Bitcoin vs Gold: Digital Stores of Value Compared

A comparison of Bitcoin and gold across returns, volatility, custody, liquidity, tax treatment and portfolio role — with practical allocation guidance for investors deciding between them or holding both.

Introduction

Bitcoin's "digital gold" framing has become one of the most-cited and most-disputed analogies in modern macro investing.

Proponents argue Bitcoin replicates gold's store-of-value properties in a more efficient digital form. Critics argue gold's 5,000-year track record cannot be replicated by an asset with 17 years of trading history. Both positions have merit. The interesting question for serious investors is not whether Bitcoin is digital gold in the abstract, but how the two assets compare across the dimensions that actually matter for portfolio construction.

The two assets share a structural role in many portfolios: they sit outside the equity-bond-cash framework as alternative store-of-value holdings that respond to different economic conditions than traditional risk assets. They differ substantially in nearly every other respect — track record, volatility profile, custody mechanism, divisibility, transferability, and the specific scenarios under which each performs best.

Both have real cases as portfolio components. Gold's case rests on demonstrated behaviour across multiple crisis types over decades, gentler volatility that fits constrained time horizons, and structural defensive properties during specific economic shocks. Bitcoin's case rests on hard-capped supply, modern divisibility, on-chain auditability, and asymmetric upside as adoption deepens. Neither case is fully settled — gold's role has evolved through history and Bitcoin's role is still emerging — but the comparison framework allows investors to make defensible decisions despite that uncertainty.

This comparison covers what retail investors typically need to evaluate:

- Long-run returns and volatility

- Custody options and costs

- Liquidity profiles

- Tax treatment by region

- The portfolio role each asset plays

The framing matters. A comparison that finds gold more reliable than Bitcoin and Bitcoin higher-returning than gold is consistent with both being held in the same portfolio rather than chosen between. Most serious investors arrive at a hybrid allocation rather than an either-or choice. The relevant question becomes how to weight the two — which depends on time horizon, behavioural tolerance and conviction about which scenarios are most likely over the holding period.

If you arrived from our Bitcoin investment fundamentals hub, this comparison fits inside the broader allocation framework introduced there. The macro-aware reader looking at Bitcoin's role in a diversified portfolio benefits from understanding how it compares with the closest established analogue rather than from evaluating Bitcoin in isolation. The conclusions of this analysis carry weight even for investors who never plan to hold gold directly, because the comparison frames Bitcoin's properties relative to a familiar benchmark rather than as abstractions on their own.

Side-by-Side Comparison

The numerical comparison below covers the dimensions most relevant for portfolio decisions. Specific figures should be treated as approximate ranges that update with market data; the comparative relationships between the two assets are stable across reasonable update windows.

Quantitative comparison at a glance

| Dimension | Bitcoin | Gold |

|---|---|---|

| Total market capitalisation | ~$1.3 trillion (mid-2026) | ~$28-30 trillion (mid-2026) |

| Annual supply growth | ~0.85%, decreasing through halvings; capped at 21 million | ~1.5-2%, ongoing |

| Supply certainty | Code-enforced, mathematically fixed | Depends on mining economics and discovery |

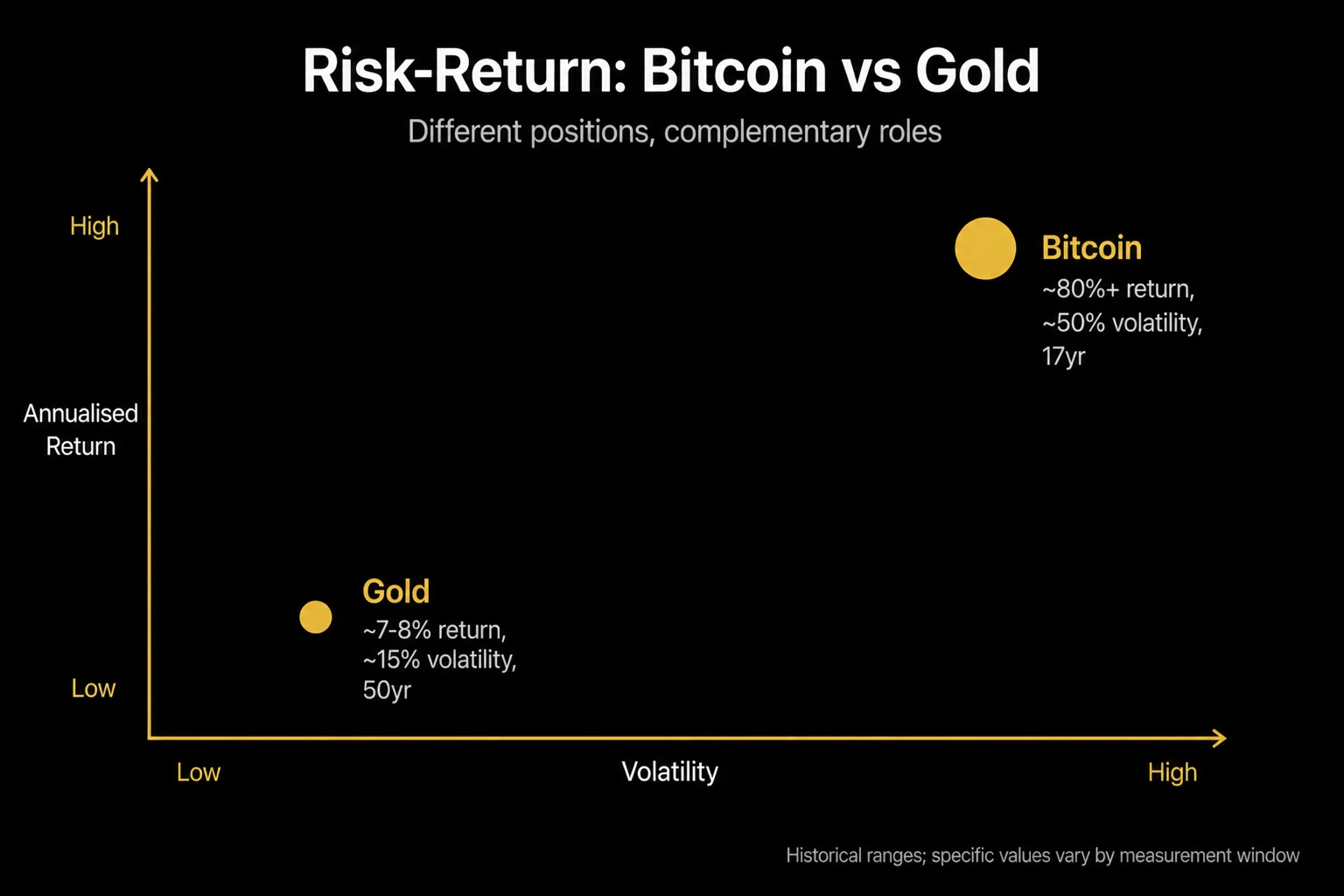

| Long-run annualised return (historical) | Substantially higher than gold; window-dependent | ~7-8% over 50 years |

| Annualised volatility | ~40-60% (post-ETF era), historically 60-80% | ~15-20% |

| Worst peak-to-trough drawdown | 70-85% across multiple cycles | 40-50% over multi-decade horizons |

| Storage cost (custody) | Near-zero for self-custody (one-time hardware ~$200); 0.20-0.25% for ETF | 0.5-1% for vault storage; 0.15-0.4% for ETF |

| Minimum practical retail unit | 0.00000001 BTC (1 satoshi) | 1 ounce (~$4,200 per troy oz, mid-2026) |

| Authenticity verification | Cryptographic, on-chain, anyone with a node | Physical testing or third-party certification |

| Cross-border mobility | Digital, no physical constraint | Customs declarations, physical transport |

| Track record | 17 years | ~5,000 years monetary history |

Notes on the supply schedules

Bitcoin's supply schedule is enforced by code and cannot be changed without near-unanimous network consensus. Gold's supply growth depends on mining technology, economic incentives and discoverable reserves, all of which can shift over time. The 1.5-2% gold supply growth is itself a long-run estimate; new mine discoveries or extraction technology improvements can move the figure within the range.

Bitcoin's 0.85% annual issuance figure decreases at each halving roughly every four years. By the early 2030s, Bitcoin's supply growth will have dropped below 0.5% annually, and by 2040 below 0.2%. Gold's supply growth is structurally constant in approximate terms because it is bounded by physical extraction economics rather than by a programmed schedule.

Notes on volatility and drawdowns

Bitcoin's volatility has compressed somewhat in the post-ETF era as institutional holders smooth the order book. The historical 60-80% annualised volatility produced the multi-cycle 70-85% drawdowns that defined Bitcoin's earlier reputation. Recent cycles have produced shallower drawdowns (40-50%) with longer durations, more aligned with traditional risk asset behaviour. Whether this volatility compression persists depends on continued institutional adoption.

Gold's volatility tends to expand during financial system stress and contract during stable periods. The asset's defensive characteristics show up most clearly in scenarios involving currency debasement, geopolitical shock or banking crisis, where gold typically rises while traditional risk assets fall. Bitcoin's behaviour in such scenarios is less established — Bitcoin has shown defensive properties in some crises (banking sector stress) and risk-on properties in others (general liquidity tightening).

Custody and operational characteristics

- Divisibility — Gold is physically divisible to coin and bar levels but not below. Practical retail trade size is typically 1 ounce minimum. Bitcoin is divisible to eight decimal places, enabling transactions of any size.

- Verifiability — Gold authenticity requires physical testing or third-party certification. Bitcoin authenticity is mathematically verifiable on the blockchain by anyone running a node.

- Cross-border mobility — Gold movement across borders involves customs declarations and physical transport. Bitcoin moves across borders with no physical constraint, though regulatory reporting may apply at large amounts.

Bitcoin's Case as Digital Gold

The case for Bitcoin as a modern store of value rests on properties that gold has but in more efficient or more verifiable forms. Bitcoin's proponents do not claim Bitcoin replaces gold. They claim Bitcoin extends the store-of-value category into the digital era while preserving the properties that made gold useful as a monetary asset for thousands of years.

Hard-capped supply

Bitcoin's 21 million supply cap is the strongest single argument for the digital-gold framing.

Gold's supply expands gradually over time as new deposits are mined. Bitcoin's supply is mathematically fixed and cannot be expanded regardless of demand. The supply certainty is enforced by code and protected by network consensus rules that have proven resilient across 17 years of operation, multiple controversial protocol changes and several attempts at hostile forks. For investors concerned about monetary debasement (currency printing, inflation, dilution of fixed-income claims), Bitcoin's supply schedule is more credibly fixed than gold's.

Modern divisibility and transferability

Bitcoin's eight-decimal divisibility means transactions of any size are possible without physical constraints. A retail investor can buy $5 of Bitcoin or $5 million of Bitcoin using the same protocol. Gold's practical retail unit is the 1-ounce coin, which sits well above most retail transaction sizes.

Bitcoin's transferability is similarly modern. Settling a $10 million Bitcoin transaction takes the same operations as settling a $10 transaction. Settling a $10 million gold transaction involves substantial physical logistics, customs reporting and counterparty management.

Programmable and auditable

Bitcoin's blockchain provides a public audit trail of all transactions and balances. Anyone running a node can:

- Verify the total Bitcoin supply

- Check that any specific address holds what it claims to hold

- Trace the history of any specific Bitcoin from issuance to current ownership

This auditability is materially stronger than gold's, where audit depends on trusted third parties (vault auditors, certification bodies) rather than on cryptographic proof. For investors concerned about supply fraud or double-counting in custody, Bitcoin's auditability is structurally superior to gold's.

The asymmetric upside

Bitcoin's market capitalisation sits at around 5% of gold's as of mid-2026. If Bitcoin captures even a fraction of gold's role as an institutional and retail store of value over the coming decades, the price implication is substantial.

The argument is not that Bitcoin replaces gold entirely. It is that the relative market caps could compress as Bitcoin's adoption matures, producing meaningful Bitcoin outperformance against gold even in scenarios where both assets perform reasonably. This thesis underlies most institutional Bitcoin allocation arguments and is the reason why some investors weight Bitcoin more heavily than gold despite gold's longer track record.

Gold's Case as Established Hedge

Gold's case rests on properties Bitcoin cannot yet match: a 5,000-year monetary history, demonstrated behaviour across multiple crisis types, and structural characteristics that have produced consistent returns across multiple generations of investors.

The case is not that gold outperforms Bitcoin in every scenario. The case is that gold's reliability has been earned over centuries while Bitcoin's reliability is being earned in real time.

Five thousand years of monetary history

Gold has functioned as a monetary asset across multiple civilisations, multiple political systems and multiple economic regimes. Roman, Byzantine, Spanish, British and US monetary systems all included gold at different stages.

Gold survived the collapse of Bretton Woods in 1971 and re-emerged as a recognised monetary asset within a decade. The track record is not that gold always rises. It is that gold consistently retains some monetary recognition across regime changes that destroy other asset classes. No other asset has comparable history.

Demonstrated crisis behaviour

Gold has produced strong returns during specific crisis types that have repeated multiple times in modern history:

- 1970s inflation period — gold appreciated significantly while equities and bonds suffered

- 2008 financial crisis — gold rallied while equities fell, providing portfolio diversification

- 2020 COVID shock — gold rose alongside risk assets but with different timing and magnitude

- 2022 inflation surge — gold preserved purchasing power while bonds suffered material losses

Bitcoin's crisis-period behaviour is less clear. Bitcoin's first major crisis test was 2022, where it fell alongside equities and bonds rather than acting as a hedge. The 2008-style flight-to-safety behaviour that gold demonstrates has not yet been demonstrated by Bitcoin in a comparable test.

Lower volatility, smaller drawdowns

Gold's volatility profile is materially gentler than Bitcoin's.

The worst peak-to-trough gold drawdowns over the past 50 years have been 40-50%, occurring over multi-year periods. Bitcoin's drawdowns have routinely reached 70-85% within single cycles. For investors who cannot sustain deep drawdowns behaviourally — those near retirement, those with concentrated wealth, those with cyclical income — gold's volatility profile fits portfolio risk budgets that Bitcoin's does not. This is the structural reason gold remains in pension and endowment portfolios where Bitcoin is not yet considered appropriate.

Institutional acceptance

Gold is held by virtually every central bank as a foreign-exchange reserve, accepted as collateral by most major financial institutions, and integrated into the global financial system through deeply liquid markets, established custody infrastructure and standardised contracts.

Bitcoin's institutional acceptance has grown substantially since 2024 but remains earlier in adoption. The depth of institutional support for gold creates resilience that Bitcoin will need years to match — not because Bitcoin is structurally inferior, but because institutional adoption takes time to deepen.

Portfolio Role: Together or Either-Or?

The most common framing in retail commentary treats Bitcoin and gold as substitutes — investors choose one or the other based on conviction in the underlying thesis.

The framing is usually wrong. Bitcoin and gold can play complementary roles in a diversified portfolio precisely because their risk profiles, return characteristics and crisis behaviours differ.

The hybrid case

A portfolio that holds both Bitcoin and gold captures different scenario coverage than either alone:

- Gold provides downside protection during specific crisis types (deflationary shocks, banking crises, currency stability events) that Bitcoin has not yet demonstrated equivalent behaviour for

- Bitcoin provides upside exposure to scenarios (digital adoption, alternatives to fiat, sovereign accumulation, ETF flow growth) that gold cannot capture in the same magnitude

- Both together hedge against the uncertainty of which scenario type will dominate over the holding period — a relevant consideration when neither investor nor analyst can predict which crisis type will materialise next

Holding 5% gold and 5% Bitcoin in a 60/40 portfolio produces different risk-adjusted return characteristics than holding 10% of either alone, with the diversification capturing both downside coverage and upside asymmetry.

The substitute case

For some investors, Bitcoin and gold serve the same portfolio role and choosing between them makes sense.

Investors with strict allocation constraints (only one alternatives sleeve, no room for both) face a real choice. Investors with strong conviction in one thesis (gold is the only proven monetary asset; Bitcoin is the future of money) often weight one heavily and exclude the other. These positions are defensible for specific investor profiles, but the substitute framing is not universally correct.

How professionals tend to allocate

Allocation professionals who have written publicly on the question — including Ray Dalio, Paul Tudor Jones and several major endowment CIOs — have tended towards hybrid allocations rather than either-or choices.

The hybrid pattern typically holds gold as a larger, more defensive position (5-10% of portfolio) and Bitcoin as a smaller, more growth-oriented position (1-5% of portfolio), with the relative weights adjusted to investor conviction and time horizon. This pattern is not universal but is the dominant approach amongst investors with experience in both assets.

The correlation question

Bitcoin and gold have shown low correlation across most measurement windows, which is the structural property that supports the hybrid allocation.

The relationship varies by regime:

- Risk-on periods — Bitcoin tends to outperform while gold drifts

- Risk-off periods — sometimes both fall together (2022); sometimes gold rises while Bitcoin falls (specific banking-crisis episodes); sometimes Bitcoin holds while gold drifts (specific dollar-strength periods)

- Liquidity crises — both assets can be sold under pressure when investors need cash regardless of long-term thesis. The 2020 March crash saw Bitcoin and gold both fall sharply during the same week as equities, then both recover. Liquidity-driven selling does not respect store-of-value framing.

The variability of the relationship is itself a diversification benefit. The two assets are not consistently substitutes or consistently complements, which means a portfolio holding both gets coverage that neither alone provides.

Tax Treatment by Region

Tax treatment differs more between Bitcoin and gold than most investors realise, with implications that often outweigh small differences in expected returns. The framework varies by jurisdiction. None of this constitutes tax advice — verify with a qualified tax advisor for any meaningful position.

United States

US tax treatment favours Bitcoin over gold for most retail investors on after-tax basis.

Gold is classified as a "collectible" by the IRS, which means long-term capital gains on physical gold and most gold ETFs are taxed at a maximum rate of 28% federal — materially higher than the 0%, 15% or 20% long-term rates that apply to Bitcoin and other property assets. Bitcoin's tax treatment as property produces lower long-term gains rates for most income bands, which translates to a multi-percentage-point after-tax return advantage over gold for taxable holdings.

Self-directed IRAs can hold both gold and Bitcoin tax-deferred or tax-free, eliminating the differential inside retirement wrappers. The wash-sale rule asymmetry (Bitcoin currently exempt; gold subject) creates additional tax-management flexibility for direct Bitcoin holdings.

United Kingdom

UK tax treatment is roughly symmetric between Bitcoin and gold for most retail investors.

Both are subject to capital gains tax on disposal with the £3,000 annual allowance and 18% (basic rate) or 24% (higher and additional rates) rates. Investment-grade gold (sovereign coins like Britannias and Sovereigns minted by the Royal Mint) is exempt from CGT entirely as legal tender, which is a meaningful UK-specific tax advantage gold has over Bitcoin.

UK ISA wrappers can hold both gold ETFs (subject to ISA-eligible product availability) and Bitcoin ETPs, sheltering gains entirely up to the annual £20,000 allowance. SIPP wrappers similarly accept both for tax-advantaged retirement holdings.

European Union

EU treatment varies materially by member state:

- Germany — Bitcoin held over 12 months is tax-free on disposal; treatment more favourable than gold which is subject to standard capital gains rules

- France — flat 30% rate on crypto disposals applies regardless of holding period; gold is subject to a different tax structure (typically 11.5% on disposal value, with optional capital-gains election)

- UK-style investment-grade gold CGT exemption — does not have direct equivalents in most EU jurisdictions, but several countries have specific provisions for gold that differ from crypto treatment

Verification with local tax advice is essential for any meaningful position.

Practical implications

The tax differential matters more for taxable holdings than for retirement-account holdings.

- US investors with taxable allocations to both assets typically find Bitcoin produces materially higher after-tax returns even at equivalent pre-tax returns

- UK investors with British gold sovereigns achieve a CGT-free exposure that crypto investments cannot match

- EU investors face country-specific dynamics that often favour one asset over the other depending on holding period and disposal patterns

The tax differential should inform allocation decisions but rarely changes the fundamental hybrid recommendation. Both assets can be held with structures that minimise the tax friction in each jurisdiction.

Practical Allocation Considerations

Translating the comparison into a concrete portfolio decision requires thinking through investor-specific factors that the abstract comparison cannot resolve. The framework below covers the practical considerations that usually drive allocation decisions in real portfolios.

Time horizon

Time horizon is the single most important input to the Bitcoin-vs-gold (or Bitcoin-and-gold) decision.

- 20+ year horizons — investors can absorb Bitcoin's deeper drawdowns and benefit more from its asymmetric upside, which favours larger Bitcoin allocations relative to gold

- 5-10 year horizons — sequence-of-returns risk disfavours Bitcoin's volatility profile, which favours larger gold allocations or smaller hybrid sleeves with conservative sizing on the Bitcoin side

- Under 5-year horizons — Bitcoin's cycle dynamics can produce extended periods of underperformance that the investor lacks time to recover from. Gold's gentler volatility and shorter recovery cycles make it the better fit when the planning horizon is constrained by approaching liabilities (retirement, large planned purchase, business exit).

The time-horizon framing is more important than thesis conviction. Even an investor strongly convinced of Bitcoin's long-term thesis should size conservatively if their horizon is too short to absorb the volatility.

Existing wealth concentration

Investors with concentrated single-stock or single-property wealth already carry substantial idiosyncratic risk. Adding a large Bitcoin position to such a portfolio compounds the existing concentration rather than diversifying.

Adding gold provides genuine diversification because gold's correlation with most concentrated wealth positions is low. For investors with concentrated wealth, gold often plays a larger role than Bitcoin in the alternatives sleeve regardless of pre-tax return expectations.

Income stability

Income stability affects which volatility profile fits the portfolio.

Investors with stable, diversified, non-cyclical income can absorb Bitcoin's drawdowns without forced selling. Investors with cyclical or fragile income face the worst-case scenario where Bitcoin drawdowns coincide with income shocks, producing forced selling at the worst time. For investors with fragile income, gold's gentler volatility makes it the better fit for the alternatives sleeve regardless of long-run return potential.

Behavioural calibration

Demonstrated behavioural tolerance through prior drawdowns is the third major input.

Investors who have held positions through 50%+ drawdowns without selling have demonstrated the discipline that supports larger Bitcoin allocations. Investors who have not yet been tested should size conservatively until they have. Gold's gentler drawdowns rarely test behavioural calibration to the same degree, which means new investors can typically hold gold positions without the test that Bitcoin requires.

The starting recommendation

For most retail investors with multi-decade horizons and moderate risk tolerance, a starting allocation of 5-10% gold and 2-5% Bitcoin produces a defensible hybrid sleeve inside a 60/40 portfolio.

The structure works because:

- The gold allocation provides downside coverage

- The Bitcoin allocation provides upside asymmetry

- The combined sleeve is small enough to be sustainable through drawdowns while large enough to influence long-term returns

Investors with stronger conviction in one or the other adjust the relative weights, but the hybrid baseline is the most-defensible starting point given the genuine differences between the two assets.

The detailed allocation framework — including the volatility-budget logic, the three-tier sizing approach, and the rebalancing mechanics — sits in our portfolio allocation guide.

Conclusion

The Bitcoin-versus-gold question is rarely a clean either-or choice for serious investors.

Both assets serve store-of-value roles, both have delivered meaningful long-run returns, both provide diversification against specific portfolio risks, and both have characteristics the other lacks:

- Gold offers a 5,000-year track record, gentler volatility and demonstrated crisis behaviour

- Bitcoin offers hard-capped supply, modern divisibility, structural auditability and asymmetric upside as adoption deepens

- Together they cover scenarios that either alone would miss — gold's crisis-tested defensive properties paired with Bitcoin's growth-asset characteristics in scenarios where digital monetary alternatives matter

The defensible position for most investors is hybrid allocation rather than substitution.

The exact ratio between the two depends on time horizon, wealth structure, income stability, behavioural calibration and tax-jurisdiction context. A 5-10% gold and 2-5% Bitcoin combined sleeve in a 60/40 portfolio produces a reasonable starting point. Conviction-based deviations from that baseline are defensible if grounded in the investor's specific situation rather than in price-prediction confidence.

The detailed sizing framework lives in our allocation satellite. The broader Bitcoin investment context lives in our investment fundamentals hub.

Sources

- Federal Reserve — macroeconomic context for monetary debasement and store-of-value comparisons

- Internal Revenue Service — US tax treatment of gold collectibles and Bitcoin property

- HM Revenue and Customs — UK CGT framework, investment-grade gold exemption, ISA rules

- EUR-Lex — EU MiCA framework affecting cryptocurrency taxation across member states

- Bitcoin Investment Fundamentals: Post-Cycle Strategy Guide

- Bitcoin Portfolio Allocation

- Bitcoin Cycle 2026: Post-Halving Reality

- Spot Bitcoin ETF vs Direct BTC

- Bitcoin vs Ethereum Comparison

- Bitcoin Review: Investment Analysis

- Crypto vs Stocks: Asset-Class Comparison

Frequently Asked Questions

- Is Bitcoin really digital gold?

- Bitcoin shares some store-of-value properties with gold — fixed supply, divisibility, verifiability, portability — but differs materially in others. Bitcoin is more divisible and easier to transfer than gold, but more volatile and shorter-track-record. Gold has 5,000 years of monetary history; Bitcoin has 17. The "digital gold" framing is useful as a directional analogy but not a precise equivalence. Many serious investors hold both, treating them as related but distinct macro assets rather than substitutes.

- Has Bitcoin outperformed gold over the long term?

- Yes, by a substantial margin. Bitcoin's annualised returns since inception have far exceeded gold's, although Bitcoin's volatility and drawdowns have also been substantially larger. Over rolling 5-year and 10-year windows, Bitcoin has outperformed gold in most periods but the magnitude of outperformance varies widely with the start and end dates. The asymmetry is structural: Bitcoin offers higher upside with higher downside, gold offers steadier returns with lower drawdowns.

- Should I hold Bitcoin or gold or both?

- Many serious investors hold both as part of a diversified store-of-value sleeve. Gold provides a 5,000-year track record, low volatility relative to Bitcoin, and proven behaviour during specific crisis types (1970s inflation, 2008 financial crisis). Bitcoin provides higher upside, modern divisibility, and exposure to a different set of macro scenarios (digital adoption, alternatives to fiat, sovereign accumulation). The answer is rarely either-or. Allocation between them depends on time horizon, risk tolerance and conviction in each thesis.

- How does gold custody compare to Bitcoin custody?

- Physical gold custody requires a bank vault, a private vault service, or home storage with appropriate security. Vault costs typically run 0.5-1% per year; home storage avoids the cost but introduces theft and loss risk. Gold ETFs and allocated gold accounts provide simpler custody at the cost of counterparty exposure. Bitcoin custody ranges from exchange custody (counterparty risk) to hardware wallets (operational responsibility, no recurring cost) to multi-sig setups (highest security, highest complexity). Bitcoin custody is generally cheaper than physical gold but requires different operational discipline.

- Which is taxed more favourably: Bitcoin or gold?

- Treatment varies by jurisdiction. In the US, gold is taxed as a collectible at a higher long-term capital gains rate (28%) than most other capital assets, while Bitcoin is taxed as property at 0-20% federal long-term rates depending on income — making Bitcoin more favourable than gold for most US investors on after-tax basis. In the UK, both are subject to standard capital gains tax with the £3,000 annual allowance and 18%/24% rates. EU treatment varies by country, with some jurisdictions favouring long-held Bitcoin (Germany's tax-free after one year) and others taxing both similarly.