024-2025 averaged in the low hundreds of millions of dollars during normal periods. Peak days regularly exceeded $500 million on strong sentiment, with occasional days surpassing $1 billion.

At typical Bitcoin prices, $500 million in daily inflows represents thousands of BTC moving from the broader market into ETF custody on a single day. The order of magnitude difference is approximately 10-20 times the daily mining supply during peak flow periods.

What the magnitude difference means

The flow comparison matters because it determines which side of the supply-demand equation drives short-term price discovery.

When daily mining supply was the largest predictable flow in Bitcoin's market — true through 2023 — the supply-side halving signal dominated. When daily ETF flows can be 10-20 times larger than daily mining supply — true during 2024-2025 — the demand side dominates.

The halving still affects supply mathematics, but its signal has weakened relative to the louder ETF flow signal.

Bitwise's projection

Bitwise published a notable projection during the 2024-2025 period: US spot Bitcoin ETFs could absorb more than 100% of new Bitcoin issuance during 2026, depending on flow patterns. If realised, this would mean the entire annual mining output of approximately 164,250 BTC (450/day × 365) would be absorbed by ETF accumulation alone, with no net supply remaining for the broader market.

The projection's accuracy is debatable, but the magnitude illustrates the scale of demand-side flow relative to supply-side mining in the post-ETF era.

The structural implication

When demand-side flows of this magnitude become a persistent feature of Bitcoin's market structure — rather than a one-off institutional adoption event — the relationship between supply changes (halvings) and price changes (cycle peaks and troughs) is mediated through the demand layer.

A halving still tightens supply. But if demand flows are 10-20 times larger and varying significantly month-to-month, the supply tightening can be entirely overwhelmed by demand changes in either direction. This is the mechanism through which the four-year cycle has weakened as a price-prediction tool.

2025 Evidence: First Negative Post-Halving Year

The 2025 calendar year provides the first empirical test of the cycle-shift thesis. Under the traditional four-year cycle model, 2025 — the year following the April 2024 halving — should have been a strong-positive year, mirroring the patterns of 2013, 2017 and 2021. Bitcoin underperformed those expectations materially.

The 2025 price path

Bitcoin opened 2025 around $93,000, near its late-2024 highs, with sentiment positioned for the historical post-halving rally. The year delivered a rally — but not a durable one.

Bitcoin pushed to a new all-time high of around $126,000 on 6 October 2025, then reversed sharply, closing the year near $87,000 — approximately 6% below its January open. That negative full-year close contradicts every prior post-halving-year pattern, and by mid-2026 the price had fallen further, to around $63,000.

The drawdowns within the year were milder than the violent corrections of earlier cycles, which itself is a marker of the post-ETF era's volatility compression. The cumulative direction was negative rather than the strongly-positive direction the cycle model predicted.

What this evidence shows

One year of contradicting evidence does not prove the cycle has ended. Single-cycle samples are statistically thin.

What the year does show is that the model's confirmation track record has dropped from 3-of-3 to 3-of-4. The 2025 result is consistent with multiple alternative explanations:

- A weakening of the four-year cycle as ETF flows replace it as the dominant signal

- A delayed cycle that will produce its strong-positive year in 2026 instead of 2025

- A permanent shift to a different cycle structure that no longer follows the four-year pattern

- A combination of all three

The volatility compression context

Beyond the direction, the magnitude of 2025's moves matters.

Earlier post-halving years had produced 200-500%+ rallies followed by 50%+ drawdowns within the same year. 2025 produced none of that. The year was characterised by 30-40% maximum drawdowns and similarly modest rallies, well below the volatility characteristic of prior cycles.

This volatility compression is consistent with the institutional-flow hypothesis. When institutional holders smooth the order book, both upside and downside extremes become less common. This produces a different shape of year regardless of the year's net direction.

The bear case for the thesis

Defenders of the traditional cycle model offer two responses to the 2025 evidence.

First, that 2025 represents a delayed cycle where the strong-positive year occurs in 2026 rather than 2025. The ETF approval may have pulled forward demand into 2024 and shifted the cycle phase by a year.

Second, that 2025's flat-to-negative result is consistent with previous post-halving years' early periods. 2013 and 2017 were not uniformly positive throughout the entire year — both had multi-month consolidation phases.

These defences are reasonable hedges against premature thesis acceptance. The responsible analytical position is to weight the cycle-shift thesis against them rather than to assert the cycle is definitively broken.

The 2026 watch points

The 2026 calendar year is the critical test for the thesis.

If 2026 produces a strongly-positive year mirroring 2017 and 2021, the cycle-shift thesis weakens. The more likely interpretation would be that the 2024-2025 ETF dynamics merely shifted the cycle phase.

If 2026 produces another flat or negative year, the cycle-shift thesis strengthens and the four-year model can be reasonably considered weakened. The investor implication is to remain framework-aware rather than committed to either thesis until the evidence resolves.

A New Frame: Demand-Driven, Not Supply-Driven

If the four-year cycle has weakened as a price-prediction tool, what replaces it? No single replacement model has fully matured.

The most defensible framework treats Bitcoin as a globally-traded macro asset. Its price reflects the balance of net flows into the asset versus net selling pressure, mediated by global liquidity conditions and the relative attractiveness of competing assets.

The demand-driven framework

Under the demand-driven framework, Bitcoin's price discovery is dominated by net institutional and retail flows rather than by the mining supply schedule.

The major flow categories are:

- Spot ETF net inflows — the largest demand-side flow in the post-2024 era

- Corporate treasury accumulation — MicroStrategy and similar institutional holders

- Sovereign and quasi-sovereign accumulation — small but growing

- Retail accumulation through DCA programmes

- Offsetting selling pressure — miner liquidations, profit-taking by holders, large institutional redemptions

The net of these flows against total available supply (mining issuance plus holder selling) determines short-term price direction.

Macro liquidity as primary driver

Within the demand-driven framework, the primary macroeconomic input is global liquidity. Three components matter most:

- Federal Reserve policy — rate decisions, quantitative tightening or easing, balance sheet posture

- Dollar liquidity — DXY index movements, eurodollar conditions

- Yields on competing assets — Treasury yields, especially the 10-year and TIPS

Periods of liquidity expansion tend to correlate with Bitcoin strength as institutional risk appetite increases. Periods of liquidity tightening tend to correlate with Bitcoin weakness as the same flows reverse.

The new cycle approximation

If a new cycle structure is emerging in the post-ETF era, it appears more aligned with global macro liquidity cycles than with the four-year halving schedule.

Macro cycles typically run shorter than four years. The average post-WWII US business cycle has been roughly 5-6 years from peak to peak, with substantial variation. Bitcoin's cycle in the post-ETF era may be both shorter and more macro-aligned than its earlier supply-driven cycles.

This is speculative — the post-ETF era is too short to establish the new pattern empirically. It is the most defensible projection given the evidence so far.

What the framework implies operationally

Operationally, the demand-driven framework redirects investor attention from halving dates to flow indicators. The relevant data points are weekly ETF flow numbers (CoinShares publishes them), Federal Reserve policy posture, dollar liquidity indicators, and the relative yield environment in competing assets.

These indicators are more numerous and noisier than the halving dates. Short-term price prediction becomes harder rather than easier under the new framework. The compensating advantage is that the framework is more honest about the actual drivers of price in the post-ETF era.

Three Drawdown Profiles to Watch Through 2026

If the cycle thesis is genuinely shifting from supply-driven to demand-driven dynamics, drawdown patterns are where the change becomes operationally visible to retail investors. Three profiles cover most of the scenarios that 2026 might produce, and recognising which profile you are observing in real time helps you respond appropriately.

Profile 1: Macro-driven shallow drawdowns (30-40% peak-to-trough)

The most likely 2026 pattern under the demand-driven thesis is moderate drawdowns triggered by macro liquidity tightening rather than Bitcoin-specific weakness. Federal Reserve hawkish surprises, sustained dollar strength, or rising real yields can compress Bitcoin alongside other risk assets. The drawdowns last 3-6 months, reach 30-40% from local highs, and recover when macro conditions reverse.

How do you recognise this profile in real time? The key signals are correlation patterns. If Bitcoin is falling alongside equities, gold and other risk-on assets while the dollar strengthens and Treasury yields rise, you are observing a macro-driven drawdown. If Bitcoin is falling while traditional risk assets remain stable or rise, the cause is more likely Bitcoin-specific.

The operational response to macro-driven drawdowns is straightforward: continue your DCA programme, do not panic, and resist the temptation to either pause or accelerate the schedule. Macro drawdowns recover when macro conditions recover — they do not respond to your trading actions, and trying to time the recovery typically produces worse outcomes than mechanical accumulation.

Profile 2: ETF-flow-reversal deeper drawdowns (40-60%)

A more concerning scenario is sustained outflows from the spot Bitcoin ETF complex producing structural selling pressure that the rest of the market cannot absorb. The mechanism: investors who allocated to Bitcoin via ETFs during enthusiastic periods rotate out during weak ones, and because the ETF complex now holds a meaningful share of liquid Bitcoin supply, sustained outflows materially affect price.

This profile would manifest as drawdowns of 40-60% lasting 6-12 months, with weekly ETF flow data showing consistent net outflows above $500 million. Unlike macro-driven drawdowns, this pattern would not necessarily correlate with broader risk-asset weakness — Bitcoin could fall while equities remain stable.

The operational response remains DCA continuation, but with two adjustments. First, review whether your allocation tier was correctly sized — if a 50% drawdown produces strong urge to sell, your tier was probably too aggressive and the drawdown is information about your true behavioural tolerance. Second, if your DCA programme accumulates Bitcoin into significant balances on exchanges during the drawdown, prioritise moving funds to hardware wallet self-custody. Exchange custody risk increases during sector-wide stress.

Profile 3: Crisis-style deep drawdowns (60%+)

The lowest-probability but highest-impact scenario is a 60%+ drawdown driven by combined factors — macro tightening, ETF outflows, and a Bitcoin-specific event such as a major exchange failure or regulatory shock. This profile resembles 2022's drawdown, which was 75% peak-to-trough and lasted approximately 18 months.

Crisis drawdowns are the most behaviourally challenging because they last long enough that the loss feels permanent. Investors who hold through them with their allocation tier intact emerge with substantially better long-term outcomes than those who sell at the trough, but the discipline required is genuinely difficult.

The operational response is the same as the other profiles, with one addition: during 60%+ drawdowns, deliberately reduce the frequency at which you check Bitcoin prices. Daily price-checking during deep drawdowns produces emotional pressure that compounds the difficulty of holding. Weekly or monthly checks are sufficient for portfolio management purposes and substantially easier behaviourally.

What this means for your 2026 plan

Your DCA schedule, allocation tier and custody approach should all be configured for Profile 3 even though Profile 1 is most likely. Configuring for the worst case ensures the better cases are also handled correctly. The opposite — configuring for the best case and hoping the worst does not arrive — produces the panic-selling outcomes that retail investors most consistently regret.

Three concrete adjustments are worth making now if you have not made them already. Review your allocation tier honestly. Move accumulated Bitcoin above $1,000 to hardware wallet self-custody if you have not done so. Document your DCA schedule so that you can resume it if interrupted, even if the interruption lasts months. None of these adjustments depends on which drawdown profile materialises, and all of them improve outcomes regardless.

How to Read 2026 Cycle Commentary

Most Bitcoin analysis published in 2026 still operates under cycle-era assumptions, even when its specific predictions have failed. Reading it critically requires recognising the patterns that distinguish framework-aware commentary from commentary that has not yet caught up to the new reality.

Three patterns that signal outdated framework

Be cautious of analysis that contains any of these patterns:

- Halving-anchored timing predictions — claims like "the cycle peak should arrive in November 2025" or "we are entering the post-halving accumulation phase". These predictions assume the four-year structure remains the dominant signal. The 2025 evidence has weakened that assumption. Predictions anchored to halving dates without adjustment for ETF flow dynamics deserve heavier scepticism than they would have received in earlier cycles.

- Stock-to-flow model citations — references to PlanB's stock-to-flow model or its derivatives as serious price-prediction tools. The model has produced predictions that diverged materially from outcomes since 2021. Its mechanism — supply scarcity as primary price driver — is exactly the mechanism that has weakened in the post-ETF era. Authors still citing stock-to-flow are usually either anchoring to legacy thesis or have not updated their framework.

- "This time is different" handwaving — analysis that acknowledges 2025's failure to follow the historical pattern but explains it through one-off narratives (specific macro events, regulatory developments, sentiment shifts) rather than through structural change. Sometimes one-off explanations are correct, but commentary that consistently uses them to defend a model whose mechanism has weakened is not framework-aware.

Three patterns that signal framework-aware commentary

Quality cycle commentary in 2026 tends to share these patterns:

- Flow-based analysis — discussion that treats weekly ETF flows, sovereign accumulation, miner liquidations and macro liquidity as primary inputs. CoinShares fund flow reports, ETF flow trackers, and macro liquidity dashboards are typically the data sources.

- Honest uncertainty about mechanism — explicit acknowledgement that the demand-driven framework is provisional and has not yet been tested across multiple cycles. The best 2026 commentary names the alternative interpretations rather than committing to one.

- Decoupled investor implications — recommendations for position sizing, accumulation discipline and risk management that produce reasonable outcomes regardless of which framework prevails. Authors who hedge their predictions but still give actionable guidance are typically more useful than authors who commit to a specific cycle interpretation.

What to monitor through 2026

For investors who want to track the thesis as evidence accumulates, four data points matter most:

- Weekly ETF net flows — published by CoinShares with a one-week lag. Sustained inflows above $1 billion per week strengthen the demand-driven framework. Sustained outflows weaken it.

- Bitcoin's calendar 2026 performance — a strong-positive year supports the delayed-cycle interpretation. A second flat or negative year strengthens the cycle-shift framework.

- Drawdown shape and depth — drawdowns of 30-50% with extended duration support the institutional-smoothing interpretation. A sharp 70-85% drawdown timed to historical schedule supports cycle-return.

- Federal Reserve policy correlation — strengthening correlation between Fed liquidity conditions and Bitcoin price supports the macro-mediated framework. Decoupling from macro conditions would suggest Bitcoin-specific factors are reasserting themselves.

None of these data points provide a complete picture on their own. Together they form a triangulation that helps you adjust your framework weighting as 2026 evidence accumulates over the months ahead. The investor who tracks all four indicators across 2026 will have substantially better calibration on which framework dominates than the investor who relies on any single signal in isolation.

Investor Implications

The cycle-shift thesis has practical implications for how retail investors approach Bitcoin allocation, accumulation and exit decisions. The implications differ from cycle-aware strategies that worked in earlier eras.

Cycle-timing has lost its edge

Strategies built around halving-dated entry and exit have lost their statistical edge.

Investors who held cash through the post-halving accumulation phase and then bought at the halving expecting the historical rally have been disappointed in 2025. Investors who positioned for cycle-peak exit in late 2025 found no peak to exit. The four-year cycle as a market-timing tool has not produced the same outperformance over buy-and-hold that it did in earlier eras.

Position sizing matters more

If cycle-timing has lost its edge, what replaces it? Position sizing relative to total wealth and behavioural tolerance becomes the dominant input — covered in detail in our portfolio allocation framework.

The right Bitcoin allocation in a post-cycle world depends on three controllable inputs: what drawdown you can sustain behaviourally, what time horizon supports the position, and what wrapper structure you have available. None of these depend on cycle predictions, which means they produce defensible outcomes regardless of how the cycle thesis resolves.

DCA dominates more strongly than before

Dollar-cost averaging has always had advantages over lump-sum entries for Bitcoin. The cycle-shift thesis strengthens those advantages.

In a world where the four-year cycle reliably produced a clear timing model, lump-sum entries during accumulation phases could outperform DCA. In a post-cycle world where timing models have weakened, DCA's structural advantages — averaging out timing risk, smoothing entry prices, reducing regret risk — become more reliable. Our DCA playbook covers the execution detail.

Watch ETF flows and macro liquidity

For investors who want some directional input despite the weakening of cycle-based timing, the most useful indicators in the post-ETF era are weekly ETF flow data (CoinShares publishes them with a short delay), Federal Reserve policy posture and announcements, and dollar liquidity indicators.

These are noisier inputs than the halving dates and require more sophistication to interpret. They are the actual inputs that drive Bitcoin price in the demand-driven framework. Long-term investors do not need to monitor these closely. Tactical allocators who want to lean into flows do.

Drawdowns may not follow historical patterns

The drawdown patterns of the previous three Bitcoin cycles — 70-85% peak-to-trough drawdowns occurring in years 2-3 after halving — may not repeat in the post-ETF era.

The volatility compression of the 2024-2025 period suggests drawdowns may be both shallower (40-50% rather than 70-85%) and less synchronised with the halving schedule. Investors planning re-accumulation during expected cycle troughs may find the troughs less deep and the timing less predictable.

Allocation sizing should remain conservative enough to absorb 50% drawdowns regardless of when they occur, rather than betting on cycle-aligned drawdown timing.

Limitations of the Thesis

Honest analysis includes the conditions under which a thesis would be wrong. The cycle-shift thesis has multiple plausible scenarios under which it would fail or partially fail.

The single-sample problem

One year of evidence (2025) is statistically thin. A single cycle that contradicts the four-year model is consistent with multiple explanations beyond "the cycle has shifted permanently".

The 2025 result could be a one-off anomaly that does not repeat in subsequent cycles. The responsible analytical position is to weight the cycle-shift thesis as a reasonable interpretation rather than as a confirmed fact, and to update the weighting as additional cycles produce additional evidence.

The delayed-cycle alternative

The 2025 evidence is also consistent with a delayed cycle where the strong-positive year occurs in 2026 rather than 2025. Under this interpretation, the ETF approval in early 2024 pulled demand forward into the pre-halving year, shifting the cycle phase by approximately one year without breaking the underlying four-year model.

If 2026 produces a strongly-positive year mirroring the historical post-halving rallies, this interpretation gains support and the cycle-shift thesis weakens. Investors should remain genuinely open to this possibility through 2026 rather than committing to the cycle-shift framework prematurely.

The ETF reversal scenario

The cycle-shift thesis depends on persistent ETF flow strength. If macro conditions produce sustained ETF outflows — a 2008-style financial crisis, regulatory restrictions on institutional Bitcoin allocation, or investor disillusionment with Bitcoin as an asset class — the demand-side dominance could weaken or reverse.

Under sustained ETF outflows, mining supply could re-emerge as the dominant flow, which would partially restore the four-year cycle's relevance. This scenario is unlikely in the base case but is not impossible.

The mechanism uncertainty

Even granting that the four-year cycle has weakened, the demand-driven replacement framework is provisional.

The framework treats macro liquidity as a primary driver, but the empirical relationship between macro liquidity and Bitcoin price has been variable across periods. Bitcoin sometimes correlates strongly with risk assets, sometimes with gold and inflation hedges, sometimes neither cleanly. The "demand-driven, macro-mediated" framework may itself be replaced by a different framework as more cycles produce more evidence.

What would change the conclusion

The cycle-shift thesis would weaken meaningfully under several specific scenarios:

- A 2026 calendar year producing a 200%+ rally that mirrors 2017 and 2021 would suggest the cycle is delayed rather than broken.

- Sustained ETF outflows during 2026-2027 would suggest the institutional adoption was a one-off rather than a structural change.

- A 2027-2028 drawdown of 70-85% timed to the historical schedule would suggest the cycle has returned.

Investors should genuinely watch for these scenarios rather than dismissing them, even if the base case remains the cycle-shift framework.

Conclusion

The four-year halving cycle that worked from 2012 to 2024 has weakened as a price-prediction tool. The mechanism is straightforward. ETF flows now dominate price discovery in ways that did not exist before January 2024, with daily flows that can exceed daily mining supply by an order of magnitude or more.

The 2025 calendar year provided the first empirical test, contradicting the historical post-halving-year pattern. The base-case interpretation is that Bitcoin's cycle has shifted from supply-driven (halving as primary signal) to demand-driven (ETF flows and macro liquidity as primary signals), with the halving still affecting supply mechanics but at a smaller weight in the overall flow balance.

The thesis is not yet proven. Multiple alternative interpretations remain consistent with the evidence, and the responsible analytical position is to weight the framework rather than commit to it. The 2026 calendar year is the critical test, and as of mid-2026 it is leaning against the delayed-cycle reading: Bitcoin set its all-time high back in October 2025 and has since fallen roughly 50%, with US spot ETF flows turning net-negative through the spring. A strong-positive year would suggest the cycle is delayed rather than broken. Another flat-or-negative year would strengthen the cycle-shift framework. Investors should remain framework-aware rather than committed to either interpretation prematurely.

The investor implication is robust regardless of which framework prevails. Position sizing, accumulation discipline, custody quality and tax-wrapper optimisation produce reliable outcomes that do not depend on cycle predictions. These are the controllable inputs that determine long-term Bitcoin investment success in either framework. Cycle-timing strategies that worked in 2012-2020 have lost their edge whether or not the cycle has fully shifted, because the conditions that made them work have at minimum weakened. Strategies built on the controllable inputs continue to work.

Sources

- Caleb & Brown — Is Bitcoin's Four-Year Cycle Broken? — analytical exploration of the cycle-shift thesis

- Amberdata — 2026 Outlook: The End of the Four-Year Cycle — institutional-grade research on the cycle shift

- BlockEden — analysis of institutional flows reshaping Bitcoin's market structure

- U.S. Securities and Exchange Commission — January 2024 spot Bitcoin ETF approval orders

- Federal Reserve — macro policy data referenced in the demand-driven framework

- Bitcoin Investment Fundamentals: Post-Cycle Strategy Guide

- Spot Bitcoin ETF vs Direct BTC

- Bitcoin Portfolio Allocation

- Bitcoin DCA Strategy Playbook

- What is Bitcoin? Technology and Investment

- Crypto vs Stocks: Asset-Class Comparison

Frequently Asked Questions

- Is the Bitcoin halving cycle dead in 2026?

- The cycle has evolved rather than died. The halving still affects supply mechanics, but its market signal has weakened materially as ETF flows have grown to dominate price discovery. The halving signal is still present, just smaller relative to demand-side ETF flows that did not exist in earlier cycles.

- What replaced the halving cycle as a price model in 2026?

- No single replacement model has matured fully. The most defensible framework treats Bitcoin as a globally-traded macro asset. Its price reflects net flows from institutional and retail buyers minus selling pressure from holders and miners, mediated by global liquidity conditions. ETF flows, Federal Reserve policy, dollar liquidity and yields on competing assets now influence Bitcoin at least as much as the mining schedule did in earlier cycles.

- How much do ETF flows really matter compared to mining supply?

- Daily mining issuance after the April 2024 halving runs at approximately 450 BTC per day. US spot Bitcoin ETF daily flows have regularly exceeded $500 million during strong sentiment periods, representing thousands of BTC moving on a single day. The flow magnitude can be more than 10 times larger than daily mining supply, which mechanically shifts price-discovery from the supply side to the demand side.

- Could the four-year cycle return in future Bitcoin cycles?

- It is possible but not the base case. For the cycle to return as dominant, ETF flows would need to recede materially relative to mining supply. That requires either a sustained reduction in institutional Bitcoin demand or significant ETF outflows. Both are plausible during severe macro stress but neither is the base-case expectation. The more likely outcome is that the cycle remains evolved into a demand-driven model that weights ETF flows alongside the mining schedule.

- What does the cycle thesis mean for my Bitcoin investment strategy?

- Cycle-timing strategies built around halving dates have lost their statistical edge. The strategies that suit the post-cycle era are consistent accumulation through DCA, position sizing relative to total wealth rather than cycle predictions, and willingness to hold through drawdowns that no longer follow the previous cycle's timing. The framework has shifted from "when to buy and sell" to "how much to hold and how to size".