Crypto Exchange Earn and Staking Guide 2026

How to earn yield on your crypto holdings through exchange staking, savings, and lending — with real APY rates, honest risk assessment, and a clear path from CEX earn to DeFi.

Introduction

Once you have bought your first cryptocurrency through a DCA strategy or a one-off purchase, your tokens sit in your exchange wallet earning nothing. Meanwhile, those same tokens could be generating yield — 2-7% APY on proof-of-stake assets like ETH and SOL, or 1-4% on stablecoin savings products. Exchange earn features let you put your idle crypto to work without leaving the platform, without setting up a separate wallet, and without interacting with any blockchain smart contract directly.

Every major centralised exchange now offers an "Earn" section: Binance has Earn (with Simple Earn, Staking, and Launchpool), OKX has Earn (with Savings, Staking, and Structured Products), Kraken has Staking. These products vary in complexity, yield, and risk — and the marketing pages rarely explain the risks clearly. Some products are genuinely low-risk: flexible USDT savings backed by the exchange's balance sheet. Others expose you to smart contract risk, slashing penalties, impermanent loss on liquidity pools, or extended lock-up periods that could leave your funds stuck during a market crash.

This guide explains every type of earn product you will encounter on a cryptocurrency exchange, shows you the real APY rates after the exchange takes its commission, walks you through the setup process on Binance and OKX, and gives you an honest assessment of the risks involved. You will also learn when it makes sense to graduate from exchange earn products to DeFi protocols like Lido, Aave, and EigenLayer — where the yields are often higher but the complexity and self-custody responsibility increase significantly.

The marketing language around exchange earn deserves a quick translation. "APY" on a flexible savings product is rarely a fixed promise — it is a rolling estimate that updates as borrower demand changes. "Up to 12%" headlines almost always refer to a teaser rate paid for the first 30 days on a small balance, with the standard rate dropping by half or more once the promo ends. "Staking" sometimes means real protocol participation through validators, and sometimes means lending dressed up in staking language for marketing reasons. Knowing which is which lets you compare products on their actual mechanics rather than on the cleanest-looking number on the dashboard.

The structure of this guide tracks the natural learning curve. The first three sections cover what each product actually is (savings, staking, structured), what you actually earn after fees, and how to set the simple ones up on the two largest UK-friendly exchanges. The next two sections cover risks honestly — including the recent history of CeFi yield product failures that wiped out billions in customer balances. The final sections cover the transition to DeFi, the UK tax implications under HMRC's income and capital gains rules, and a five-minute checklist for getting your first earn position running today on whatever balance you already hold.

If you are completely new to exchanges, start with our first 30 days on a crypto exchange guide. If you want to understand the fees involved in moving your crypto between earn products, see our exchange fees guide.

Types of Exchange Earn Products

Flexible Savings

Flexible savings is the simplest earn product available on your exchange. You deposit your cryptocurrency (typically BTC, ETH, or stablecoins like USDT and USDC) into the savings product and earn interest daily. You can withdraw at any time with no lock-up and no penalty. Your funds stay as liquid as your spot wallet. What is the trade-off? You earn a lower APY than locked products.

How does the exchange generate this yield? On most platforms, your deposited tokens are lent to margin traders who pay interest to borrow them. The exchange takes a 10-20% commission and passes the rest to you. Your yield fluctuates with market demand. During volatile periods, more traders want to borrow — so your APY goes up. During quiet markets, it drops.

What APY can you expect? On Binance Simple Earn Flexible, USDT currently yields approximately 1.5-3% APY, BTC yields 0.5-1.5%, and ETH yields 1-2.5%. These rates change daily. On OKX Savings, the rates are comparable. For context: a UK savings account pays 3-5% APY on GBP with FSCS protection up to £85,000. Flexible crypto savings pays less than a bank account for stablecoins but offers exposure to the underlying asset's price appreciation (for BTC and ETH).

Locked Staking and Fixed-Term Products

Locked staking requires you to commit your tokens for a fixed period — typically 30, 60, 90, or 120 days. In return, you earn a higher APY than flexible savings. Your tokens are locked during this period. You cannot withdraw, sell, or transfer them until the lock ends. Some exchanges let you redeem early with a penalty (you forfeit accumulated rewards). Others do not let you redeem early at all — your tokens are truly locked.

Should you use locked products? Only if you are sure you will not need those tokens during the lock period. What happens if Bitcoin drops 40% while your BTC is locked for 90 days? You cannot sell. For a long-term DCA investor, the lock-up does not matter — your tokens were not going anywhere. But if you trade actively and might need to sell at short notice, locked products create a dangerous constraint on your liquidity.

What rates can you expect? On Binance: ETH 30-day lock yields 2.8-3.2% APY, ETH 120-day lock yields 3.5-4%, SOL 30-day yields 6-7%, USDT 30-day yields 3-5%. OKX offers similar rates. The premium for locking over flexible is 0.5-1.5 percentage points. Is that worth it? On a £1,000 ETH position, the gap between 2.5% flexible and 3.5% locked is just £10/year. You decide if the lost liquidity is worth £10.

Native Proof-of-Stake Staking

Native staking is fundamentally different from savings products. When you stake ETH through Binance or OKX, your tokens are delegated to validator nodes on the Ethereum network. These validators participate in the proof-of-stake consensus mechanism that secures the blockchain. Your rewards come from the protocol itself — not from lending. Why does this matter to you? Because protocol yield is more sustainable than lending yield. It does not depend on borrower demand. As long as the network needs validators, you earn rewards.

The exchange runs the validator infrastructure on your behalf. You do not need to run your own node (which requires 32 ETH). You do not need to manage private keys for a validator or worry about uptime. The exchange handles all of this and charges a 10-25% commission on your rewards. If the base ETH staking yield is 3.5% APR and the exchange takes 20%, your net APY is about 2.8%.

Native staking is available for proof-of-stake tokens: ETH, SOL, ADA, DOT, ATOM, AVAX, and others. Each token has different reward rates and unbonding periods. ETH has a 1-5 day withdrawal queue. SOL takes 2-3 days to unstake. DOT has a 28-day unbonding period — during which your tokens earn nothing and cannot be moved. You should check the unstaking timeline before you commit any tokens.

The ETH staking yield is also more nuanced than a single APR number suggests. The base validator reward is around 2.6% APR for issuance plus 0.4-0.8% from priority fees and MEV (maximal extractable value) captured during block proposals. Whether the exchange passes the MEV portion to you depends on the operator. Binance keeps roughly 25% of total rewards, including MEV, OKX about 15-20%, Kraken about 15%, and Coinbase about 25%. The differences look small as percentages but compound noticeably over multi-year horizons: a 10% commission gap on a £10,000 ETH stake at 3.5% gross APR is around £35/year — modest in year one, meaningful by year five with reinvestment. If staking yield is the main reason you hold ETH on a centralised platform, the operator's commission policy is the single biggest variable to optimise around.

The withdrawal queue on Ethereum deserves a separate note. After the Shanghai upgrade in 2023, exiting validators are processed in a first-in-first-out queue limited to a fixed number per epoch. Under normal conditions, a request clears in 1-5 days. During mass-exit events (large protocols unwinding, major exchange unstakes), the queue has stretched to 10-14 days. Exchange staking products inherit this delay because the underlying ETH still has to leave the validator. If liquidity within days matters more than the extra basis points of native yield, a liquid staking token (covered next) sidesteps the queue entirely by letting you sell the wrapped position on the spot market.

Liquid Staking Tokens on Centralised Exchanges

The newest category of exchange-earn product is the liquid staking token (LST) — a wrapped representation of your staked ETH that you can trade, transfer, or use as collateral while the underlying position keeps earning yield. Binance issues WBETH (Wrapped Beacon ETH); the older BETH token still exists but has been gradually phased out in favour of WBETH as the canonical wrapper. Other major exchanges either offer their own equivalent or integrate Lido's stETH directly through their Earn interface.

How WBETH and Similar Tokens Work

When you subscribe to ETH on Binance ETH staking and choose the WBETH option, the exchange takes your ETH, sends it to validators, and credits your account with WBETH at the current exchange rate. That rate starts at 1.000 WBETH per ETH and gradually increases as staking rewards accumulate. After a year of 3% net staking APY, 1 WBETH might be redeemable for 1.030 ETH. You do not see daily reward distributions in the way you would with Simple Earn — instead, the token's redemption value silently grows. This is mechanically identical to how Lido's stETH works, except issued and redeemed by a centralised counterparty.

The two practical advantages over traditional Simple Earn staking are liquidity and composability. WBETH trades on the Binance spot market, so you can sell your staked position at any time without joining the validator exit queue — useful if ETH crashes and you want out within minutes rather than days. WBETH can also be used as collateral on Binance Loans, letting you borrow USDT against your staked position without unstaking. Neither feature is available with the standard "Locked ETH Staking" product, which holds your ETH inside the earn account with no transferable representation.

Risks Specific to Liquid Staking Tokens

Liquid staking tokens carry one risk that ordinary staking does not: the token can trade at a discount to the underlying ETH. During the March 2023 banking turmoil, stETH briefly traded at a 7% discount to ETH on secondary markets because liquidity providers panicked. WBETH has historically held closer to peg because Binance acts as the redemption backstop, but in a stressed market the discount could widen and effective slippage on a forced sale can exceed several years of accumulated yield in a single trade. For example, on a £10,000 WBETH position, a 5% discount-to-peg sale costs you £500 — roughly equivalent to 18 months of net staking rewards at 3% APY. The defence is the same as for any wrapper: sell only at peg and treat the discount-to-fair-value spread as a short-term cost of liquidity rather than a long-term feature.

The second risk is operator concentration. If most exchange ETH stakers funnel into WBETH, Binance's validator share of the Ethereum network grows. Concentrated validator share is a long-running concern in the Ethereum community because it creates censorship and consensus risks. This is not a financial risk to your individual position, but it is a reason serious long-term ETH holders sometimes prefer non-custodial liquid staking via Rocket Pool or distributed protocols rather than any single exchange's wrapper.

Launchpool and Promotional Products

Have you seen "Launchpool" on Binance? This feature lets you stake your existing tokens (usually BNB, USDT, or the exchange's native token) to earn a new token that is about to be listed. The APY can look extremely high (50-200%+ annualised) during the farming period. But these events typically last only 5-10 days. Your actual return depends on how many users participate — the more tokens staked, the smaller your share of the reward pool.

Should you participate in Launchpool? If you already hold BNB or USDT on Binance, yes — there is no downside. You keep your original tokens and receive the new token for free. The risk is minimal if you were holding those tokens anyway. But should you buy BNB specifically to farm a Launchpool event? No. The BNB price volatility during the event can easily exceed the value of your farmed tokens.

Structured Products and Dual Investment

Structured products (called "Dual Investment" on Binance, "Shark Fin" on OKX) are options-based products that offer higher yields in exchange for conditional outcomes. For example, a BTC Dual Investment might offer 15% APY if BTC remains below £55,000 by the settlement date; if BTC exceeds £55,000, you receive your principal in USDT instead of BTC (effectively selling your BTC at the strike price). These products are not suitable for beginners. They involve complex tokenomics, governance token mechanics, and options pricing. You can lose money relative to simply holding the underlying asset. Avoid them until you understand the options well.

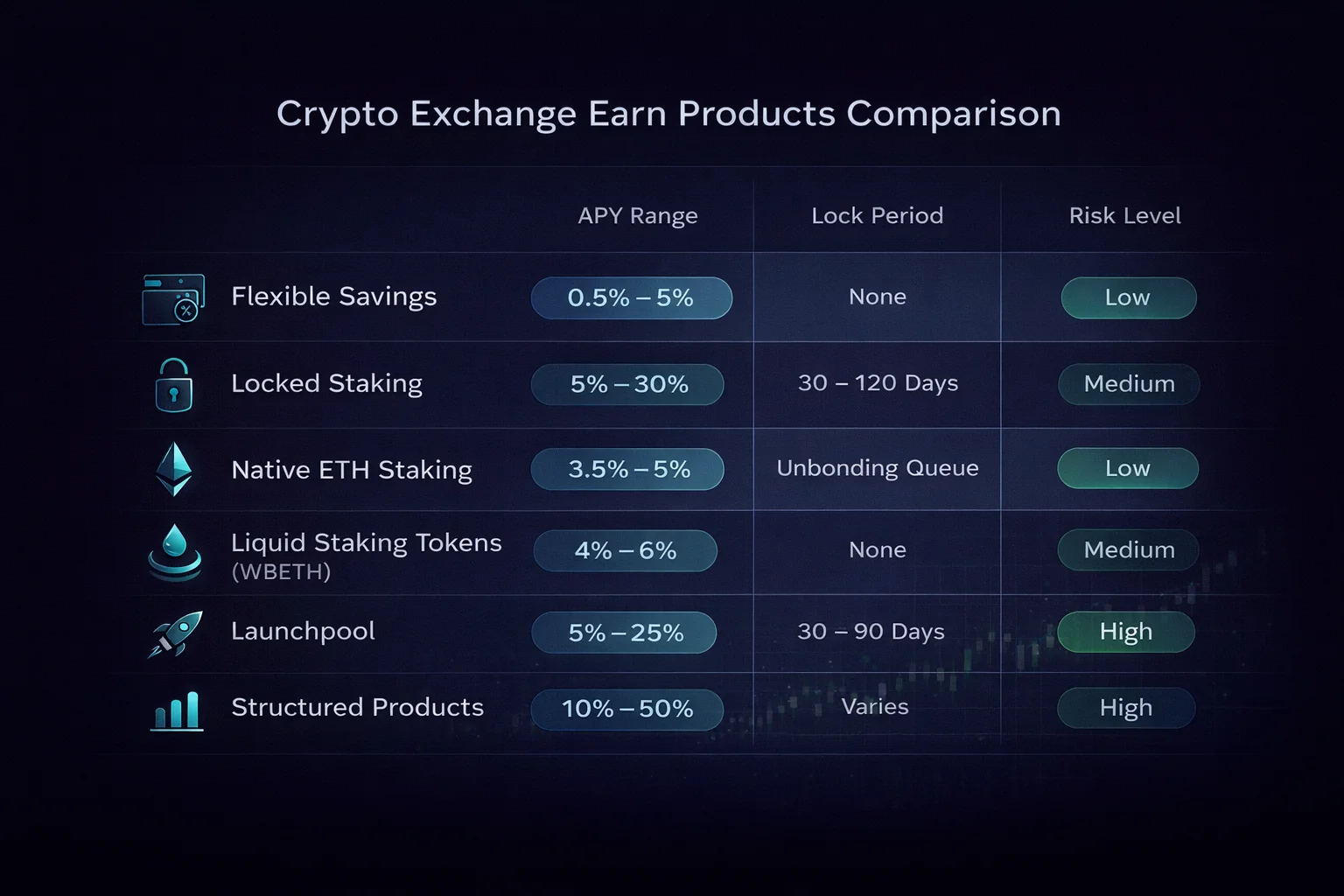

Here is a summary of all earned product types and their characteristics:

- Flexible Savings — withdraw anytime, 0.5-3% APY, lowest risk amongst earn products

- Locked Staking — fixed term (30-120 days), 2-7% APY, higher yield but no liquidity

- Native Staking — real protocol yield from validator participation, 2.5-7% APY, unbonding period applies

- Liquid Staking Tokens (WBETH) — wrapped staked ETH, tradeable on spot, no unbonding queue

- Launchpool — stake existing tokens to earn new tokens, high short-term APY, event-based

- Structured Products — options-based, 10-50% APY, complex risk profile, not for beginners

Real APY Rates: What You Actually Earn

Advertised vs Real Rates

Exchanges advertise headline APY rates that look attractive, but your actual return is lower after you account for the exchange's commission and rate fluctuations. When Binance advertises "3.5% APY on ETH staking," that is the rate before their commission. If Binance takes a 20% commission on staking rewards, your net APY is 2.8%. The commission is not always clearly displayed — you should calculate your actual earnings by checking your reward history, not by trusting the advertised rate.

How can you verify your real APY? After one month of staking, check your total rewards received. Divide the reward value by your staked principal, multiply by 12 (to annualise), and compare against the advertised rate. If Binance advertises 3.5% and you are receiving an effective 2.7%, the difference is the commission plus any rate fluctuation. This verification takes five minutes and prevents you from overestimating your returns in your portfolio tracking.

Current Rates Across Major Exchanges

Here are the approximate yield rates you can expect on the most commonly staked assets as of early 2026. These rates fluctuate — always check the current rate on your exchange before committing your tokens:

- ETH staking — Binance: 2.5-3.2% net APY, OKX: 2.5-3.0%, Kraken: 2.5-4.0% (Kraken charges lower commission)

- SOL staking — Binance: 5-7% net APY, OKX: 5-6.5%, higher yield reflects the Solana network's higher inflation rate

- USDT flexible savings — Binance: 1.5-3% APY, OKX: 1-3%, fluctuates with borrowing demand

- BTC flexible savings — Binance: 0.5-1.5% APY, OKX: 0.3-1%, lowest rates because BTC cannot be natively staked

- USDT 30-day locked — Binance: 3-5% APY, OKX: 3-4.5%, premium over flexible for committing to the lock period

How does this compare to a bank? A UK easy-access savings account pays you 3-5% APY with FSCS protection. Stablecoin savings pays similar rates but without deposit insurance. Where exchange earn shines is on proof-of-stake assets. You earn protocol yield on ETH and SOL that has no traditional finance equivalent — your bank cannot offer you staking rewards. Even BTC, which uses proof-of-work mining rather than staking, can earn you savings yield through lending on your exchange.

Setting Up Earn on Binance

Binance Simple Earn

Binance Simple Earn is the easiest way to start earning yield on your holdings. Here is how to set it up for ETH staking. You should already have ETH in your Binance spot wallet — if you have been following our DCA strategy guide, you will have accumulated ETH through your recurring purchases.

Step 1: Log into Binance and navigate to Earn → Simple Earn. You will see a list of all available tokens with their current APY rates.

Step 2: Search for ETH and click "Subscribe." You will see two options: Flexible (withdraw anytime, lower rate) and Locked (fixed term, higher rate). For your first time, choose Flexible — you can always switch to locked later once you are comfortable.

Step 3: Enter the amount of ETH you want to stake. You can stake all of your ETH or keep some in your spot wallet for trading. Binance shows you the estimated daily reward based on the current APY.

Step 4: Enable "Auto-Subscribe" if you want future DCA purchases to automatically flow into the earn product. This is a powerful feature for DCA investors — your weekly ETH purchases automatically start earning yield without any manual intervention.

Step 5: Confirm and subscribe. Your ETH begins earning rewards immediately (for flexible) or from the next distribution cycle (for locked). Your rewards are distributed daily and automatically added to your earn balance, compounding over time.

Auto-Subscribe: The Set-and-Forget Approach

The most powerful feature of Binance Simple Earn for DCA investors is Auto-Subscribe. When enabled, any ETH (or other token) that arrives in your spot wallet — whether from a DCA purchase, a manual buy, or a transfer from another exchange — is automatically subscribed to the earn product. This means your holdings are always earning yield with zero manual effort. You should enable Auto-Subscribe for every token you plan to hold long-term.

Setting Up Earn on OKX

OKX Earn Products

OKX Earn works similarly to Binance Simple Earn. Navigate to Finance → Earn to see all available products. OKX splits its earn products into three categories: Simple Earn (flexible and fixed-term savings), On-chain Earn (native staking via DeFi protocols), and Structured Products (advanced options). Which should you choose? Start with Simple Earn.

Step 1: Go to Finance → Earn → Simple Earn. Search for the token you want to stake (ETH, SOL, USDT, etc.).

Step 2: Choose between Flexible and Fixed Term. OKX displays the current APY for each option clearly. Subscribe with your desired amount.

Step 3: OKX also offers auto-subscription similar to Binance. You should enable it for every token you hold long-term so your purchases automatically start earning from day one.

OKX On-Chain Earn

OKX On-Chain Earn is a unique feature that connects you to DeFi protocols directly through the OKX interface. You can stake ETH via Lido (receiving stETH liquid staking tokens), provide liquidity to Aave lending pools, or participate in EigenLayer restaking — all without leaving the OKX app or managing your own wallet. This is a convenient bridge between centralised exchange earn and full DeFi participation.

Should you use On-Chain Earn? It offers you higher yields than Simple Earn because you access the full DeFi protocol rate with no exchange commission. But it adds smart contract risk. If a protocol gets exploited, your funds could be at risk. For your first few months, you should stick to Simple Earn. Consider On-Chain Earn only after you understand how DeFi protocols work and can evaluate their security track records.

Risks You Must Understand

Counterparty Risk

When you deposit tokens into an exchange earn product, you trust the exchange to hold your assets safely. If the exchange becomes insolvent, gets hacked, or freezes withdrawals, you may lose your deposited tokens. This is not a theoretical risk. FTX collapsed in November 2022. Customers who had tokens in FTX Earn products lost billions. Your staked tokens on a centralised exchange are not protected by any deposit insurance like the UK's FSCS.

How should you manage this risk? First, never stake more than you can afford to lose on any single exchange. Second, if your portfolio exceeds £5,000, you should split it across two exchanges. Third, for holdings above £2,000-5,000, consider moving to self-custody with a hardware wallet. You can stake through native DeFi protocols instead of exchange products. Our hardware wallet security guide explains how to set up self-custody.

The recent history of CeFi yield product failures is worth understanding in detail because each one teaches a different lesson. Celsius Network froze customer withdrawals in June 2022 with around $4.7 billion in customer deposits at stake. Those funds had been advertised as paying 8-17% APY on stablecoins — yields generated by lending the deposits into uncollateralised institutional loans that defaulted in the May 2022 Terra collapse. Celsius customers received fractional recoveries through a multi-year bankruptcy process; the headline yield turned out to be funded by leverage rather than sustainable revenue. BlockFi followed in November 2022 with $10 billion in customer assets affected, much of it tied to FTX exposure. FTX itself collapsed two days earlier with around $9 billion of customer crypto missing — funds that had been silently moved to its sister hedge fund Alameda Research and lost on directional trades.

The pattern across all three failures is the same. Earn rates significantly above 8% on stablecoins were sustained by undisclosed counterparty risk. When the underlying loans defaulted or the trading book blew up, customer balances were unrecoverable because they were not segregated from the operator's own funds. Binance and OKX run different business models — primarily exchange fees and conservative lending books — but the core lesson applies regardless of operator: any deposit on a centralised platform is an unsecured claim on that platform, no different in legal standing from a bank deposit before deposit insurance existed. The £85,000 FSCS protection that covers your high-street current account does not extend across the threshold.

Lock-Up and Liquidity Risk

If you lock your tokens for 90 days and the market crashes 50% on day 15, you cannot sell until day 90. By then, the price may have recovered — or it may have fallen further. Locked staking is only appropriate for tokens you have already decided to hold regardless of short-term price movements. If there is any chance you might want to sell during a downturn, use flexible savings instead of locked products. The extra 0.5-1.5% APY from locking is not worth the risk of being unable to exit a losing position.

A useful framing: the lock premium is the cost of an option you are selling to the exchange. By committing your tokens for 90 days, you give up the right to sell during that window. The exchange compensates you with a slightly higher rate. Whether that compensation is fair depends on how much you would value the option in a stress scenario. For tokens you are confident you would never sell anyway (your long-term BTC and ETH cold-storage allocation), the option has near-zero value to you and locking is rational. For tokens you actively trade or might need to convert to cover an unexpected expense, the option is valuable and the lock premium will not cover its loss in a real downturn. Match the product to the actual liquidity profile of the underlying capital, not to the headline yield.

Variable APY Risk

The APY rates you see are not guaranteed. Flexible savings can drop from 3% to 0.5% overnight if borrowing demand falls. Staking rewards fluctuate as network participation changes. You should never build your financial plan around a specific rate lasting forever. Treat your earn product yield as a bonus, not as your primary income source.

Stablecoin yields are particularly sensitive to the broader crypto credit cycle. During the 2021 bull market, USDT flexible savings on Binance paid 8-12% APY because borrower demand for leverage was extreme. By the bottom of the 2022 bear market the same product paid 1.5-2.5% — a 70% reduction in yield. ETH staking rewards moved less dramatically in the same window, dropping from around 5% APR (when network usage was high and priority fees were elevated) to around 3% APR (when activity cooled). The lesson: rate-sensitive deposits should be re-evaluated quarterly, not set once and ignored. A product that made sense at 5% may not make sense at 1.5% if the lock-up cost or counterparty risk has not changed in proportion.

One practical habit that helps: write down the headline rate when you subscribe and check it again 30 and 90 days later. If the rate has moved more than 1 percentage point, take a moment to ask whether the trade-off still makes sense. For locked products, this check is moot until the term expires — but it informs whether you re-lock at the new rate or move into a flexible position instead. Many beginners discover months after the fact that their "high yield" stablecoin product has been paying half the original rate for weeks because they never looked.

Slashing Risk on Proof-of-Stake Tokens

When you stake ETH or other proof-of-stake tokens, the validator node that holds your stake can be penalised (slashed) if it behaves incorrectly — double-signing a block, going offline for extended periods, or violating the consensus protocol rules. Slashing penalties can range from 0.5% to your entire stake depending on severity. On exchange staking, the exchange runs the validators and typically absorbs minor penalties. But in a major slashing event, the exchange may pass some of the loss to you. Should you worry about this? For large exchanges with professional infrastructure, slashing risk is very low — but not zero. You should factor it into your decision on how much to stake.

Real-world slashing events on Ethereum have been rare and small. The largest single-event slashing on the Ethereum mainnet to date was the Staked.us incident in February 2023, where 75 validators were slashed for around 75 ETH total — roughly 1 ETH per validator on a 32 ETH stake, or about a 3% loss for that specific operator's customers. Compared to the daily price volatility of ETH itself, which regularly delivers 3-5% intraday moves during normal market conditions and 8-12% during news-driven days, the financial impact of even a worst-case slashing event on a well-managed validator is dwarfed by ordinary mark-to-market swings on the underlying staked ETH token itself across a normal trading day.

Most major exchanges publish slashing-coverage policies stating they will absorb operator-fault slashing up to a certain percentage. Binance's policy reimburses customers for slashing losses caused by Binance's own infrastructure, but excludes losses caused by protocol-level mass slashing events. The honest summary: slashing is a real but small tail risk on ETH staking, and the day-to-day yield variation from network participation rates dwarfs the expected loss from slashing on any well-managed validator.

Compounding Your Earn Yield

Most exchange earn products distribute rewards daily, and most allow those rewards to compound automatically — the new tokens immediately start earning their own yield. The arithmetic of compounding is one of the few areas in personal finance where small numbers become large given enough time, and exchange earn is one of the easiest places to actually capture it.

A Worked Example

Suppose you start with £5,000 of USDT in Binance flexible savings at 4% APY, compounding daily, with no further deposits. After year one your balance is £5,204. After year five it is £6,107. After year ten it is £7,459 — almost a 50% increase from the original principal with no extra effort. The effective annual yield with daily compounding at a 4% nominal rate is 4.08%, slightly higher than the headline number because each day's reward earns its own micro-yield from the moment it lands.

Now add a £50 weekly DCA into the same earn balance and the trajectory changes meaningfully. Year one ends at around £7,830 (£5,000 starting + £2,600 deposited + £230 yield). Year five ends at around £20,500. Year ten ends at around £39,400. The DCA contribution dominates in early years and the compounding contribution catches up in later years. The dull-sounding "set up Auto-Subscribe and forget" workflow is genuinely the highest-leverage habit available to a small retail investor, because it converts attention you would have to spend manually moving rewards into yield you do not have to think about.

Compounding Cadence and Lock Periods

Exchange earn products differ in how often rewards compound. Binance Simple Earn flexible distributes daily and the new tokens immediately re-enter the same earn position the next day if Auto-Subscribe is on. Locked products often credit rewards to your spot wallet at the end of the lock period rather than re-staking automatically — meaning a 90-day locked product compounds only quarterly unless you re-subscribe by hand. This is one of the hidden reasons flexible products with auto-subscribe sometimes outperform locked products despite a lower headline rate: a flexible 4% with daily compounding can match a locked 4.5% with quarterly compounding once you account for the cadence difference, with no liquidity penalty.

The practical takeaway: when you compare earn products, do not just compare headline APY. Look at the compounding frequency, whether reinvestment is automatic, and whether the locked premium is large enough to outweigh the lost flexibility. For most beginner balances under £2,000, flexible products with auto-subscribe are the right default. The yield difference between 3% flexible and 4.5% locked over a year on a £1,000 balance is around £15 — not enough to justify accepting a 90-day liquidity restriction during a volatile market where the same balance could move 30% in a week, leaving you locked into a position you would otherwise have rotated out of and forfeiting more in opportunity cost than the entire annual yield premium ever paid.

CEX Earn vs DeFi: When to Graduate

Why Start with Exchange Earn

Why should you start with exchange earn? Because it removes all the complexity. You do not need a separate wallet. You do not pay gas fees. You do not need to understand smart contract calls. You cannot accidentally send tokens to the wrong address. The exchange handles validator management, reward distribution, and compounding for you. Your interface is simple: deposit, earn, withdraw.

For portfolios under £2,000, exchange earn is often your only practical option. Why? Because gas fees on Ethereum mainnet cost you £2-15 per transaction. If you stake £500 of ETH earning 3% APY (£15/year), paying £10 to stake and £10 to unstake wipes out your entire year's yield. Exchange staking has no gas fee overhead — all operations happen inside the exchange.

When to Move to DeFi

When should you move? Three conditions should be met before you graduate. First, your portfolio exceeds £2,000-5,000, so gas fees become a tiny fraction of your yield. Second, you know how to use a hardware wallet for self-custody. Third, you have spent 3-6 months with exchange earn, so you understand how rewards work and how yields change.

What does the DeFi graduation path look like? Beyond pure ETH staking, the broader DeFi ecosystem includes dApp governance tokens, NFT-collateralised lending, and yield-bearing wrappers that exchange earn products do not expose you to. Here are the main options you should explore:

- Liquid staking via Lido — stake ETH and receive stETH, a liquid token that earns staking yield while remaining tradeable and usable as collateral in DeFi. Our liquid staking guide covers this in depth.

- Lending via Aave or Compound — deposit USDT, USDC, or ETH into a lending protocol and earn interest from borrowers. Your yield comes from the same source as exchange savings products, but without the exchange commission. Our DeFi lending guide explains the process.

- Restaking via EigenLayer — restake your stETH to earn additional yield from securing middleware protocols. Higher yield but more complex risk. Our restaking guide covers the details.

- Yield optimisation via Pendle or Yearn — advanced yield strategies including yield tokenisation and auto-compounding. Our yield optimisation guide is the starting point.

Tax Implications for UK Investors

Staking Rewards as Income

HMRC treats cryptocurrency staking rewards and savings interest as income at the point you receive them. When you receive 0.001 ETH as a staking reward and ETH is worth £2,800 at that moment, you have £2.80 of taxable income. This income is subject to Income Tax at your marginal rate (20% basic, 40% higher, 45% additional). Does your exchange withhold tax for you? No. You are fully responsible for reporting this income on your Self Assessment tax return.

How should you track your staking income? Export your reward history from your exchange monthly. Binance provides a detailed earn history under Wallet → Earn → History. OKX provides similar reports under Assets → Earn → History. You must record the date, token, quantity, and GBP value of every reward. A crypto tax tool like Koinly can import your data automatically via API and calculate your total income across all exchanges and DeFi protocols.

Capital Gains on Reward Tokens

If you receive staking rewards and later sell those reward tokens at a higher price, you owe Capital Gains Tax on the appreciation above the income value. For example: you receive 0.01 ETH as staking rewards when ETH = £2,800 (income value = £28). You later sell that 0.01 ETH when ETH = £3,500 (disposal value = £35). Your capital gain is £7, which gets added to your annual CGT calculation. This creates a double taxation layer for you — Income Tax when you receive the reward, then CGT when you sell it — but each tax applies to a different part of the total value.

Your Capital Gains Tax allowance for 2025-2026 is £3,000. If your total crypto gains (including staking reward appreciation) stay under this threshold, you owe no CGT. For most beginners earning modest staking rewards on small balances, the CGT impact is minimal. It becomes significant if you accumulate rewards over several years and sell during a bull market. You should check your total gains annually to ensure you stay within your allowance.

Your First Earn Setup: A Quick Checklist

Ready to start earning? Here is what you should do today. The entire process takes under five minutes and you can undo it at any time by withdrawing back to your spot wallet.

- Check your spot wallet — do you have any idle BTC, ETH, or USDT that you plan to hold for at least 30 days?

- Navigate to Earn → Simple Earn on your exchange and look up the current flexible APY for your tokens

- Subscribe your idle tokens to flexible savings — you can withdraw at any time if you need them

- Enable Auto-Subscribe so your future DCA purchases automatically start earning yield

- Set a calendar reminder to check your earn rewards in 30 days and export the data for your tax records

You do not need to stake everything at once. Start with your USDT balance (lowest risk, simplest product). Once you see rewards appearing daily, move your ETH into flexible staking. After a month, you can evaluate whether locked staking makes sense for your situation. The important thing is to start today — even £50 of USDT earning 2% APY is better than £50 sitting idle in your spot wallet doing nothing for you.

Conclusion

Exchange earn products are the simplest way to generate yield on your cryptocurrency holdings without leaving the platform you already use for buying and selling. Flexible savings lets you earn 0.5-3% APY with full liquidity. Locked staking increases your yield to 2-7% APY in exchange for committing to a fixed term. Native staking on proof-of-stake tokens like ETH and SOL earns you real protocol rewards from validator participation in the blockchain consensus mechanism. Launchpool lets you farm new tokens with assets you already hold.

The key risks you should understand before staking: counterparty risk (if the exchange fails, you lose your staked tokens — remember FTX), lock-up risk (you cannot sell locked tokens during a market crash), variable APY (rates are not guaranteed and fluctuate with market conditions), and slashing risk on native staking (validators can be penalised for protocol violations). For amounts under £2,000, these risks are acceptable for most investors. For larger holdings, consider graduating to self-custody and DeFi protocols where you retain full control of your private keys.

Your action plan: start with flexible savings on your existing holdings today — it takes 60 seconds and you can withdraw at any time. Once you are comfortable, enable Auto-Subscribe so your DCA purchases automatically start earning. After 3-6 months, evaluate whether locked staking or native staking offers a meaningful yield improvement for your holding period. When your portfolio exceeds £2,000-5,000, explore our liquid staking guide and DeFi lending guide to begin your graduation from centralised earn to decentralised yield.

The honest framing for everything in this guide: exchange earn is a useful first step, not a destination. The yields are modest, the risks are real but manageable on small balances, and the operational simplicity makes it the right place to learn how staking and lending work without losing money to a misconfigured wallet or a fat-fingered transaction. As your portfolio grows past the threshold where exchange counterparty risk starts to dominate the yield calculation — somewhere between £2,000 and £5,000 for most beginners — the decision to migrate to self-custody and direct DeFi participation becomes the right one. Until then, the five-minute Auto-Subscribe setup is the highest-leverage thing you can do to your portfolio today.

For example, on a £1,500 USDT balance at 4% flexible APY, you earn approximately £60 per year — small in absolute terms but real, passive, and compounding. For example, on a £3,000 ETH staking position at 3% net APY, your annual yield is around £90 (plus any ETH price appreciation). For example, on a £500 starter balance split 70/30 between BTC flexible savings (1% APY) and ETH staking (3% APY), your combined yield in year one is approximately £8 — modest, but the infrastructure is in place for when your balance grows.

For example, after 12 months of weekly £25 DCA into ETH (cumulative £1,300) with Auto-Subscribe to staking at 3% net APY, your accumulated rewards are approximately £20. For example, doubling that to £50 weekly DCA brings the same period to £2,600 invested and roughly £40 in staking rewards. For example, on a £5,000 mixed portfolio (£3,000 ETH staked + £2,000 USDT flexible at 4%) your year-one yield reaches approximately £170 — at which point the £2,000 self-custody migration threshold becomes the next decision to make.

Sources and References

Frequently Asked Questions

- What APY can I expect from exchange staking?

- ETH staking on Binance and OKX yields approximately 2.5-3.5% APY after the exchange takes its commission. SOL staking yields 5-7% APY. USDT flexible savings pays 1-4% APY depending on market demand for borrowing. These rates fluctuate daily — you should always check the current rate before committing, and remember that the advertised APY is before the exchange deducts its commission (typically 10-25% of your rewards).

- Is exchange staking safe?

- Exchange staking carries counterparty risk — your crypto is held by the exchange, not in your own private key wallet. If the exchange becomes insolvent (as happened with FTX in 2022), you may lose your staked assets entirely. For amounts under £1,000-2,000, the convenience of exchange staking typically outweighs the risk for most beginners. For larger amounts, you should consider native staking via your own validator or a liquid staking protocol like Lido where you retain custody of your tokens.

- Do I pay tax on staking rewards in the UK?

- Yes. HMRC treats staking rewards as income at the point you receive them — you owe Income Tax based on the GBP value of each reward when it arrives in your account. If you later sell those reward tokens at a higher price, you also owe Capital Gains Tax on the appreciation above the income value. You should track the date, quantity, and GBP value of every reward for your annual Self Assessment return.

- What is the difference between flexible and locked staking?

- Flexible staking lets you withdraw your tokens at any time with no penalty — you earn a lower APY (typically 0.5-2% less) for this liquidity. Locked staking commits your tokens for a fixed period (30, 60, 90, or 120 days) in exchange for higher yield. If you need access to your funds during the lock period, you forfeit some or all accumulated rewards. You should use flexible for any tokens you might need to sell at short notice, and locked only for tokens you are committed to holding long-term regardless of price movements.

- Should I use exchange earn or DeFi protocols?

- Start with exchange earn products — they require no separate wallet setup, no blockchain gas fees, and no smart contract interaction risk. Once your portfolio exceeds £2,000-5,000 and you are comfortable with self-custody via a hardware wallet, consider graduating to DeFi protocols like Lido (liquid staking), Aave (lending), or EigenLayer (restaking). DeFi typically offers higher yields because you eliminate the exchange commission, but it adds complexity and requires you to manage your own security.

Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.