DCA Crypto Strategy Setup Guide for 2026

How to build and automate a Dollar-Cost Averaging plan for Bitcoin and Ethereum — with step-by-step Binance and OKX setup, real backtesting data, and the mistakes that cost beginners money.

Introduction

Dollar-Cost Averaging is the simplest investment strategy in crypto — and historically one of the most effective for beginners. You invest a fixed pound amount into Bitcoin, Ethereum, or another cryptocurrency at regular intervals (weekly, bi-weekly, or monthly) regardless of what the price is doing. When the price drops, your fixed amount buys more units. When the price rises, your fixed amount buys fewer units. Over time, your average cost per unit lands somewhere between the highs and the lows — consistently lower than the average market price during the same period.

Why does this matter for you as a beginner? Because the alternative — trying to time the blockchain-based cryptocurrency market by buying low and selling high — fails for the vast majority of retail investors. Research from Glassnode shows that fewer than 5% of retail traders consistently outperform a simple DCA strategy over any 3-year period. The reason is psychological: when the price crashes 40%, fear stops you from buying at the exact moment your money would have the most impact. When the price pumps 60%, greed pushes you to buy at the worst possible entry point. DCA removes both emotions from the equation by automating your purchases on a fixed schedule.

This guide shows you exactly how to set up a DCA strategy from scratch. You will learn how to choose your assets, decide on your investment amount and frequency, set up automatic purchases on Binance and OKX, avoid the five most common mistakes that cost beginners money, and understand when it makes sense to adjust your plan. Every example uses real GBP amounts and UK-specific tax guidance so you can implement your plan today. If you are completely new to exchanges, start with our first 30 days on a crypto exchange guide, then return here to automate your purchases.

The approach works across all market conditions. During the 2022 bear market, investors who maintained their weekly DCA into Bitcoin at £20,000-30,000 accumulated significantly more BTC than those who only bought during the 2021 euphoria at £40,000-50,000. By the time the market recovered in 2024, those bear market purchases had doubled or tripled in value. You do not need to predict when the bottom will happen — your DCA buys automatically capture it as long as you keep buying.

Already familiar with DCA as a concept? Skip to the Binance setup section or the OKX setup section to start configuring your automatic investments right now. For a deep dive on minimising the fees you pay on each DCA purchase, see our exchange fees guide.

Why DCA Works: Data, Not Gut Feeling

The Mathematical Basis

DCA works because of a mathematical property called the harmonic mean effect. When you invest a fixed amount at varying prices, you automatically buy more units when prices are low and fewer when prices are high. Your average cost per unit ends up lower than the arithmetic average of all the prices during your investment period. This is not a theoretical advantage — it is a mathematical certainty for any asset whose price varies over time.

Here is a concrete example with real numbers. Suppose you invest £100/week into Bitcoin over four weeks at these prices: Week 1 at £40,000, Week 2 at £32,000 (a 20% dip), Week 3 at £36,000, Week 4 at £44,000. Your total investment is £400. You bought 0.00250 BTC in Week 1, 0.00313 BTC in Week 2 (more because the price was lower), 0.00278 BTC in Week 3, and 0.00227 BTC in Week 4. Your total: 0.01068 BTC at an average cost of £37,453 per BTC. The arithmetic average price over those four weeks was £38,000. Your DCA gave you a 1.4% better entry price — and the advantage grows larger with more volatility.

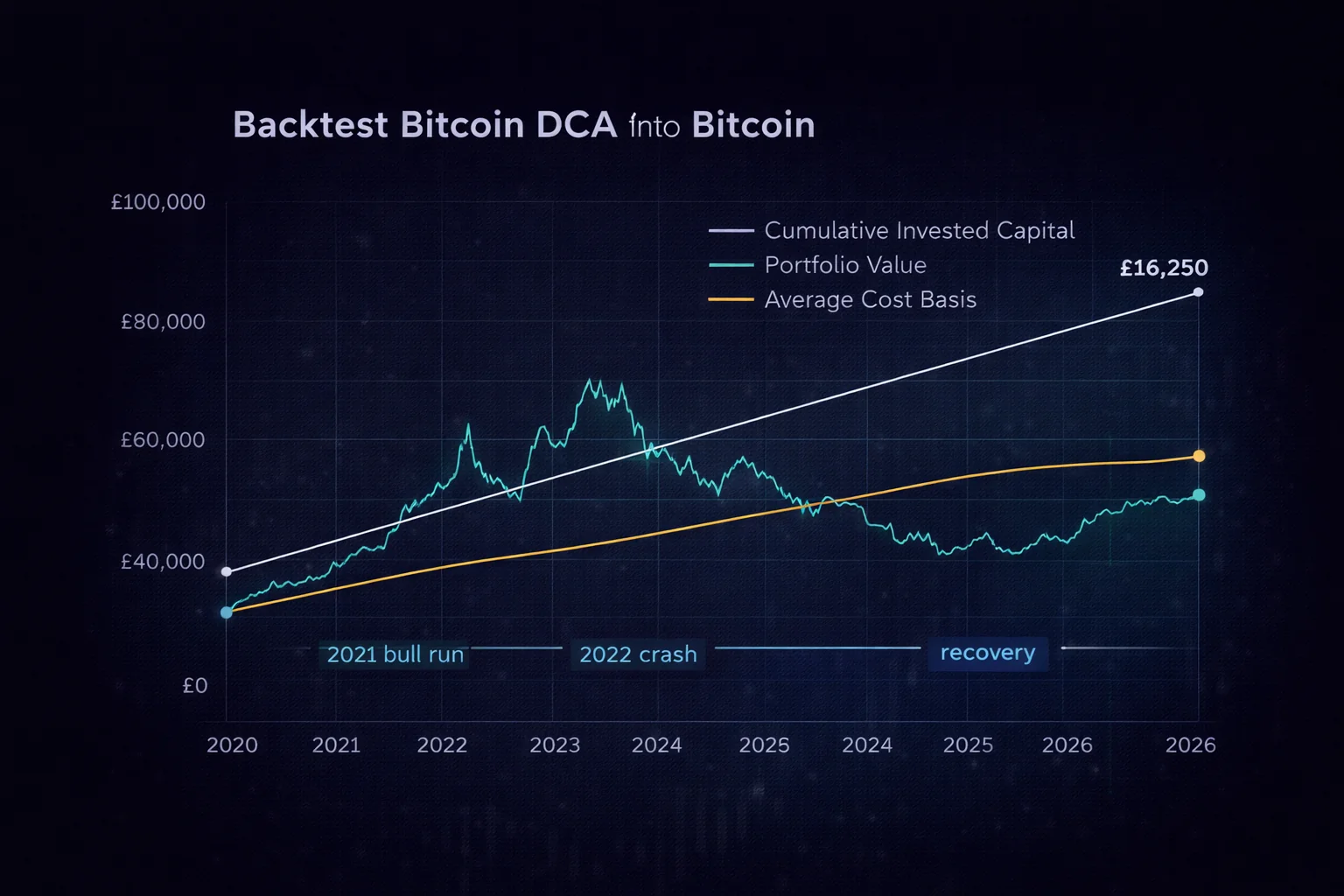

Historical Backtesting: Bitcoin and Ethereum

How has DCA actually performed in real market conditions? Let us look at the numbers. If you had invested £50/week into Bitcoin starting from January 2020, your total investment by April 2026 would be approximately £16,250 (325 weeks × £50). Despite buying through the 2021 bull run, the 2022 crash (Bitcoin fell from £48,000 to £13,000), and the 2024-2025 recovery, your portfolio value would be approximately £28,000-35,000 depending on exact timing — a 70-115% total return on a strategy that required zero market analysis.

What if you had invested that same £16,250 as a lump sum on January 1, 2020? Your return would depend entirely on the price that day — approximately £5,500 per BTC. A lump sum at that price would have returned approximately 400-600%. But here is the critical insight: you almost certainly would not have invested £16,250 on January 1, 2020. Most people who try to time the market wait for a dip, miss the rally, buy in at the top, panic sell during the crash, and end up with worse returns than a simple DCA. Your DCA strategy does not need to beat a perfectly timed lump sum — it needs to beat what you would actually do without a system.

Ethereum tells a similar story. A £50/week DCA into ETH from January 2020 would have returned approximately 80-140% by April 2026, with the wide range reflecting the extreme volatility of the 2021-2022 cycle. The DCA investor who bought through the crash at £800-1,000 per ETH accumulated significantly more units than someone who bought only during the 2021 euphoria at £3,000-4,000.

Shorter time windows tell a more uneven story and are worth seeing honestly. A £50/week DCA into Bitcoin starting in November 2021 (the previous cycle peak) would have been deeply underwater within 12 months — your £2,600 of cumulative buys would have been worth around £1,800 by November 2022 as the price collapsed 75%. By the end of 2024 the same position had recovered to around £4,500-5,500, and by April 2026 to £7,000-9,000.

The lesson is not that DCA always wins quickly. The lesson is that DCA is mechanically resilient: even if you start at the worst possible moment, the buys you continue making during the drawdown drag your average price down to a level that recovers as the cycle turns. The investor who panicked at the November 2022 low and stopped buying never captured that recovery; the investor who kept buying at £15,000-20,000 BTC ended up with the lowest cost basis in the entire 5-year window.

Frequency comparisons are also worth quantifying. Across the full 2020-2026 backtest window, weekly DCA produced an average cost basis approximately 1.8% lower than monthly DCA on the same total capital. That sounds large but translates to a difference of around £290 on a £16,000 cumulative investment — meaningful but not life-changing. Daily DCA improved on weekly by a further 0.3%, which barely covers the increased exchange fees on most platforms and adds significant operational friction for almost no measurable benefit on a typical retail balance over a multi-year horizon. The practical conclusion: weekly is the sweet spot for retail investors. More frequent than weekly delivers diminishing returns; less frequent gives up real averaging benefit during volatile periods.

DCA vs Lump Sum: When Each Strategy Wins

Should you always DCA instead of investing a lump sum? Not necessarily. Academic research (Vanguard, 2012; updated with crypto data by various analysts) shows that in a consistently rising market, lump sum investing outperforms DCA approximately 65% of the time because your money is invested for longer. However, this assumes you have the lump sum available and the discipline to invest it all at once regardless of current market conditions.

In practice, DCA wins for most beginners because it solves three real problems that lump sum investing does not. First, most people do not have £5,000-10,000 sitting idle to deploy — they earn income monthly and need a strategy that matches their cash flow. Second, the psychological burden of investing a large sum all at once is enormous — if the price drops 30% the week after your lump sum, you will question your decision and may panic sell. Third, DCA creates a sustainable habit that you maintain for years, while lump sum investments tend to be one-off events followed by months of inaction. For your first year of crypto investing, DCA is almost always the right approach.

Build Your DCA Plan

Which Assets Should You Buy?

For your first DCA strategy, you should stick to Bitcoin and Ethereum — the two largest cryptocurrencies by market capitalisation with the longest track records and deepest liquidity on every major exchange. A simple 70/30 split (70% BTC, 30% ETH) gives you exposure to both the "digital gold" narrative (Bitcoin, secured by proof-of-work mining and consensus) and the "smart contract platform" ecosystem (Ethereum, which powers DeFi protocols, governance tokens, and validator staking) without the complexity of managing multiple altcoin positions or tracking slippage on low-liquidity token pairs.

Why not include altcoins from the start? Because altcoins add risk without proportional reward for beginners. Most altcoins lose 80-95% of their value during bear markets and many never recover. Even the largest altcoins (Solana, Cardano, Avalanche) have experienced 85%+ drawdowns from their all-time highs. Bitcoin and Ethereum have also experienced major drawdowns (70-80%), but they have always recovered to new highs within 2-4 years. You should only add altcoins to your DCA after you have maintained a BTC/ETH strategy for at least 6-12 months and understand how crypto market cycles, tokenomics, and APY yields work.

Here are the most common beginner DCA portfolio allocations:

- Conservative — 100% Bitcoin. Your lowest-risk option within crypto. Suitable if you view crypto as a long-term store of value and custody asset.

- Balanced — 70% Bitcoin, 30% Ethereum. Your best risk/reward balance for a beginner. Gives you exposure to both major narratives.

- Growth — 50% Bitcoin, 30% Ethereum, 20% large-cap altcoins. Only suitable after 6+ months of experience. The altcoin allocation increases both your upside and downside.

How Much Should You Invest?

The most important rule: only invest money you can afford to lose entirely. Crypto is a volatile asset class — your portfolio can drop 50% in a single month and may take 2-3 years to recover. Your DCA amount should come from discretionary income after you have covered your essential expenses, maintained your emergency fund (3-6 months of living costs in a savings account), and contributed to your pension or ISA if applicable.

What does that look like in practice? For a UK-based earner on a £35,000 salary with typical expenses, a reasonable starting DCA might be £25-50/week (£100-200/month). For someone earning £60,000+ with lower expenses, £100-200/week (£400-800/month) may be appropriate. The exact amount matters less than your consistency — £25/week every week for two years builds a larger position and better habit than £200/week for three months followed by six months of nothing.

You should start smaller than you think you need to. Beginning with £25/week lets you experience your first 30% drawdown with only £100-200 at risk rather than £1,000+. If you handle that drawdown calmly and continue buying, increase your amount. If you find yourself checking the price hourly and losing sleep, you are investing too much relative to your risk tolerance. Your DCA amount should feel boring, not exciting.

Weekly, Bi-Weekly, or Monthly?

How often should you buy? Backtesting data across Bitcoin's entire history shows minimal difference between weekly, bi-weekly, and monthly DCA over periods longer than 2 years. Weekly DCA gives you a slightly better average entry price during periods of high volatility (approximately 1-2% better than monthly), but the transaction fees and gas fee costs on 52 trades per year versus 12 can partially offset this advantage if you withdraw to a private key wallet after each purchase.

The practical advice: match your DCA frequency to your income cycle. If you get paid monthly, set up a monthly DCA on the day after payday. If you get paid weekly, a weekly DCA makes more sense. The key is choosing a frequency you will actually maintain for years. A monthly DCA that you stick to consistently will outperform a weekly DCA that you forget about after two months because the setup was too fiddly.

One approach that works well for many UK investors: set up a weekly DCA for Bitcoin (your core position) and a monthly DCA for Ethereum (your secondary position). This gives you the smoother averaging of weekly buys on your largest allocation while keeping management simple for the smaller allocation.

DCA Variations Worth Knowing

Standard fixed-amount DCA is the right starting point for almost everyone. But once you have run a basic plan for six months and want to refine the approach, three documented variations are worth understanding. Each one trades simplicity for a slightly different risk-return profile, and each has measurable historical evidence to support it.

Value Averaging

Value averaging, formalised by Michael Edleson in the 1990s, replaces the rule "buy a fixed pound amount each period" with "buy enough to grow the portfolio by a fixed pound amount each period". For example, instead of investing £50 every week, you set a target of "grow my BTC position value by £50 per week". If the price falls and your existing position is worth less than expected, you buy more than £50 to make up the gap. If the price rises and your existing position is worth more than the target, you buy less — or in extreme cases sell some of the gain to bring the line back into shape. The mechanical effect is that value averaging buys more aggressively at lows and less at highs than fixed-amount DCA, modestly improving the long-run average price.

The trade-off is variable cash requirement. During a sharp drawdown, value averaging might call for a £200 buy when you only have £50 available, forcing you to either skip the period or hold a larger cash buffer than fixed DCA needs. For most beginners with limited spare cash, this complication is not worth the marginal improvement in average price. Value averaging is most useful for investors who already maintain a 6-12 month cash reserve and can stomach the occasional large buy.

Threshold and Dynamic DCA

A simpler variation is threshold DCA: maintain a baseline weekly buy, but double or triple it whenever the price falls below a defined level. For example, "£25/week normally, £75/week whenever BTC is more than 20% below its 90-day high". This rule captures more of any meaningful drawdown without requiring you to make discretionary judgements in the moment. The 90-day high acts as an anchor that updates automatically as the market evolves, so you do not have to guess what counts as a dip.

Dynamic DCA takes the same idea further by tying the buy size to a continuous indicator like the 200-day moving average rather than a discrete threshold. The trade-off is the same as value averaging: better mathematical performance, more cash flow variability, more rules to remember. For your first year stick to fixed DCA. After your first full bear-market cycle as a real participant, you have enough lived experience to choose whether the added complexity is worth it for you.

Dual-Pair DCA: BTC and Stablecoins

One variation worth considering even as a beginner is splitting your weekly buy between BTC/ETH and a stablecoin reserve. Instead of £50/week into BTC, run £40/week into BTC and £10/week into USDC held in flexible savings. The stablecoin pot grows steadily and can be deployed as a bonus buy whenever the price drops sharply. After six months you have around £260 of dry powder available for opportunistic buys without ever having to add fresh capital. This is the simplest way to get some of the benefit of dynamic DCA without the complexity, and it doubles as a behavioural anchor — having a visible cash reserve labelled "for buying dips" makes it psychologically easier to actually buy during the dip rather than freezing.

Step-by-Step: Binance Auto-Invest

Binance's Auto-Invest feature lets you set up recurring purchases of one or more cryptocurrencies from your GBP balance. Here is exactly how to configure it for a £50/week Bitcoin DCA. You should have already completed KYC verification and made at least one GBP deposit via Faster Payments before starting — if you have not, follow our exchange setup guide first.

Step 1: Navigate to Auto-Invest. Log into your Binance account. Go to Earn → Auto-Invest (or search "Auto-Invest" in the top search bar). You will see the Auto-Invest dashboard with options to create a new plan.

Step 2: Select your asset. Click "Create Plan" and select BTC (Bitcoin) as your target asset. If you want to DCA into multiple assets, you can create separate plans for each — for example, one plan for BTC and one for ETH with different amounts.

Step 3: Set your amount and frequency. Enter £50 as your recurring amount. Select "Weekly" as your frequency. Choose your preferred day of the week — Tuesday and Wednesday historically have slightly lower average prices than weekends, but the difference is negligible over long time periods. Pick a time of day (any time works — the price variation within a single day is irrelevant for a long-term DCA).

Step 4: Select your funding source. Choose "GBP Spot Wallet" as the payment source. This means your DCA purchases will draw from your GBP balance — you need to ensure you have sufficient GBP deposited before each scheduled purchase. If your balance is insufficient on the scheduled date, Binance will skip that purchase (it will not charge you overdraft fees or pull from other balances).

Step 5: Review and confirm. Check your settings: BTC, £50, weekly, from GBP balance. Confirm the plan. Binance will show you the next scheduled purchase date. Your Auto-Invest plan is now active — it will execute automatically every week until you pause or cancel it.

What about fees? Binance Auto-Invest uses the Convert rate rather than the spot trading rate, which means you pay a small markup (typically 0.1-0.3%) compared to placing a limit order manually on the spot page. For a £50/week DCA, this markup costs you approximately £0.05-0.15 per purchase, or £2.60-7.80 per year. You can eliminate this by manually buying on the spot page each week instead of using Auto-Invest, but for most beginners the convenience of automation outweighs the small fee difference. Our fees guide explains how to reduce costs further. If you do plan to switch to manual buys on the spot page, the limit, market, and stop order mechanics walk-through covers the order types you'll need to choose between on each purchase.

Step-by-Step: OKX Recurring Buy

OKX's Recurring Buy feature works similarly to Binance Auto-Invest. Here is how to set up a £50/week Bitcoin DCA on OKX. You should have completed identity verification and deposited GBP via Faster Payments before starting.

Step 1: Navigate to Recurring Buy. Log into your OKX account. Go to Trade → Recurring Buy (or find it under the "Bot Trading" section in the app). You will see the recurring buy dashboard.

Step 2: Configure your plan. Select BTC as your target asset. Enter £50 as your recurring amount. Choose "Weekly" as your frequency and select your preferred day and time. OKX lets you create multi-asset plans — you can allocate 70% to BTC and 30% to ETH within a single plan if you prefer, which simplifies management compared to running separate plans.

Step 3: Select your payment method. Choose your GBP balance as the funding source. Like Binance, OKX will skip the purchase if your balance is insufficient — you will not be charged overdraft or penalty fees.

Step 4: Review and activate. Confirm your settings and activate the plan. OKX will show your next scheduled execution date. You can monitor your plan's performance, adjust the amount, or pause it at any time from the Recurring Buy dashboard.

How does OKX pricing compare to Binance for DCA purchases? OKX Recurring Buy also uses an internal conversion rate rather than the spot order book, so you pay a similar 0.1-0.3% markup. OKX's base maker fee (0.08%) is slightly lower than Binance's (0.10%), but since both DCA features use the Convert rate rather than maker/taker pricing, the effective cost is comparable. Choose your exchange based on which platform you prefer overall, not on the marginal fee difference for DCA purchases.

Common Mistakes That Cost You Money

1. Stopping During Bear Markets

This is the most expensive mistake you can make with a DCA strategy — and the most common. When Bitcoin drops 40% and your portfolio is deep in the red, every instinct tells you to stop buying. But bear markets are when DCA delivers its best results. The purchases you make at £20,000 BTC are worth 3x more than the purchases you made at £60,000. If you stop buying during the dip, you miss the accumulation phase that produces the strongest long-term returns.

How can you prevent yourself from stopping? First, set your DCA amount low enough that continuing during a bear market does not cause financial stress. If £100/week feels uncomfortable when your portfolio is down 50%, reduce it to £25/week rather than stopping entirely. Second, do not check your portfolio daily during drawdowns — weekly or monthly check-ins are sufficient. Third, remind yourself that your DCA strategy is designed to span multiple market cycles (3-5+ years), not to produce returns in any single quarter.

2. Using Card Deposits Instead of Bank Transfers

If you fund your DCA purchases via debit card instead of Faster Payments bank transfer, you pay 1.5-3.5% in deposit fees on every purchase. On a £200/month DCA, card deposits cost you £36-84 per year in unnecessary fees. This is money that should be working for you in your portfolio, not going to the card processor. Always deposit via bank transfer — even if it takes an extra day to arrive.

The fix is simple: set up a standing order from your bank account to your exchange's GBP deposit address. Your money arrives every week or month automatically, with zero deposit fees, ready for your next scheduled DCA purchase. If your bank blocks transfers to crypto exchanges, try a different sending account or contact your bank's support team to whitelist the exchange.

3. Chasing the Latest Hot Token

Every few months, a new token goes viral on social media — up 500% in a week, everyone is posting screenshots of their gains, and you feel like you are missing out. The temptation is to redirect your DCA from boring BTC/ETH into the hot token. Do not do this. The vast majority of tokens that pump 500% in a week crash 90% in the following month. Your DCA into Bitcoin and Ethereum is a wealth-building strategy measured in years, not a speculation measured in days.

If you genuinely want to speculate on altcoins, allocate a separate "speculation budget" — no more than 5-10% of your total crypto allocation — and keep it completely separate from your DCA. Your DCA is your disciplined, long-term investment. Your speculation budget is your high-risk play money. Never mix the two.

4. Checking the Price Too Often

If you check Bitcoin's price 10 times a day, you will eventually sell at a loss during a panic. This is not a character flaw — it is a well-documented cognitive bias called loss aversion. Research shows that investors who check their portfolios daily make worse decisions than those who check monthly. Your DCA strategy is automated for a reason — let the automation work while you focus on your career, family, and hobbies.

A practical approach: check your portfolio once per month on the same day you review your bank statements. This gives you enough visibility to ensure your DCA is executing correctly without the emotional whiplash of daily price movements. If you find yourself unable to stop checking, delete the exchange app from your phone and log in only via desktop once a month.

5. Not Keeping Records for Tax

Every DCA purchase is an acquisition event that you must record for HMRC. If you make 52 weekly purchases per year and eventually sell some of your holdings, you need the date, GBP amount, BTC quantity, and GBP/BTC exchange rate for every single purchase to calculate your capital gains correctly. Failing to keep these records can result in HMRC estimating your cost basis at zero — meaning you pay Capital Gains Tax on the full sale proceeds rather than just the gain.

The solution: export your trade history from your exchange quarterly and store it in a secure location (cloud drive, password manager, or a dedicated crypto tax tool like Koinly). Some exchanges limit historical data access to 12-18 months, so you should download your records regularly rather than waiting until you need them for your Self Assessment tax return.

6. Spreading DCA Across Too Many Exchanges

A subtler mistake than the previous five: running parallel small DCAs on three or four different exchanges in the belief that this diversifies counterparty risk. In practice, splitting a £100/week budget into £25/week on Binance, £25 on Kraken, £25 on Coinbase, and £25 on OKX multiplies your management overhead, multiplies the number of tax export workflows you have to maintain, multiplies the number of separate KYC processes you must keep refreshed and verified each year as each platform demands periodic document re-checks along with updated proof-of-address evidence and source-of-funds questionnaires, multiplies the surface area for phishing attacks against your accounts, and rarely produces meaningful safety improvement on the kind of balances retail beginners actually hold.

The counterparty risk you actually face on a £5,000 balance is overwhelmingly addressed by moving the long-term portion to a hardware wallet, not by sprinkling it across four custodial accounts that each could fail in the same way.

The clean rule: one primary exchange for active DCA and trading, optionally one backup for redundancy if your portfolio exceeds £5,000, and a hardware wallet for everything beyond your active trading float. Multi-exchange complexity is for institutional sized portfolios where the operational overhead is justified by the absolute value at stake. For a beginner running £25-100/week DCA, the overhead always exceeds the benefit by a wide margin, and the time spent reconciling four different export formats every quarter is time you could have spent earning the income that funds the strategy in the first place.

When to Adjust or Stop Your DCA

Your DCA should run on autopilot most of the time, but there are legitimate reasons to adjust it. Here are the scenarios where you should consider making changes to your plan:

- Your income changes significantly — if you get a raise, you can increase your DCA proportionally. If you lose your job or take a pay cut, reduce your DCA to a level your emergency fund can sustain for 6 months.

- You need the money for an emergency — your DCA should never come from your emergency fund. If you face an unexpected expense, pause your DCA rather than selling your existing holdings at a potential loss.

- You reach your target allocation — if your crypto portfolio grows to represent more than 10-20% of your total net worth, consider reducing your DCA amount and directing new savings to other asset classes (index funds, ISA, pension) for diversification.

- Market conditions change fundamentally — not a 30% dip (that is normal volatility), but a genuine structural change like a major regulatory ban or a protocol-breaking security vulnerability. These events are rare but warrant a pause and reassessment.

When should you stop your DCA entirely? Only when you have reached your financial goal for this allocation. If you started DCA with the goal of accumulating 0.5 BTC over 3 years, and you reach that target, you can stop and shift to a maintenance mode (smaller, less frequent purchases). Alternatively, if your financial situation changes and you need to prioritise other goals (house deposit, paying off debt, starting a business), pausing your crypto DCA is a responsible decision.

What you should never do is stop your DCA because you are "waiting for a better price." This is market timing disguised as patience, and it defeats the entire purpose of DCA. If you have decided to invest £50/week into Bitcoin, the best time to make your next purchase is your next scheduled date — not when you think the price has bottomed. You are not smarter than the market, and neither is anyone else.

Tax Implications and Record Keeping

In the UK, buying cryptocurrency is not a taxable event. Your DCA purchases do not trigger any Capital Gains Tax liability when you make them. Tax only applies when you dispose of your crypto — selling for GBP, swapping for another cryptocurrency, or spending it on goods and services. Each disposal is a taxable event where you calculate your gain or loss based on your cost basis under HMRC's share pooling rules.

How does share pooling work with DCA? Under Section 104 of the Taxation of Chargeable Gains Act, all your BTC purchases are pooled together into a single holding. If you bought 0.001 BTC at £40,000 and 0.002 BTC at £30,000, your pooled cost basis is (£40 + £60) / 0.003 = £33,333 per BTC. When you sell any amount, your gain is calculated against this pooled average cost, not against the specific purchase that you "mentally" allocated to that sale. This makes record keeping simpler: you just need the total cost and total quantity in your pool.

Your Capital Gains Tax allowance for 2025-2026 is £3,000. This means you can realise up to £3,000 in gains per tax year without paying any CGT. For a DCA investor who has accumulated £5,000-10,000 in crypto over 2-3 years, this allowance often covers your entire gain if you sell gradually. If your gains exceed the allowance, you pay 10% (basic rate taxpayer) or 20% (higher rate taxpayer) on the excess.

What records should you keep? For every DCA purchase, you need to record:

- Date of purchase

- GBP amount invested (including any fees)

- Quantity of crypto received

- Exchange used and order reference

- GBP/BTC or GBP/ETH exchange rate at time of purchase

You can maintain these records manually in a spreadsheet, or use a crypto tax tool like Koinly or CoinTracker that imports your exchange data automatically via API. If you trade on multiple exchanges or also use DeFi protocols for staking or lending, a dedicated tax tool is worth the £49-99/year subscription cost because it handles the complexity of cross-platform share pooling that would take hours to calculate manually.

Pausing and Restarting Your DCA

Life happens. A job change, a redundancy, a house purchase, an unexpected bill — there are many legitimate reasons your DCA might need to pause for a while. The mechanical question (how to pause the plan in the exchange UI) is trivial: both Binance Auto-Invest and OKX Recurring Buy have a single button. The harder question is how to handle a pause without losing the discipline that made the strategy work in the first place.

Pause Is Not the Same as Stop

The most useful framing is to treat any interruption as a pause with a defined restart trigger, not as an open-ended stop. Before you cancel the auto-buy, write down what condition needs to be true before you turn it back on. "When my emergency fund is back above £3,000." "When my new contract starts in three months." "When my mortgage offer is finalised." Without that explicit condition, a six-month pause silently becomes an eighteen-month stop, and the eighteen-month stop becomes "I used to DCA into Bitcoin a few years back". The plan you had at month one was good. The plan you have at month eighteen, after watching the price move without you, is almost always worse.

If you can afford to keep buying at a smaller amount, do that instead of pausing entirely. Reducing a £50 weekly DCA to £10 maintains the habit, the cost-basis records, and the psychological commitment, while freeing up 80% of the cash flow. The £10 you keep buying with is enough to ensure you do not develop the muscle memory of "I do not buy crypto any more". The accounting cost of restarting an active account is much lower than restarting a dormant one.

Restarting After a Long Pause

If you do end up stopping for six months or more, the restart is more psychologically loaded than the original setup because the price has moved. If BTC is now 40% higher than when you stopped, the temptation is to wait for it to come back down. If BTC is now 40% lower, the temptation is to "wait and see whether it goes lower". Both temptations are forms of market timing dressed up as caution. The honest answer is that neither past price gives you any information about the future, and the cost of waiting is the same opportunity cost the original DCA was designed to avoid.

The cleanest restart procedure is to treat the new period as if it were day one of a fresh DCA. Pick the amount that fits your current cash flow, set the schedule to whatever matches your income now, and execute the first purchase the same day you make the decision. Do not try to "catch up" by lump-summing the missed weeks — that defeats the entire smoothing benefit of DCA. Just resume the rhythm and let time do the work. If you are restarting after a serious bear market, the first six months of restart purchases will probably end up being some of the best entries in your entire history, because that is when fearful investors are sitting out and prices reflect their absence.

Changing the Amount Without Stopping

A salary change, a rent increase, or a new financial goal might mean you need to change the DCA amount rather than pause. Both Binance and OKX let you edit the recurring amount on an existing plan without cancelling and recreating it, which preserves your historical record and makes tax reporting cleaner. Edit the amount, not the entire plan. If you cancel and create a new plan with the same name, some exchanges treat it as a new product internally, which can confuse export tools when you reconcile your records months later. The fewer "fresh starts" your tax history contains, the simpler your year-end Self Assessment will be.

Conclusion

DCA is the most reliable entry strategy for new crypto investors because it solves the three problems that derail most beginners: timing anxiety, emotional decision-making, and inconsistency. By investing a fixed amount at regular intervals, you guarantee that you buy more when prices are low and less when prices are high — a mathematically optimal approach that requires zero market analysis. Your only job is to set it up, fund your account, and not interfere.

The setup takes under 10 minutes on either Binance (Auto-Invest) or OKX (Recurring Buy). Start with £25-50/week into Bitcoin, or split 70/30 between BTC and ETH if you want broader exposure. Fund your account via Faster Payments bank transfer (never card deposits). Export your trade records quarterly for your tax return. And most importantly, do not stop buying during bear markets — that is when your DCA strategy delivers its strongest long-term value.

The five mistakes to avoid: stopping during bear markets (the most expensive error), using card deposits instead of free bank transfers, chasing hot altcoins instead of sticking to your BTC/ETH plan, checking prices too frequently (which triggers emotional decisions), and failing to keep tax records from day one. If you avoid these five mistakes and maintain your DCA for at least 2-3 market cycles, you will outperform the vast majority of retail crypto investors who try to time their entries and exits.

Your next steps: if your account is ready, set up your Auto-Invest or Recurring Buy today and make your first automated purchase this week. If you have not yet set up an exchange account, follow the exchange setup guide referenced earlier before returning here to automate. For those already DCA-ing who want to learn about earning additional yield on their holdings, read our exchange earn and staking features guide.

Sources and References

Frequently Asked Questions

- How much should I invest per week with DCA?

- Start with an amount you can afford to lose entirely — typically £25-100/week for most UK beginners. The key principle is consistency over size. £25/week invested every week for a year (£1,300 total) will likely outperform £1,300 invested as a single lump sum if you time it wrong. Only increase your DCA amount after you have maintained the habit for at least 3 months and experienced at least one significant market drawdown without panicking.

- Is weekly or monthly DCA better?

- For Bitcoin and Ethereum, backtesting data shows minimal difference between weekly and monthly DCA over periods longer than 2 years. Weekly DCA gives you slightly better average entry prices during volatile periods, but the difference is typically under 2% annually. You should choose the frequency that matches your income cycle — if you get paid monthly, a monthly DCA on payday is simpler and equally effective over the long term.

- Should I DCA into altcoins or just Bitcoin?

- For your first 6-12 months, you should stick to Bitcoin and Ethereum only. These two assets have the deepest liquidity on every exchange, the strongest track records, and the lowest risk of going to zero compared to altcoins. After you understand market cycles and have a stable DCA habit, you can allocate 10-20% of your DCA to a small number of large-cap altcoins with strong fundamentals — but never more than you can afford to lose entirely.

- Can I pause my DCA during a bear market?

- You can, but you probably should not. Bear markets are when DCA delivers its strongest results — you buy more units at lower prices, reducing your average cost basis significantly. Pausing during a bear market and resuming during a bull market is effectively buying high and missing the lows, which defeats the purpose of DCA. If you cannot afford your current DCA amount during a downturn, reduce it to £10-25/week rather than stopping entirely.

- Do I pay tax on DCA purchases in the UK?

- Buying crypto is not a taxable event under HMRC rules. You only owe Capital Gains Tax when you sell, swap, or spend your crypto. Each DCA purchase creates a new acquisition that gets pooled into your Section 104 holding under HMRC share pooling rules. You should record the date, GBP amount, quantity, and exchange rate for every purchase — you will need these records for your annual Self Assessment return when you eventually dispose of any of your holdings.

Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.