Bitcoin Portfolio Allocation 2026: Sizing

A volatility-budget framework for sizing Bitcoin against total wealth — three allocation tiers, rebalancing mechanics, and how regional tax wrappers affect the optimal structure for US, EU and UK investors.

Introduction

Allocation sizing is the most important Bitcoin investment decision and the most underweighted in popular commentary. A 1% allocation that holds through a 70% drawdown produces meaningfully different outcomes — and behavioural experiences — from a 25% allocation that does the same.

Most retail investors who lose money on Bitcoin do so not because they bought the wrong asset, but because they sized the position incorrectly relative to their portfolio, time horizon and behavioural tolerance. The pattern is consistent across every Bitcoin cycle. Investors with 5% allocations rarely sell during drawdowns. Investors with 30% allocations frequently sell during drawdowns. The fundamental analysis of the asset rarely changes between these two outcomes — only the position size relative to total wealth.

Consider a concrete contrast. Two investors each have $500,000 (£400,000) of investable wealth. Investor A allocates 5%, holding $25,000 of Bitcoin. Investor B allocates 30%, holding $150,000 of Bitcoin. A 60% Bitcoin drawdown produces a $15,000 loss for Investor A — meaningful but absorbable, equivalent to 3% of net worth. The same drawdown produces a $90,000 loss for Investor B, equivalent to 18% of net worth. Investor A typically holds through the drawdown. Investor B typically does not. Five years later, when Bitcoin has recovered and exceeded its previous high, Investor A still holds the position and benefits. Investor B sold near the bottom and did not.

The asset performed identically in both cases. The investor experience differed because the sizing differed. This is the consistent pattern that makes allocation sizing the highest-leverage decision in Bitcoin investing — higher than entry timing, higher than exchange selection, higher than custody choice. None of those other decisions matter if you cannot hold the position through the drawdowns it will inevitably produce.

This satellite goes deeper into the allocation framework than the cluster hub introduces. We cover:

- The volatility-budget concept that underpins the three allocation tiers

- Conservative, balanced and aggressive tier sizing with concrete examples

- Rebalancing mechanics that determine after-cost performance

- The role of Bitcoin inside a 60/40 portfolio

- Wrapper-by-jurisdiction context that often dictates whether the allocation should be ETF or direct

The right allocation depends on time horizon, income stability, existing wealth concentration and demonstrated behavioural discipline rather than on price predictions. None of those inputs require forecasting Bitcoin's path. All of them are knowable about your own situation. The framework below gives a defensible answer for most retail scenarios, with concrete examples calibrated to portfolio sizes typical of UK and US retail investors and explicit notes for jurisdiction-specific tax structures that affect optimal sizing.

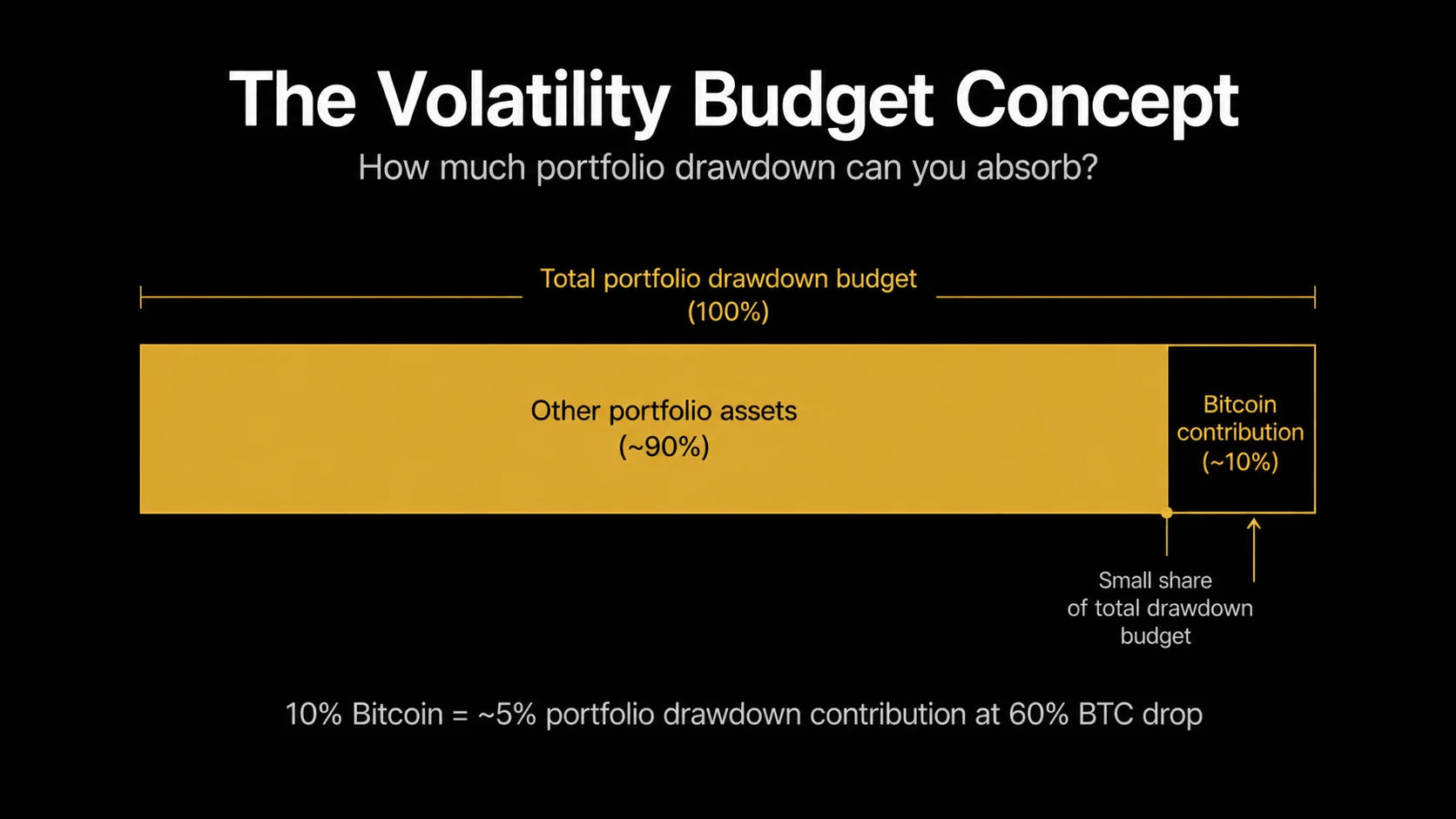

Why Sizing Matters: The Volatility Budget

The volatility budget is the maximum portfolio drawdown you can sustain without changing your behaviour or your financial plan. It is the foundation of every defensible Bitcoin allocation decision.

Most retail allocation mistakes trace back to sizing positions without explicitly thinking about what the worst plausible drawdown would do to the household balance sheet and to the investor's behaviour during the drawdown.

The working drawdown assumption

The defensible working assumption for Bitcoin in 2026 is that a 50-70% peak-to-trough drawdown is plausible from any entry point.

The post-ETF era has compressed Bitcoin's volatility somewhat compared with prior cycles. The 80%+ drawdowns of 2014, 2018 and 2022 are less likely as institutional holders smooth the order book. Drawdowns of 40-50% remain entirely plausible during macro shocks, sentiment shifts, or regulatory surprises. Allocation sizing should assume the worst plausible drawdown is roughly 50% rather than the 30% drawdowns more typical of equities.

Calculating your budget

The calculation is straightforward:

- Step 1 — take your total investable wealth (excluding primary residence and other illiquid assets that you would not sell to fund living expenses)

- Step 2 — multiply by the maximum drawdown you can sustain across all assets without changing your behaviour or financial plan (typically 20-30% for most retail investors)

- Step 3 — the result is your absolute volatility budget, which you allocate across asset classes weighted by their expected drawdown contribution

For Bitcoin specifically, an allocation of size N produces an expected worst-case drawdown contribution of approximately 0.5×N (using the 50% drawdown assumption). A 10% Bitcoin allocation contributes approximately 5% to the worst-case portfolio drawdown.

The behavioural dimension

The mathematical volatility budget is necessary but not sufficient. Behavioural tolerance is the second constraint, often binding more tightly than the mathematical one.

Most retail investors who sell Bitcoin at the bottom do so because the drawdown produced emotional pressure that exceeded their behavioural tolerance, not because the loss had reached an objective threshold. The behavioural budget is harder to estimate honestly — most investors overestimate their tolerance until tested. Investors who have held Bitcoin through prior drawdowns without selling have demonstrated a behavioural budget. Investors who have not yet been tested should size conservatively until they have.

Income stability and human capital

Income stability affects allocation through the worst-case scenario where a Bitcoin drawdown coincides with a job loss, business downturn or other income shock.

Investors with stable, diversified income — employed in growth industries, multiple income streams, robust emergency fund — can sustain larger Bitcoin allocations because their cash flow does not depend on the position. Investors with concentrated, cyclical or fragile income should size smaller, because the correlation between their personal income and risk-asset prices may be higher than they realise. Recessions tend to compress both simultaneously.

Human capital — the present value of future earnings — also matters. A 30-year-old with 35 years of earning ahead can absorb deeper drawdowns than a 60-year-old approaching retirement, even at the same current portfolio size.

Conservative Tier (1-5%)

The conservative tier treats Bitcoin as a small alternatives sleeve inside a traditional portfolio. Position sizes range from 1% (cautious exposure) to 5% (meaningful but limited).

This tier suits investors near retirement, those with concentrated single-stock or single-property wealth, anyone whose income cannot absorb a Bitcoin drawdown coinciding with a negative shock, and investors who have not yet demonstrated behavioural tolerance through a Bitcoin cycle.

The mathematical case

Concrete example: a 2% Bitcoin allocation in a $625,000 (£500,000) portfolio holds $12,500 of Bitcoin. A 50% drawdown costs $6,250 — a 1% hit to total portfolio value.

Most retail investors with stable income absorb a 1% portfolio drawdown without behavioural pressure regardless of asset-specific volatility. The position is large enough to matter on the upside (a 5x return adds $62,500 to portfolio value, scaling to $50,000 net of the original allocation) and small enough to be invisible on the downside.

Suitable scenarios

The conservative tier fits several specific scenarios:

- Investors within 5-10 years of retirement face sequence-of-returns risk where large drawdowns near retirement can permanently impair retirement income. Capping Bitcoin at 1-3% prevents this risk regardless of long-term return potential.

- Investors with concentrated single-stock or single-property wealth already carry substantial idiosyncratic risk. Adding a large Bitcoin allocation compounds rather than diversifies.

- Investors using Bitcoin as inflation hedge or geopolitical insurance want a small position that hurts very little if it underperforms and helps meaningfully if its insurance properties activate.

The behavioural calibration scenario

Investors who have not yet held Bitcoin through a major drawdown also belong in the conservative tier — regardless of their stated conviction. Behavioural tolerance is empirical: you do not know whether you can hold through a 60% drawdown until you have done so. Self-assessment consistently overestimates this capacity.

The conservative tier serves as a calibration period. Hold a 2-5% allocation through a complete cycle. If you find yourself reaching for the sell button during a 50%+ drawdown, your behavioural tolerance is genuinely conservative-tier and the original sizing was correct. If you find yourself wanting to buy more during the drawdown without anxiety, you have demonstrated the behavioural tolerance that supports moving to balanced or aggressive tier on the next cycle.

This calibration approach prevents the most common allocation mistake: investors who size for their imagined behavioural tolerance rather than their actual one, then sell at the worst moment when the imagined tolerance turns out to have been wrong.

Implementation pattern

Most conservative-tier allocations work better as ETF holdings inside a tax-advantaged account than as direct Bitcoin. The position size does not justify hardware wallet operational complexity. The wrapper benefit dominates the long-term return for retirement-account holdings. The simpler operational profile reduces the risk of operational errors that disproportionately affect small positions.

Specific patterns by region:

- US investors — IBIT or FBTC inside an IRA

- UK investors — ISA-eligible Bitcoin ETP through Hargreaves Lansdown, IG, Trading 212 or AJ Bell

- EU investors — regulated Bitcoin ETP appropriate to the investor's domicile under MiCA

Balanced Tier (5-15%)

The balanced tier treats Bitcoin as a meaningful but not dominant portfolio component. Position sizes range from 5% (moderate exposure) to 15% (substantial weight without dominance).

This tier suits investors with 10+ year horizons, stable diversified income, existing diversification across other asset classes, and demonstrated behavioural tolerance through at least one Bitcoin drawdown.

The mathematical case

Concrete example: a 10% Bitcoin allocation in a $625,000 (£500,000) portfolio holds $62,500 of Bitcoin. A 50% drawdown costs $31,250 — a 5% hit to total portfolio value.

Most investors with stable income and existing diversification absorb a 5% portfolio drawdown without behavioural pressure if they expected it. The same 50% drawdown at a 30% allocation removes 15% of total portfolio value, which produces forced selling regardless of prior conviction in a meaningful share of investors.

The 5-15% range is the band where Bitcoin meaningfully influences long-term portfolio returns without dominating the experience of holding the portfolio.

Suitable scenarios

The balanced tier fits investors with multi-decade horizons and demonstrated discipline. Three components determine sustainability at this size:

- Time horizon — 10+ years provides room for the position to compound through multiple cycles, smoothing the entry-timing risk that affects shorter-horizon allocations

- Stable diversified income — provides the cash flow that prevents forced selling during drawdowns

- Existing diversification — across equities, bonds, real estate or other asset classes means the Bitcoin position is one component amongst several

- Demonstrated behavioural tolerance — holding through prior drawdowns without selling determines whether the investor can sustain the larger position

Implementation pattern

Balanced tier allocations split well between ETF and direct ownership depending on account structure.

The retirement-account portion typically lives in ETFs because direct Bitcoin in retirement accounts requires specialised infrastructure that often offsets the wrapper benefit. The taxable account portion can be split between ETF (operational simplicity, tax-loss harvesting eligibility for direct on the wash-sale-rule asymmetry) and direct ownership (no expense ratio, self-sovereignty, multi-decade compound efficiency).

Many balanced-tier investors run a 50/50 split between their retirement-account ETF holdings and their taxable-account direct ownership, capturing the benefits of both wrappers within a single allocation target.

Aggressive Tier (15-30%)

The aggressive tier is for investors with strong prior conviction, long horizons, stable wealth structures and demonstrated ability to hold through multiple prior drawdowns without selling.

Position sizes range from 15% (substantial conviction) to 30% (dominant component). Above 30%, Bitcoin starts to determine portfolio outcomes more than other components, which crosses into concentration territory rather than diversified investment.

The mathematical case

Concrete example: a 25% Bitcoin allocation in a $625,000 (£500,000) portfolio holds approximately $156,000 of Bitcoin. A 50% drawdown costs $78,000 — a 12.5% hit to total portfolio value.

Most retail investors find a 12.5% portfolio drawdown produces meaningful behavioural pressure regardless of prior conviction. Investors who can sustain the aggressive tier without selling typically share specific characteristics:

- Prior drawdown experience without selling

- Income stability that does not correlate with crypto markets

- Sufficient existing wealth that the absolute drawdown does not threaten financial security

- An explicit conviction thesis that survives the drawdown narrative

Suitable scenarios

The aggressive tier fits a narrow set of investor profiles.

Investors who got there gradually — through balanced-tier holdings that grew with the asset rather than through initial large lump-sum sizing — typically sustain the position better than investors who size aggressively at entry.

Investors with explicit conviction frameworks (specific thesis about Bitcoin's role over multi-decade horizons, willingness to hold through 70% drawdowns based on that thesis) sustain the position better than investors operating on momentum or social pressure.

Investors with diversified wealth outside the Bitcoin position (stable income, real estate, equity holdings, other liquid assets) can sustain the position because their financial security does not depend on the Bitcoin holding.

Implementation pattern

Aggressive tier allocations almost always include direct ownership for the larger portion of the position.

The cumulative expense-ratio drag of holding 25% of net worth in ETFs over multi-decade horizons becomes material. At 0.25% annually on a $156,000 position, the cost is $390/year initially, scaling with the position value. Over 20 years on a position that grows substantially, the cumulative ETF expense exceeds $25,000 even at modest growth rates, compared with negligible costs for properly-executed direct ownership.

The trade-off favours direct holdings beyond the threshold where operational setup is justified, which most aggressive-tier investors cross by definition.

Honest pre-commitment

Investors choosing the aggressive tier should be honest about prior performance. If you did not hold a Bitcoin position through the 2022 drawdown without selling, your behavioural calibration may not yet support a 25% allocation.

The most reliable predictor of behavioural tolerance is demonstrated behaviour through a prior cycle, not self-assessment. Investors lacking that track record are better served by starting at the balanced tier and scaling up gradually as the allocation grows with the asset, rather than starting at an aggressive sizing that they may not be able to sustain.

Rebalancing: Calendar vs Threshold

Without a rebalancing protocol, the allocation tier you chose at entry stops being your allocation tier within a single market cycle. Bitcoin's volatility produces drift faster than most other asset classes — a Bitcoin position can double in twelve months and double again in another twelve, taking a 10% allocation past 30% before the investor has thought about whether to act. By that point, the portfolio has different risk characteristics than the one the original sizing decision was meant to produce.

Rebalancing forces the allocation back to its target periodically, capturing volatility-driven value through cycles rather than letting the position grow into concentration. Two structured approaches dominate retail practice, with a hybrid emerging as the practical default.

The choice between calendar and threshold approaches affects after-tax returns, behavioural sustainability and operational complexity.

Calendar rebalancing

Calendar rebalancing checks allocation drift on a fixed schedule and rebalances if drift exceeds a threshold. Annual rebalancing aligned to tax-year boundaries (5 April in the UK, 31 December in most other jurisdictions) is the most common pattern.

Benefits:

- Fixed number of rebalancing events per year (typically zero to one)

- Simplified tax reporting because all disposals happen in a known window

- Clean integration with calendar-driven income flows and standard portfolio review processes

Quarterly rebalancing produces more frequent events and finer-grained drift control at the cost of more transaction friction and tax complexity. Annual is recommended for most retail investors.

Threshold rebalancing

Threshold rebalancing checks drift continuously and rebalances when the position moves more than 5 or 10 percentage points from target.

The mathematical case is that threshold rebalancing captures more value through volatility. By selling Bitcoin when it has rallied above target and buying when it has fallen below target, the strategy produces a small but consistent rebalancing premium over the long term.

The trade-off is that threshold rebalancing produces more frequent taxable events, more trading friction, and more operational complexity. For most retail investors, the after-tax return advantage of threshold over calendar rebalancing is small enough that the operational simplicity of calendar rebalancing dominates.

The hybrid approach

Many serious investors run a hybrid approach: calendar rebalancing as the default, with threshold-triggered partial rebalancing during extreme moves.

The default is annual rebalancing aligned to tax-year boundaries. If during the year the Bitcoin allocation drifts more than 50% above target (e.g., a 10% target growing to 15%+), a partial rebalancing trims back to a buffer above target rather than to the precise target. This captures most of the threshold-rebalancing benefit during exceptional moves while preserving the operational simplicity of calendar rebalancing during normal market conditions.

Tax considerations

Rebalancing produces tax consequences that vary by wrapper and jurisdiction.

Inside tax-advantaged wrappers (US IRA/401(k), UK ISA/SIPP, EU pension structures), rebalancing is tax-free and can happen without consideration of timing. In taxable accounts, rebalancing realises capital gains or losses, which interact with annual allowances, tax-loss harvesting strategies, and short-versus-long-term holding periods.

Specific jurisdictional notes:

- UK investors with positions outside ISA wrappers can use the £3,000 annual CGT allowance to rebalance up to that gain figure each tax year without tax cost

- US investors can use tax-loss harvesting on direct Bitcoin holdings (currently exempt from the wash-sale rule) to offset rebalancing gains

- EU investors face country-specific tax structures that affect optimal rebalancing timing materially

Bitcoin Inside a 60/40 Portfolio

The traditional 60/40 stock-bond portfolio remains the reference point for most retail allocation discussions despite the criticism it received during the 2022 bond drawdown. Adding a Bitcoin sleeve to a 60/40 portfolio is one of the most common questions amongst investors approaching the asset for the first time.

The answer depends on which side the sleeve draws from and how the resulting structure interacts with the original portfolio's risk-balancing logic.

Drawing from equities

The cleanest extension of 60/40 with Bitcoin draws the Bitcoin allocation from the equity side rather than from bonds. A 5% Bitcoin sleeve produces a 55/40/5 structure (equities/bonds/Bitcoin).

The logic is that Bitcoin and equities share more risk-on characteristics — both rise during macro liquidity expansion, both fall during liquidity contraction — than Bitcoin and bonds, which often move in opposite directions to equities during traditional risk-off periods. Drawing Bitcoin from the equity side preserves the bond allocation's defensive role during equity drawdowns.

Larger Bitcoin sleeves (10-15%) follow the same logic with proportionally larger reduction from equities.

Drawing from bonds

The alternative approach draws the Bitcoin sleeve from the bond side, producing structures like 60/35/5 or 60/30/10.

The case for this approach is that bonds in 2025-2026 deliver lower expected returns than historical averages because of the post-2022 rate environment, and that some of the "diversification" the bond allocation provides is duplicated by the Bitcoin sleeve in different drawdown scenarios.

The case against is that bonds remain genuinely uncorrelated with equities during certain types of drawdown (recessions, deflationary shocks) where Bitcoin tends to fall alongside equities. Most rigorous analysis supports drawing Bitcoin from equities rather than bonds for this reason.

Performance characteristics

A 60/40 portfolio extended with a 5% Bitcoin sleeve has historically produced higher returns and somewhat higher volatility than the underlying 60/40, with Sharpe ratio improvements that are modestly positive across most testing windows.

The improvement scales roughly linearly with the Bitcoin allocation up to about 15% before diminishing. Allocations above 15-20% start to produce volatility increases that exceed the return increases, indicating the sleeve has crossed from diversification into concentration territory. The 5-10% range is the historically most favourable risk-adjusted band for 60/40 extensions with Bitcoin.

Rebalancing in the extended portfolio

Rebalancing the Bitcoin sleeve back to target captures most of the diversification benefit. A 60/40/5 structure where the Bitcoin sleeve grows from 5% to 15% during a rally and is rebalanced back to 5% by trimming the gains produces materially better long-term returns than the same structure left to drift.

The trimmed gains return to the equity and bond allocations in their original 60/40 ratio, producing a self-reinforcing pattern where Bitcoin gains fund the rest of the portfolio's continued growth. This is the structural benefit of including Bitcoin as a small-to-medium sleeve in an otherwise traditional portfolio.

Geographic Wrapper Context

The wrapper structure dictates where the allocation lives, which affects after-tax returns more than most retail investors realise. The framework varies meaningfully by jurisdiction. None of this constitutes tax advice — verify with a qualified accountant for any meaningful position.

United States

US investors have multiple wrapper options that interact with Bitcoin allocation decisions:

- Standard taxable brokerage accounts — hold both spot Bitcoin ETFs and direct Bitcoin (via specialised platforms) with capital-gains treatment on disposal

- Standard IRAs (Traditional and Roth) — increasingly accept spot Bitcoin ETFs through major plan administrators including Fidelity, Schwab and Vanguard, providing tax-deferred or tax-free Bitcoin exposure

- 401(k) plans — vary by plan administrator; some now offer direct Bitcoin ETF access while others still require brokerage-link routing

- Self-directed IRAs — through specialised cryptocurrency custodians, allow direct Bitcoin holdings inside the wrapper, although the $200-500 annual fees often offset the wrapper benefit for positions under $50,000

The wrapper-aware allocation pattern for US investors typically follows three layers:

- Conservative-tier portion inside retirement-account ETFs

- Balanced-tier portion split between retirement ETFs and taxable direct holdings

- Aggressive-tier conviction holdings primarily in taxable direct ownership where the no-expense-ratio advantage compounds over multi-decade horizons

Tax-loss harvesting on direct Bitcoin (currently exempt from the wash-sale rule) is an additional benefit available only on the direct side.

United Kingdom

UK investors have the cleanest wrapper-driven allocation framework.

The £20,000 annual ISA allowance can hold ISA-eligible Bitcoin ETPs through brokers including Hargreaves Lansdown, IG, Trading 212 and AJ Bell, sheltering gains from CGT entirely up to the allowance. Multi-year ISA contributions can build a substantial Bitcoin position inside the wrapper over time. A £20,000 annual contribution over five years produces £100,000 of ISA-protected Bitcoin exposure plus any in-wrapper growth, all sheltered from CGT and dividend tax permanently.

SIPPs (self-invested personal pensions) can also hold Bitcoin ETPs in many cases, providing further tax-advantaged exposure with the higher SIPP contribution limits. Direct Bitcoin holdings outside any wrapper remain subject to the £3,000 annual CGT allowance and 18%/24% rates on gains above the allowance.

The wrapper-aware allocation pattern for UK investors typically prioritises:

- ISA wrapper capacity for the entire conservative-tier allocation and a meaningful portion of balanced-tier holdings

- SIPP wrapper capacity for additional tax-advantaged exposure in retirement-focused investing

- Direct Bitcoin self-custody for aggressive-tier conviction holdings beyond what the wrappers can absorb

European Union

EU treatment varies materially by member state under MiCA:

- Germany — one-year holding rule (gains tax-free after 12 months) favours direct Bitcoin holdings over ETF wrappers, because ETF disposals can trigger different tax treatment under securities rules even after the same period

- France — flat 30% rate on most crypto disposals makes the wrapper choice relatively neutral in pure tax terms, allowing investors to choose on operational grounds

- Portugal — 28% rate on disposals within one year, 0% beyond produces similar dynamics to Germany

- Netherlands — wealth-tax structure on Bitcoin ("box 3") changes the calculation entirely, with annual taxation regardless of realisation

Spain, Italy, Belgium, Sweden and other major EU jurisdictions each have distinct rules that affect optimal wrapper selection.

EU investors face the most country-specific decisions amongst the regions covered. The recommendation is to verify with a qualified local accountant before structuring any position above approximately €25,000, where the few hundred euros of consultation cost pays back many times over in optimal structure.

Common Allocation Mistakes (and How to Spot Them)

Most retail Bitcoin allocation mistakes cluster around five patterns. Recognising them in your own thinking is more useful than abstract framework knowledge — the mistakes are predictable enough that catching them in advance protects you from the worst outcomes.

Mistake 1: Sizing to upside conviction rather than downside tolerance

The most common allocation mistake is choosing position size based on how much you want Bitcoin to be worth in five years rather than how much you can absorb a 60% drawdown on. Investors who size for the upside find themselves overweight during drawdowns and consistently sell at the worst moments.

How do you spot this mistake in your own thinking? Ask yourself: if Bitcoin dropped 60% tomorrow, would you continue your DCA programme without anxiety? If the answer is no, your allocation is sized to upside conviction rather than downside tolerance, and you should reduce it before the drawdown arrives rather than after. The behavioural cost of selling at the bottom is consistently higher than the opportunity cost of starting smaller.

Mistake 2: Assuming behavioural tolerance you have not demonstrated

Closely related: investors who have never held Bitcoin through a major drawdown consistently overestimate their behavioural tolerance. The 25-year-old confident in his ability to hold through 80% drawdowns has not yet experienced one. The 45-year-old who held through the 2018-2019 cycle has actual data on her behavioural tolerance and can calibrate accordingly.

If you fall in the first category, treat your behavioural tolerance estimate as theoretical until proven otherwise. Start at the conservative tier even if you feel ready for aggressive. The cost of starting too small is small (you can scale up after demonstrating discipline). The cost of starting too large and panic-selling at the bottom is large and difficult to recover from.

Mistake 3: Confusing portfolio drawdown with Bitcoin drawdown

A 60% Bitcoin drawdown does not produce a 60% portfolio drawdown unless your entire portfolio is Bitcoin. With a 10% Bitcoin allocation, the same 60% Bitcoin drawdown produces approximately 6% portfolio drawdown — meaningful but absorbable. Investors who track Bitcoin's price and feel its drawdowns as if they were portfolio drawdowns have miscalibrated their risk perception.

The remedy is operational. Track portfolio-level performance, not Bitcoin-level performance. Check your overall net worth quarterly, not Bitcoin's daily price. Most retail investors who panic-sell during Bitcoin drawdowns would not have done so if they had been tracking the portfolio-level impact rather than the asset-level price.

Mistake 4: Ignoring tax wrapper opportunity

The wrapper choice — ETF inside retirement accounts versus direct Bitcoin in taxable accounts — produces 20-30% after-tax return differences over multi-decade horizons in most jurisdictions. Investors who default to one wrapper without considering the alternative leave significant value on the table.

The fix is straightforward but requires upfront work. Before sizing the position, map your available account types and their tax treatment. Identify which portion of your target allocation can fit in tax-advantaged wrappers and which cannot. Place the wrapper-eligible portion in ETF form inside the wrapper; place the remainder in direct Bitcoin in taxable accounts. This is the highest-leverage allocation decision after sizing itself.

Mistake 5: Setting allocation and never reviewing it

Your circumstances change. Income changes, time horizon changes, family situation changes, behavioural tolerance evolves through cycles. The 15% allocation that suited you at age 35 with strong income and a 30-year horizon probably does not suit you at age 60 with fixed-income lifestyle and a 10-year horizon.

Review your allocation annually. Ask whether your current size still matches your current life situation. Most allocation drift problems are not market-driven — they are life-driven, and the investor has not adjusted. Setting a calendar reminder for annual allocation review costs nothing and catches the problems that would otherwise compound for years.

Mistake 6: Treating allocation as a single decision rather than a system

Allocation is not one decision. It is a system of decisions: target tier, wrapper choice, custody mechanism, rebalancing protocol, drawdown response plan. Investors who frame allocation as "how much Bitcoin should I own" miss the operational structure that determines whether the answer holds up through cycles.

The system framing produces better outcomes because each component supports the others. Your tier choice determines your wrapper allocation. Your wrapper allocation determines your custody mechanism. Your custody mechanism determines your rebalancing operational complexity. Skip any component and the others become unstable. A 15% target tier with no rebalancing protocol becomes a 30% drift position within one strong cycle. A 15% allocation in the wrong wrapper produces 20-30% lower after-tax returns over decades. The components are not optional add-ons — they are integral to the framework working at all.

If you have made the sizing decision but skipped any other component, treat the framework as incomplete rather than complete-with-minor-gaps. Each missing component is a failure mode waiting to manifest. Set aside an evening to fill in the gaps before the next drawdown tests them.

Mistake 7: Anchoring on initial cost basis rather than current portfolio reality

Investors anchored on initial cost basis frequently misjudge their current allocation. Bitcoin appreciation distorts allocation perception substantially through cycles. Investors believing they hold "10% Bitcoin" sometimes actually hold 25-30% allocation after appreciation pushed concentration beyond initial targets. Conversely, drawdowns mechanically reduce allocation percentage relative to other assets, sometimes triggering unwarranted concern when overall portfolio still maintains balanced exposure relative to original allocation framework.

The defensible approach treats current allocation percentage rather than purchase-time allocation percentage as primary reference. Recalculate allocation quarterly using current market values across complete portfolio. Current allocation guides current decisions; historical allocation simply provides context about accumulated performance.

Conclusion

Bitcoin allocation sizing is the most controllable input to long-term Bitcoin investment outcomes. The volatility-budget framework gives a defensible answer for most retail scenarios:

- Identify your maximum sustainable portfolio drawdown

- Allocate it across asset classes weighted by their drawdown contribution

- Place the Bitcoin portion at the size that fits your time horizon, income stability and demonstrated behavioural tolerance

The three tiers — conservative, balanced, aggressive — map cleanly to typical investor profiles, and rebalancing mechanics ensure the allocation captures volatility-driven value through full cycles rather than drifting passively.

What to do this week

If you are starting from scratch on Bitcoin allocation, the framework converts into four concrete actions:

- Calculate your volatility budget. Take total investable wealth excluding primary residence. Multiply by the maximum portfolio drawdown you can sustain without behavioural change (typically 20-30% for most retail investors). The result anchors all subsequent sizing decisions.

- Choose your starting tier honestly. If you have not held Bitcoin through a prior 50%+ drawdown without selling, start at the conservative tier. Behavioural tolerance is empirical, not theoretical. Investors who self-assess as aggressive but lack track record consistently overestimate.

- Map your wrapper allocation. Identify which portion of your target allocation lives in tax-advantaged retirement accounts (US IRA/401(k), UK ISA/SIPP) versus taxable accounts. The wrapper structure usually determines whether each portion should be ETF or direct Bitcoin.

- Define your rebalancing protocol. Annual calendar rebalancing is the practical default. Document the threshold at which you will rebalance (e.g., "trim Bitcoin if the position drifts more than 50% above target"). Without a written protocol, drift accumulates and the allocation becomes meaningless.

The allocation decisions you make at entry determine the framework. The rebalancing decisions you make over time determine whether the framework holds. Both matter. The sequence is structural-decision first, then operational-discipline through cycles.

The execution detail for accumulating into the chosen target sits in our DCA playbook. The wrapper-by-wrapper decision between ETF and direct Bitcoin sits in our ETF vs direct framework. The broader portfolio strategy beyond Bitcoin specifically is covered in our crypto portfolio strategies guide.

Sources

- Federal Reserve — macro-policy context affecting Bitcoin volatility and allocation decisions

- HM Revenue and Customs — UK CGT framework, ISA allowance rules, SIPP regulations

- Internal Revenue Service — US Bitcoin tax treatment and IRA-eligibility framework

- EUR-Lex — EU MiCA framework affecting cryptocurrency taxation across member states

- Bogleheads — long-running portfolio-allocation research community covering 60/40 and alternatives sleeves

- Bitcoin Investment Fundamentals: Post-Cycle Strategy Guide

- Spot Bitcoin ETF vs Direct BTC

- Bitcoin DCA Strategy Playbook

- Bitcoin vs Gold Comparison

- Crypto Portfolio Strategies

- Crypto Risk Management

- Crypto vs Stocks: Asset-Class Comparison

Frequently Asked Questions

- What is a volatility budget for Bitcoin allocation?

- A volatility budget is the maximum portfolio drawdown you can sustain without changing your behaviour or financial plan. For Bitcoin, the working assumption is that a 50-70% peak-to-trough drawdown is plausible from any entry point. If your Bitcoin allocation multiplied by 50% would force you to sell other assets at a bad time, harm retirement timing, or trigger emotional decisions, the allocation is too large for your volatility budget. The right allocation is the largest size that keeps the worst-case drawdown within tolerable bounds.

- Should I rebalance my Bitcoin position calendar-based or threshold-based?

- Calendar rebalancing checks allocation drift on a fixed schedule (typically annually) and rebalances if drift exceeds a threshold. Threshold rebalancing checks drift continuously and rebalances when the position moves more than 5 or 10 percentage points from target. Threshold rebalancing tends to capture slightly more value through volatility but produces more frequent taxable events. For most retail investors, annual calendar rebalancing aligned to tax-year boundaries produces the best after-tax result.

- Can I hold Bitcoin in a 401(k) or IRA?

- Spot Bitcoin ETFs are increasingly available inside US 401(k) plans and standard brokerage IRAs through major plan administrators. Direct Bitcoin requires a self-directed IRA with a specialised cryptocurrency custodian, which adds annual fees of $200-500 that often offset the wrapper benefit for smaller positions. For most US retirement-account Bitcoin allocations, holding a spot ETF (IBIT, FBTC or similar) inside a standard brokerage IRA is the simpler path that captures the tax-deferral or tax-free benefit.

- How does Bitcoin fit into a 60/40 portfolio?

- A traditional 60/40 stock-bond portfolio extended with a Bitcoin sleeve typically draws the Bitcoin allocation from the equity side rather than from bonds, because Bitcoin and equities share more risk-on characteristics. A 60/40 portfolio with a 5% Bitcoin sleeve becomes 55/40/5. The sleeve adds asymmetric upside while the bond allocation continues to provide downside protection. Investors with longer horizons and higher risk tolerance scale the sleeve to 10-15% by reducing the equity allocation accordingly.

- What is the right Bitcoin allocation for my age?

- Age affects Bitcoin allocation primarily through time horizon and human-capital remaining. Investors with 20-30 year horizons can absorb deeper drawdowns and benefit more from compounding, which supports balanced or aggressive tier allocations. Investors within 5-10 years of retirement face sequence-of-returns risk that disfavours large drawdowns, which supports conservative tier allocations. The transition typically happens gradually over the decade before retirement rather than abruptly at any single age.