RWA Tokenisation Complete Guide

An honest map of real-world asset tokenisation in 2026: which tokenised treasuries, private-credit funds, tokenised real estate, and tokenised gold products are actually accessible to retail investors, what the AUM and yields are with date stamps, what the real risks look like (issuer, smart-contract, redemption, regulatory), and how to get on-chain exposure without confusing hype with substance.

What RWA Tokenisation Means in 2026

Real-world asset (RWA) tokenisation (also spelt tokenization in US English) is the on-chain representation of a legal claim on an off-chain asset — a US Treasury bill, a private-credit loan, a unit of fractional real-estate ownership, or an ounce of allocated gold sitting in a vault. The token itself is a programmable ERC-20 (or Solana SPL, or equivalent) that carries the economic rights of the underlying instrument: yield, principal, and redemption against the issuer.

By mid-2026, the live, retail-relevant slice of the RWA market is concentrated in four categories. Tokenised US treasuries lead — BUIDL (BlackRock's institutional money-market fund tokenised through Securitize) stands at approximately $2.37B AUM per rwa.xyz live snapshot as of June 2026 (down 11.67% over the prior 30 days), and Franklin Templeton's BENJI suite climbed to around $1.98B by 29 April 2026 across multiple chains. Tokenised private credit on Maple Finance and Centrifuge together account for roughly $3.7B in TVL (Maple ~$2.1B per DeFiLlama May 2026; Centrifuge ~$1.636B per DeFiLlama June 2026), with broader on-chain credit (Goldfinch, Clearpool, plus tokenised-credit assets like JAAA on rwa.xyz) extending the category into the high single-digit to low-teens of billions.

Tokenised real estate remains the smallest category in dollar terms and the most operationally risky. Tokenised gold, dominated by PAXG and XAUT, holds more than $5B in combined backing across the two leading issuers — PAXG at approximately $1.98B market cap (CoinGecko live snapshot, June 2026, against 456,894 PAXG circulating), and XAUT at $3.303B market value against 707,747 fine troy ounces per the 31 March 2026 BDO Italia attestation.

This guide maps the four categories with current numbers, explains how tokenisation actually works at the issuance, custody, oracle, and redemption layers, and gives an honest read on the risks — without pretending that every token is liquid, every issuer is solvent, or every regulator has signed off. Where a satellite guide goes deeper (treasuries, private credit, how-to-invest, gold-and-commodities), this hub points you to it; nothing is duplicated. Where a comparison page goes side-by-side on specific products (treasury wrappers, or PAXG vs XAUT), the link is in the relevant section.

Two practical things to keep in mind throughout. First, RWA AUM and yield figures move quickly; every number in this guide is date-stamped to give you a check against the live source. Second, jurisdictional access is the single most common reason a reader cannot actually buy something they read about — most institutional treasury wrappers gate by accredited-investor status, several issuers exclude US persons, and exchange availability varies. We flag access constraints in each category.

For context on why the category matters: the 2024-2026 window has been the period in which the largest TradFi asset managers moved from running pilots to running real product. BlackRock's BUIDL has crossed approximately $2.3B in AUM (PRNewswire, April 2026), Securitize crossed roughly $4B AUM under management by April 2026 and was selected by NYSE as a Designated Digital Transfer Agent for a tokenised-stock platform (with a SPAC IPO shareholder vote scheduled for 29 June 2026 per CoinDesk), and Sky (formerly MakerDAO, rebranded August 2024) now generates more than 60% of protocol revenue from RWA collateral with USDS at $7.9B market cap. These are the kind of structural facts that change how serious investors think about category risk; we use them throughout this guide as anchors, not as endorsements.

One framing note before we begin. The risk taxonomy in this guide treats the on-chain wrapper and the off-chain asset as two separate counterparty stacks that must each be evaluated. The strongest tokenised-treasury products combine a major TradFi issuer (BlackRock, Franklin Templeton, Invesco) with a regulated tokenisation infrastructure provider (Securitize, Ondo's stack, Franklin Templeton's in-house) and an audited on-chain token; the weakest products combine a thinly-capitalised SPV with a single-property real-estate exposure and an unaudited bridge wrapper. Read the issuer's filings the same way you would read a bond prospectus: the wrapper is the smaller of the two stories you need to understand.

What Is RWA Tokenisation

The shortest accurate definition is this: RWA tokenisation moves the ownership ledger of a real-world asset from a traditional registry — a bank's custody book, a fund administrator's transfer agent, a land registry — to a blockchain. The token on-chain is the unit of ownership, and the smart contract enforces the rules of transfer, allowlisting, and (where applicable) yield distribution.

Scope: what counts as RWA

In practice, "RWA" in 2026 refers to four broad categories of off-chain assets that have meaningful on-chain representation:

- Government securities — primarily short-duration US Treasuries and money-market fund shares. This is the largest and fastest-growing category, anchored by BUIDL, BENJI, OUSG, USDY, and the Invesco Short Duration US Government Securities Fund (formerly Superstate USTB).

- Private credit — overcollateralised and undercollateralised loans to vetted borrowers, structured as on-chain credit pools. Maple Finance and Centrifuge are the prominent platforms.

- Real estate — fractional ownership of residential or commercial property through an SPV that issues tokens against rental income and capital appreciation.

- Commodities — overwhelmingly gold (PAXG, XAUT), with smaller positions in silver, oil, and carbon credits.

What is generally not meant by "RWA" in current usage: tokenised equities (still pre-market for retail access in most jurisdictions, with NYSE's selection of Securitize as a tokenised-stock platform partner being one of the most credible 2026 signals); tokenised carbon credits and other ESG instruments (small, fragmented, and dominated by issuer-specific frameworks); and protocol-native synthetic assets that track real-world prices without holding real-world collateral.

Why this category matters in 2026

Three macro forces have pushed RWA from a niche experiment in 2022-2023 into a multi-billion-dollar live segment:

Yield reset. When US short-end rates climbed in 2022-2023, the gap between bank-deposit yields and DeFi-stablecoin yields collapsed, and tokenised T-bills opened a path to capture that yield without leaving on-chain rails. As of mid-2026, the US short end remains around 4-5%, which is competitive with most DeFi-lending yields on stablecoins.

Issuer-side maturity. The 2024-2026 window has seen BlackRock, Franklin Templeton, Invesco, and others move beyond pilots into substantive AUM. Securitize crossed approximately $4B in tokenised AUM under management by April 2026 and was selected as a Designated Digital Transfer Agent for NYSE, with a SPAC IPO shareholder vote scheduled for 29 June 2026 (CoinDesk). Sky (formerly MakerDAO) now generates more than 60% of protocol revenue from RWA collateral, according to The Token Dispatch's ecosystem coverage, with its USDS stablecoin reaching $7.9B market cap by March 2026.

Regulatory tailwinds outside the US. EU MiCA has provided a clear (if narrow) authorisation path for crypto-asset service providers, with the CASP transitional deadline of 30 June 2026 forcing the issue. Singapore, Hong Kong, and the UAE have each issued framework guidance for tokenised securities.

The US continues to be operationally complex, but the regulatory direction is engagement rather than blanket rejection — illustrated by the SEC closing its multi-year investigation of Ondo Finance without charges in November 2025 alongside Ondo's October 2025 acquisition of Oasis Pro Markets (SEC-registered broker-dealer, ATS, and transfer agent) to expand US tokenised-securities operations, and by BlackRock's 8 May 2026 SEC filings for two new tokenised fund products — an on-chain share class for the BlackRock Select Treasury Based Liquidity Fund (BSTBL, ~$7B AUM; SEC EDGAR CIK 97098) and the BlackRock Daily Reinvestment Stablecoin Reserve Vehicle (BRSRV, a blockchain-native tokenised MMF; SEC EDGAR CIK 844779), both separate from BUIDL — signalling product-by-product engagement.

The RWA Market Map 2026

The four-category split below uses verified AUM and TVL figures with date stamps. Every number changes weekly; treat the figures as a snapshot of mid-2026 conditions to anchor your search, not as live data.

Government securities (tokenised treasuries)

This is the largest live category and the cleanest fit for "yield without leaving on-chain rails". The headline products as of mid-2026:

- BUIDL (BlackRock USD Institutional Digital Liquidity Fund, tokenised by Securitize): approximately $2.37B AUM per rwa.xyz live snapshot as of June 2026 (-11.67% over the prior 30 days), making it the largest single tokenised-treasury product. Reg D for accredited investors only; chains include Ethereum, Polygon, Arbitrum, Avalanche, Aptos, Optimism, Solana (added March 2025 via Wormhole), and BNB Chain (added November 2025) — eight chains in total. In November 2025, BUIDL was accepted as off-exchange collateral on Binance (custody via Ceffu, Binance's crypto-native custody partner; banking triparty partners alongside) and launched a new share class on BNB Chain with cross-chain interoperability via Wormhole, broadening the addressable institutional base.

- BENJI (Franklin Templeton OnChain US Government Money Fund suite): approximately $1.98B AUM across the suite by 29 April 2026 (Franklin Templeton press release). Available on Stellar, Ethereum, Polygon, Solana, Aptos, Avalanche, Base, and Arbitrum. Retail access exists through certain wrappers and chains; verify the current product page for your jurisdiction.

- USDY (Ondo US Dollar Yield): approximately $740M token supply by Q1 2026 (Blockonomi / Altrady). Retail-accessible for non-US persons in supported jurisdictions, with redemption against US treasuries and bank deposits. USDY is not available to US persons by baseline Reg S structure (not a November 2025 change).

- OUSG (Ondo Short-Term US Government Bond Fund): approximately $1.1B+ TVL by Q1 2026 (Blockonomi / Altrady). Accredited and qualified institutional buyers only.

- Invesco Short Duration US Government Securities Fund (formerly Superstate USTB): tokenised under Superstate's prior structure, the fund continues to operate at meaningful AUM under the new Invesco wrapper, focused on short-duration US government securities. Verify current minimums and jurisdictional access on Superstate's product page.

For a side-by-side product comparison (issuer structure, redemption rails, supported chains, minimums, and accreditation status), see our tokenised treasury products comparison. For depth on the yield-versus-staking-versus-lending decision and the full Binance-corridor entry path that is independent of OKX, see our tokenised treasuries guide.

Private credit

The second-largest category by TVL and the most credit-sensitive. As of Q1 2026, total on-chain private credit sits around $5B (DEXTools / VaaSBlock), with the live retail-and-accredited-accessible share concentrated in two platforms:

- Maple Finance: approximately $2.1B TVL across Ethereum and Solana (DeFiLlama, May 2026). Maple operates pool-based credit to vetted borrowers; the Core Foundation lawsuit settled in mid-2026, and syrupBTC went live as part of Maple's product expansion. Maple's product set carries a real default history — the 2022 Orthogonal Trading default was the most material incident — which is part of the honest case for treating private credit as credit-risk-bearing yield rather than a treasury substitute.

- Centrifuge: approximately $1.636B TVL as of June 2026 (DeFiLlama), with deepest depth on Ethereum (~$1.25B) and growing footprints on Avalanche, Base, and Plume Mainnet. Centrifuge's pool structure brings real-world receivables on-chain through SPVs, with senior and junior tranches that let investors size their credit exposure explicitly.

- Goldfinch: the third name worth knowing for completeness, though its retail-accessible product set is narrower than Maple's or Centrifuge's. Goldfinch's reorganisation following its 2022-2023 default cycle is a useful case study in how an on-chain credit protocol updates its underwriting and pool structures after losses — covered in depth on our RWA private credit guide.

Real estate

The smallest live category in retail-accessible dollar terms and the one where the operational gap between marketing and reality is widest. Fractional-real-estate tokenisation platforms typically use an SPV structure: the SPV owns the property, issues tokens representing economic interest, and distributes rental income (after fees and reserves) to token holders.

Two practical caveats define the category. First, secondary liquidity is structurally thin — most platforms have order books that clear in tens of thousands of dollars per day per property rather than continuous markets. Second, issuer standing matters more here than in any other RWA category, because the SPV structure depends on operational and legal hygiene that has not always been present at every issuer. Readers should verify any tokenised-real-estate issuer against current legal filings before depositing.

For investors who want allocated exposure to real-world real estate through an on-chain wrapper, a more conservative path is often a tokenised real-estate fund (rather than single-property fractional tokens), and the realistic share of a portfolio for this category is typically small (single-digit percent) given the liquidity profile.

Commodities (gold-led)

Tokenised gold is the most retail-accessible commodity category and the most operationally mature. PAXG (Paxos Gold) and XAUT (Tether Gold) are the two dominant tokens, each backed by allocated gold held by an LBMA-accredited custodian and redeemable against the underlying bars (subject to minimums and fees that depend on the issuer's current terms). Smaller tokenised-gold products exist on Solana and other chains, but liquidity is concentrated in PAXG and XAUT.

The two leading tokens have different redemption mechanics, fee structures, and exchange-listing depth — covered head-to-head on our PAXG vs XAUT comparison. For the broader gold-and-commodities thesis (including silver, oil, and carbon-credit experiments), see our tokenised gold and commodities guide.

How Tokenisation Works

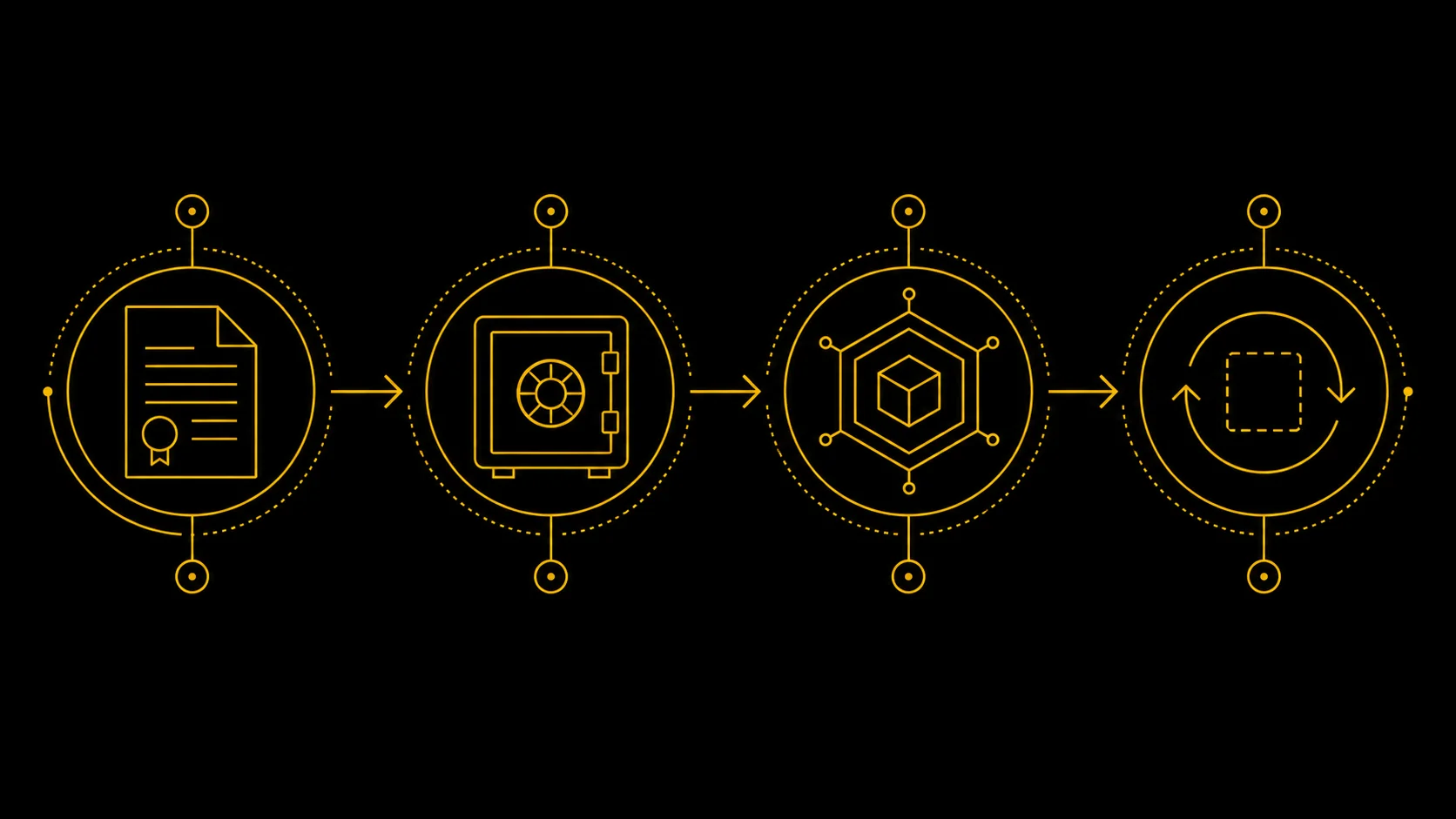

The mechanics differ in detail by category, but the lifecycle has four shared building blocks: issuance, custody of the underlying asset, oracle / accounting connection, and redemption. Understanding each block is what lets you read an issuer's documentation and tell a robust structure from a fragile one.

Issuance

Issuance is the legal act of creating the on-chain token and binding it to a specific real-world claim. For tokenised treasuries, this typically involves a regulated fund vehicle (a Delaware trust, a Luxembourg SICAV-RAIF, a Cayman-domiciled feeder fund) whose units are then represented on-chain by a smart contract. For tokenised real estate, the issuer creates an SPV that owns the property and issues equity-like tokens against the SPV's cap table. For tokenised gold, the issuer (Paxos for PAXG, TG Commodities Limited for XAUT) executes purchase of allocated gold and mints tokens against the holding.

The two questions worth asking about any issuer: who is the legal counterparty if you ever need to claim against the underlying asset, and what is that counterparty's regulatory standing in the jurisdiction where you live. A token's on-chain representation is only as useful as the legal claim it carries off-chain.

Custody of the underlying asset

The off-chain custodian holds the real-world asset and is the single most important counterparty risk in the structure. Major tokenised-treasury products use TradFi custodians of long-standing repute (BNY Mellon for BUIDL per Securitize disclosure, plus other tier-one TradFi custodians on the peer products); tokenised-gold products use LBMA-accredited vault operators (Brink's for PAXG); tokenised-real-estate SPVs use a mix of regulated trustees and law firms.

For DeFi-native users, the mental model adjustment is that custody risk now sits with a TradFi counterparty, not a smart-contract bug. That trade-off (better solvency profile, real-world legal recourse, vs. counterparty concentration risk) is the central feature of the category.

Oracle and accounting connection

The on-chain token has to know what the underlying asset is worth, and at what cadence. Three patterns are common:

- Net asset value (NAV) oracle: the issuer (or a regulated transfer agent) publishes NAV per share to an oracle contract, and the on-chain price updates accordingly. BENJI and BUIDL operate on this pattern, with daily or near-daily NAV strikes.

- Allocated-asset attestation: for tokenised gold, the issuer publishes regular attestations confirming the number of allocated ounces against tokens outstanding. PAXG publishes monthly independent third-party attestations listing bar serial numbers and vault locations; XAUT publishes quarterly attestations from BDO Italia — point-in-time balance verification rather than a full forensic audit.

- SPV cap-table sync: for tokenised real estate, the SPV's cap-table changes are reflected on-chain through allowlisted transfer functions, typically at quarterly or annual valuation cadence.

The oracle layer is where smart-contract risk and TradFi counterparty risk meet. A compromised oracle can lie about NAV; a delayed oracle can trigger unfair liquidations elsewhere in DeFi if the token is used as collateral; an off-chain attestation can be falsified by the issuer. Each product makes a different trade-off on transparency and frequency.

Reading an issuer's oracle design

The oracle block is where careful readers separate well-built products from fragile ones, because it determines how quickly the on-chain price reflects off-chain reality — and what happens when it cannot. Three questions do most of the work. First, cadence: a daily NAV strike (the BUIDL and BENJI pattern) means the token's on-chain price is at most a day stale in normal conditions, while a quarterly attestation (the tokenised-gold pattern) means the market price floats freely between publications and the attestation verifies backing rather than price.

Second, publication path: who signs the update, on which contract, and whether the publisher is the issuer itself, a regulated transfer agent, or an independent oracle network — each implies a different failure mode if the publisher halts. Third, behaviour under stress: when redemptions queue or the underlying market closes (US treasuries do not trade at the weekend; the token does), the oracle either keeps publishing the last good value, switches to an explicit stale flag, or lags silently. The first two are acceptable designs; the third is how depegs surprise holders.

None of this requires reading contract code. Every serious issuer documents its NAV or attestation mechanics, and the absence of that documentation is itself the finding. A practical habit before sizing any position: locate the oracle or attestation page, note the update cadence and the most recent timestamp, and decide whether that cadence matches how quickly you might need to exit. A product whose backing you can verify only quarterly belongs in a different mental bucket from one struck daily — even when both are honestly run — and the difference should show up in position size, not just in awareness.

Redemption

Redemption is what closes the loop. For tokenised treasuries, redemption is typically a T+0 or T+1 wire from the issuer against burnt tokens; minimums vary (BUIDL's redemption rails are calibrated for institutional flow, BENJI's retail wrappers redeem smaller). For tokenised gold, redemption is into either USD against burnt tokens or physical bars subject to allocation minimums (PAXG's physical redemption requires a multi-bar minimum; XAUT's process differs in detail). For tokenised real estate, redemption is the operational weak point — many issuers offer only secondary-market exit at depressed bids during stress windows.

The redemption-gate risk is one of the most common concerns honest reviewers raise about RWA. An issuer that pauses redemptions under stress effectively converts a liquid-looking token into an illiquid claim. Read the issuer's redemption pause and gate language carefully before sizing exposure.

Benefits vs Traditional Access

For investors weighing whether tokenised RWA is meaningfully different from buying the underlying asset through a brokerage, four advantages stand out — each accompanied by an honest caveat. The headline claim of the category is that programmable on-chain rails change the cost structure and the operational cadence of holding the underlying. Whether that change is material enough to motivate moving a particular position on-chain depends on which underlying, which jurisdiction, and which downstream use you want the holding to support. For a stablecoin-denominated saver who already operates on-chain, the answer is usually yes; for an investor whose flows live entirely in a brokerage account, the answer is often that the brokerage path is fine. Read the four points below as a framework for that judgement rather than as a universal endorsement.

24/7, programmable settlement

Tokenised assets transfer on the blockchain's schedule, not the issuer's business hours. A BUIDL transfer between two whitelisted addresses settles in minutes at any time of day. The settlement layer also exposes programmable hooks — you can write smart contracts that move RWA tokens conditional on price, time, or counterparty signature, which is genuinely new functionality compared with a brokerage account. The honest caveat is that allowlist controls in most regulated RWA tokens limit who you can send to, so the "programmable" property is bounded by the issuer's KYC perimeter.

Fractional and global access

A retail investor in a non-US jurisdiction can hold a fraction of a money-market-fund share through USDY without opening a US brokerage account; a saver in an EM-currency country can hold tokenised gold without navigating a domestic precious-metals dealer. For the categories where retail access exists (USDY, BENJI retail wrappers, PAXG, XAUT, some tokenised-real-estate platforms), the access barrier is meaningfully lower than the TradFi equivalent. The caveat is that "global access" still depends on the issuer's jurisdictional matrix — many retail-friendly products explicitly exclude the US and several other countries.

Composability with on-chain rails

A tokenised treasury that lives next to a stablecoin in the same wallet, on the same chain, is unusable as collateral, swap pair, or yield-strategy input in a way that a brokerage-held fund unit is not. Sky's RWA-backed revenue, which now exceeds 60% of protocol revenue per The Token Dispatch, is partly a consequence of this composability: tokenised treasuries flowing into Sky's vaults provide stable yield that backs USDS. Composability also matters for the settlement layer beneath all of this — Ethereum mainnet, Polygon, Arbitrum, and Base are now the most active venues for tokenised-treasury issuance, and the L2 settlement landscape continues to consolidate around a handful of chains (see our Ethereum L2 complete guide for the chain-by-chain picture). The caveat: composability adds layers of smart-contract risk that the brokerage account does not carry.

Yield without leaving on-chain rails

The single most pragmatic benefit. For an investor who already holds stablecoins on-chain, swapping into a tokenised treasury captures the underlying T-bill yield without converting back to fiat, paying brokerage fees, or waiting on settlement cycles. As of mid-2026, with the US short end around 4-5%, this is a directly comparable yield to a money-market fund without leaving the chain. The caveat is that the yield is taxable in most jurisdictions as soon as it accrues or is realised, and the token's value can still move with rate expectations even though the underlying yield is "risk-free".

A worked example: allocating $10,000 across the map

A concrete illustration makes the trade-offs visible. Take a non-US retail investor with $10,000 of stablecoin-denominated savings already sitting on-chain, and hold mid-2026 rates constant throughout. A defensible allocation across the market map might place $6,000 in a retail-accessible tokenised treasury product such as USDY (4.65% APY as of mid-2026, per Ondo's published rate), $2,000 in tokenised gold split between PAXG and XAUT as a non-yielding hedge, $1,000 in on-chain private credit through a retail wrapper — accepting advertised yields in the high single digits in exchange for genuine credit risk — and $1,000 held back in the stablecoin itself for gas, rebalancing, and redemption friction.

Run the arithmetic honestly and the blended yield lands at roughly 3.5%: about $279 a year from the treasury sleeve, perhaps $80-90 from the credit sleeve if no defaults bite, and nothing from the gold or cash positions. A conventional brokerage money-market fund would pay a similar headline rate with less operational overhead. The case for the on-chain version therefore does not rest on raw yield. It rests on the properties the previous subsections describe: settlement that runs at any hour, collateral that plugs directly into on-chain venues, jurisdiction-independent access for savers whose local banking rails are weak or expensive, and the option to compound, hedge, or redeploy without leaving the wallet.

The same example also shows where the structure punishes small accounts. Redemption minimums and network fees weigh proportionally heavier at $10,000 than at $1,000,000; the institutional products with the deepest liquidity (BUIDL, OUSG) are simply unavailable at this size because of accreditation gates; and a single private-credit default inside a $1,000 sleeve erases several years of its expected spread over treasuries. None of this argues against the category — it is the honest frame for sizing it. Treat the illustration as arithmetic, not advice: rates move, jurisdiction lists change, and the right split depends on circumstances no guide can see.

Risk Taxonomy

The honest map of RWA risk has six categories. This hub names each category and gives a one-paragraph mechanism; the satellite guides go deeper on product-specific and credit-specific risks (treasuries on Sat1, private credit on Sat2, operational and KYC on Sat3, gold on Sat4). Treat the six categories as a checklist when you evaluate any specific issuer.

Issuer risk

The TradFi entity behind the token (the fund, the SPV, the gold custodian) can become insolvent, commit fraud, or have its assets frozen. Major tokenised-treasury issuers (BlackRock, Franklin Templeton, Invesco) carry low headline issuer risk; smaller tokenised-real-estate platforms carry materially higher issuer risk and have, in past instances, faced legal disputes. This is the place to check primary-source filings and the issuer's regulatory standing in your jurisdiction.

The practical question for any specific issuer is whether the legal claim survives stress. A money-market fund unit held by BlackRock as transfer agent, custodied at BNY Mellon, with a Securitize-administered cap table, has a clear path of recovery even under issuer stress because the underlying assets and the custody chain are separate, regulated entities. A tokenised-real-estate token issued by an SPV whose sole asset is a single property and whose operational hygiene is uncertain is a fundamentally different counterparty profile, even if the token contract and the SPV documents look superficially similar. Reading the difference is the work that protects sized exposures.

Smart-contract risk

The on-chain token, plus any bridge, wrapper, or DeFi protocol you route through, can be exploited. A recent verified example: in April 2026, Kelp DAO suffered a roughly $292M bridge exploit attributed to the North Korean Lazarus Group, in which attackers minted roughly 116,500 unbacked rsETH; Kelp completed operational recovery in May 2026, with withdrawals reopened on 14 May and rsETH backing restored above 100% by late May (The Block and Kelp DAO disclosure). The full arc of the Kelp incident is the point — the exploit happened, the protocol recovered, and the underlying RWA collateral on Kelp was not impaired. Smart-contract risk is mitigated by limiting layers (use first-party issuer rails where possible, not wrappers-of-wrappers) and by sizing each layer's exposure to what you can afford to lose.

Regulatory risk

Jurisdictional engagement can shift. In November 2025, the SEC closed its multi-year investigation of Ondo Finance without charges; Ondo's October 2025 acquisition of Oasis Pro Markets (SEC-registered broker-dealer, ATS, and transfer agent) expanded rather than withdrew its US tokenised-securities footprint. USDY's exclusion of US persons is its baseline Reg S structure, not a November 2025 change. EU MiCA's CASP transitional deadline of 30 June 2026 will force several non-authorised CASPs out of the EU market unless they complete their applications. In the UK, HMRC's framing of tokenised-RWA disposals (post-30 October 2024 budget rates of 18% basic and 24% higher) applies the same way it does to other crypto. Regulatory risk is the category that changes fastest; check the issuer's current jurisdictional notice before sizing.

Liquidity risk

Secondary-market depth varies by product. Tokenised treasuries with active redemption rails (BUIDL, BENJI, USDY) tend to have shallow secondary order books, because most flow goes through primary mint and redeem; this is fine in normal markets but means the price can dislocate from NAV during stress. Tokenised real estate has structurally thin secondary books almost by design. Tokenised gold (PAXG, XAUT) has the deepest secondary liquidity in the RWA universe, listed on most major CEXs and several DEXs.

Depeg risk (NAV deviation)

For tokenised assets whose on-chain price is expected to track an off-chain reference (NAV per share, USD value of allocated gold), the gap between on-chain price and reference can open under stress. PAXG and XAUT have been remarkably tight to spot gold but have shown small premia and discounts during high-volatility windows. Tokenised treasury tokens with NAV-oracle pricing can show short-lived dislocations if the oracle update lags rapid moves in the short end.

Redemption-gate risk

Issuers can pause redemptions under stress, converting a liquid-looking token into an illiquid claim. Every regulated RWA issuer reserves the right to gate; the terms vary materially. This is the single most important fine-print item to read on any issuer's product page before depositing meaningful size.

The history of redemption gating in adjacent markets is instructive. UK property funds gated redemptions through the 2016 and 2020 stress windows, money-market funds in the US briefly approached the same problem during the 2020 dash-for-cash, and several CeFi crypto-lending platforms froze withdrawals through the 2022 cycle. The on-chain wrapper does not change the underlying liquidity profile of the asset; it changes the speed at which the wrapper can be repriced. A tokenised-treasury fund that gates redemptions for a week still leaves you holding what is, in substance, a one-week-illiquid claim, regardless of what the on-chain price screen says.

Regulation Landscape

RWA tokenisation lives at the intersection of securities law, money-transmission law, and crypto-asset-service-provider frameworks. The jurisdiction-by-jurisdiction picture as of mid-2026 looks like this.

European Union — MiCA

The Markets in Crypto-Assets regulation (MiCA) frames most retail-facing tokenised products as crypto-asset services, with a transitional period for CASP authorisation ending on 30 June 2026 — the final EU-wide deadline confirmed by ESMA, with many member states having adopted shorter national windows. Tokenised securities that meet the test of a "financial instrument" under MiFID II fall outside MiCA and into the existing securities regime instead — most tokenised treasuries and tokenised-private-credit products structured as fund units sit there. The practical reading for a non-EU reader is that EU-targeted products (BENJI retail wrappers, USDY in supported EU jurisdictions) are increasingly accessible through MiCA-authorised intermediaries, with the CASP transitional deadline pushing the remaining grey-area issuers either into authorisation or out of the EU market.

United States — SEC posture and Ondo signal

The US regulatory posture in mid-2026 is best read as case-by-case engagement rather than blanket position. The signal that matters most is BlackRock's 8 May 2026 SEC filings for two new tokenised fund products (BSTBL on-chain share class and BRSRV blockchain-native MMF, per SEC EDGAR — both separate from BUIDL), alongside the Securitize SPAC IPO vote on 29 June 2026 and Securitize's selection by NYSE as a Designated Digital Transfer Agent for a tokenised-stock platform. Each of these is a meaningful operational engagement between major US institutions and the SEC on the practical mechanics of tokenised securities — a level of engagement that was absent eighteen months earlier.

Against that, the Ondo Finance episode is the realistic counterweight: the SEC investigation into Ondo closed in November 2025 with no charges filed, and Ondo completed its October 2025 Oasis Pro Markets acquisition (SEC-registered broker-dealer, ATS, and transfer agent) to expand US tokenised-securities operations. The product access split remains: OUSG stays gated to US qualified purchasers and accredited investors under Reg D, and USDY is structured under Reg S for non-US persons rather than offered to US retail — both baseline structures, not changes. The takeaway for US retail readers: most retail-friendly tokenised-treasury products do not currently take US customers, and the institutional-grade US-accessible products (BUIDL, OUSG for accredited and qualified institutions) sit behind Reg D / Reg S structures.

United Kingdom — HMRC framing

HMRC's Cryptoassets Manual frames tokenised RWA disposals as standard chargeable disposals for Capital Gains Tax. Following the 30 October 2024 budget, CGT rates on disposals made on or after that date are 18% (basic-rate band) and 24% (higher- and additional-rate bands), against the 2024/25-onwards £3,000 annual allowance. Yield received in stablecoins or additional tokens is generally treated as miscellaneous income at the GBP value on the day of receipt. The FCA's cryptoasset registration regime (under MLR 2017) applies to UK-domiciled service providers; tokenised securities fall under the existing FSMA perimeter and FCA permissions where relevant. For a deeper read of the UK CGT framing applied to crypto, see our crypto taxes guide.

Custody and Security

RWA tokens are still on-chain tokens. The custody question splits into two layers: the off-chain custody of the underlying asset (which is the issuer's responsibility) and the on-chain custody of the token (which is yours).

For the off-chain side, the relevant questions are who holds the underlying, what their regulatory standing is, and what the attestation cadence looks like. Tokenised treasuries leverage TradFi custodians with long-established reporting; tokenised gold uses LBMA-accredited vaults with regular attestations; tokenised real estate sits behind SPV trustees and depends on the SPV's operational hygiene.

For the on-chain side, you control the wallet that holds the token, and the same self-custody principles that apply to any other ERC-20 apply here. For meaningful position sizes, a hardware wallet is the standard recommendation — it isolates the signing key from network-connected devices, which materially reduces the surface area for phishing and malware-driven theft.

One operational note worth flagging for hardware-wallet users. In January 2026, Ledger disclosed a third-party data leak via its e-commerce partner Global-e, which exposed order data (names and contact details) for Ledger customers who purchased through Ledger's online store. The hardware self-custody design is unaffected — no private keys or wallet funds were accessed — and the underlying hardware-wallet model remains the right tool for significant on-chain holdings. The relevant user action is to treat all unsolicited "Ledger support" or "Global-e" communications as suspicious and to verify through Ledger's official channels (CoinDesk and Ledger incident notice).

How to Get Exposure

The high-level path from fiat to a tokenised RWA position has four steps:

- Step 1 — exchange: use a centralised exchange to convert fiat into a stablecoin (USDC or USDT) or directly into the target RWA token where the exchange lists it.

- Step 2 — wallet: withdraw to a self-custody wallet (software wallet for smaller positions; hardware wallet for meaningful size).

- Step 3 — product: bridge or swap into the chosen RWA token, either directly on a CEX that lists it, on a DEX, or through the issuer's primary mint rails if you are accredited or qualified.

- Step 4 — monitor: track yield, NAV, redemption windows, and any issuer notices. Tokenised RWA is not "set and forget"; the regulatory and operational layer moves.

The step-by-step instructions, jurisdictional matrix, and KYC pathways for each retail-relevant RWA product are covered in our how to invest in RWA guide, which carries the single source of truth on jurisdiction and KYC for the cluster.

Entry venue — exchange corridor

For non-US retail investors looking for a one-stop entry venue with broad asset support, deep stablecoin rails, and an established Earn-and-Web3-wallet stack, OKX is one of the most widely used corridors into the on-chain RWA universe. OKX lists most of the stablecoin and bridge tokens needed for the RWA market map above, supports withdrawal to self-custody wallets on Ethereum and several L2s, and operates a Web3-wallet product that integrates with the chains where major RWA issuers operate.

In February 2025, OKX's parent entity Aux Cayes FinTech pleaded guilty to operating an unlicensed money-transmitting business in the US and paid $504.4 million in penalties to the US Department of Justice (CNBC, 24 February 2025); the exchange operates under a three-year independent compliance monitorship through 2027. The settlement does not bar OKX from operating in non-US jurisdictions, and the exchange continues to be widely used by non-US retail and institutional traders. Verify your jurisdiction's eligibility on OKX directly before signing up.

For US-eligible flows, the picture is materially different — domestic venues carry their own listings and constraints, and most retail-facing tokenised-treasury products do not currently take US customers at all. The how-to-invest guide walks through the realistic US options.

Outlook

Three institutional signals are worth tracking through the rest of 2026 and into 2027, in roughly the order of how concretely they have moved.

BlackRock's product expansion. BUIDL at approximately $2.37B AUM (rwa.xyz live, June 2026), plus BlackRock's 8 May 2026 SEC filings for two sibling tokenised funds (BSTBL on-chain share class and BRSRV blockchain-native MMF, per SEC EDGAR) and the November 2025 Binance integration (Ceffu custody and Wormhole interoperability), points to a continued shift from pilots to mainstream institutional product. The reasonable read is not that BlackRock will single-handedly dominate the category, but that the largest asset manager in the world is making operational commitments that anchor the regulatory conversation around a familiar counterparty profile.

Securitize's SPAC IPO and NYSE partnership. Securitize crossed approximately $4B AUM under management by April 2026 and was selected by NYSE as a Designated Digital Transfer Agent for a tokenised-stock platform; the SPAC IPO shareholder vote is scheduled for 29 June 2026 (CoinDesk). If the vote passes and the listing proceeds, Securitize becomes the first listed pure-play tokenisation-infrastructure company, which is the kind of structural signal that materially changes how institutional allocators think about category risk.

Sky's RWA share of revenue. Sky (formerly MakerDAO) now generates more than 60% of protocol revenue from RWA collateral (The Token Dispatch), and USDS reached $7.9B market cap by March 2026. This is the strongest single signal that on-chain protocols are using tokenised RWA as a real source of yield-bearing collateral rather than as a marketing experiment. It also means that the largest decentralised stablecoin in active use is now substantially backed by tokenised real-world assets — a structural fact worth keeping in mind when reading about stablecoin reserves.

Three things to keep in mind about the outlook. First, AUM growth is not the same as broader retail access — most institutional products remain accredited-investor-only. Second, the regulatory perimeter is still uneven by jurisdiction; the global picture in mid-2027 may look quite different from where it sits today, in either direction. Third, smart-contract risk does not disappear as the category scales; it changes shape (more sophisticated bridge architectures, more layered DeFi integrations, larger AUM at stake per exploit). The Kelp DAO bridge exploit in April 2026 is a recent reminder that the LRT / bridge layer is the most attacked surface in adjacent on-chain markets, even when the underlying collateral is sound.

A fourth signal worth watching is the cadence at which non-US regulators issue clarifying guidance. EU MiCA's CASP transition completes on 30 June 2026; the UK FCA's broader cryptoasset framework continues to evolve through 2026; Singapore's MAS and Hong Kong's SFC have each issued specific guidance on tokenised securities in the past twelve months. The competitive pressure from non-US jurisdictions issuing clearer rules tends to push US-domiciled issuers to either localise their products (BUIDL on multiple chains, BENJI in retail wrappers in supported jurisdictions) or to localise via US-licensed acquisitions while continuing global operations (the Ondo path — October 2025 Oasis Pro Markets acquisition expanded US capability rather than withdrew it). Watching where new product launches happen first, and where they choose not to launch, is often a more honest signal of the regulatory trajectory than reading press statements.

A final, narrower technical signal: the depth and concentration of tokenised-treasury holdings within DeFi-protocol collateral pools. Sky's RWA share of revenue (more than 60% per The Token Dispatch) is the most quoted example, but several smaller protocols are beginning to accept tokenised treasuries as collateral for stablecoin issuance or for permissioned lending pools. If that trend continues, tokenised treasuries become the backing of a meaningfully larger share of on-chain stablecoin supply, which both increases the category's structural importance and concentrates a new form of TradFi-to-DeFi linkage risk that did not exist at scale eighteen months earlier.

Conclusion

RWA tokenisation is no longer hypothetical. As of mid-2026, the four-category map is live and measurable: tokenised treasuries hold the largest AUM (BUIDL ~$2.37B per rwa.xyz live June 2026, BENJI ~$1.98B, plus the OUSG / USDY / Invesco Short Duration set), tokenised private credit anchors the second-largest category (Maple ~$2.1B TVL, Centrifuge ~$1.636B per DeFiLlama, with broader on-chain credit extending into the high single-digit to low-teens of billions), tokenised gold provides the deepest retail-accessible commodity exposure (PAXG ~$1.98B mcap per CoinGecko June 2026 and XAUT $3.303B per Q1 2026 attestation; collectively over $5B in backing), and tokenised real estate remains the smallest live retail-relevant category and the highest-risk operationally.

For an investor deciding whether to allocate to RWA, the practical reading is this. The yield case for tokenised treasuries is straightforward when the US short end is around 4-5%: capture the underlying T-bill yield on-chain, without leaving the stablecoin rails you already use, with redemption against a regulated TradFi issuer. The yield case for tokenised private credit adds real credit risk and requires reading the issuer's default history honestly; Maple's 2022 Orthogonal default and the category's wider 2022-2023 default cycle are part of that honest reading. Tokenised gold is a legitimate retail-accessible substitute for an allocated-bullion position, with deeper secondary liquidity than the rest of the RWA universe. Tokenised real estate is the category where the gap between marketing and operational reality is widest, and where caution scales with position size.

Three things matter more than picking any specific product. First, jurisdictional access — most retail-friendly products exclude the US, several exclude additional countries, and the matrix changes; verify before depositing. Second, smart-contract layering — every wrapper, bridge, and DeFi integration you add multiplies risk, and the April 2026 bridge exploit discussed above — and its May 2026 recovery — shows what that risk looks like in practice. Third, redemption mechanics — the difference between a token that redeems T+0 against a major TradFi custodian and a token that promises redemption "subject to market conditions" is the difference between a treasury substitute and an illiquid claim.

For the next concrete step into the category, two paths exist. If you want product-by-product depth on tokenised treasuries — the largest category — and the realistic Binance-corridor entry path, the tokenised treasuries satellite guide in the Related Articles section below is the next read. If you want the operational step-by-step (exchange, wallet, jurisdiction, KYC) before you commit any capital, the how-to-invest satellite handbook is also listed there. Either route, treat AUM and yield figures as live and check the primary source before sizing.

A final note on portfolio context. Treating RWA as a single allocation category is usually wrong. Tokenised treasuries behave like a stablecoin substitute with yield — they belong in the cash sleeve of a portfolio, not the risk-asset sleeve, and they should be sized against the function of that sleeve (liquidity buffer, denominator for option strategies, on-chain earnings rail). Tokenised private credit behaves like a high-yield credit position with material default risk and limited secondary liquidity; it belongs in a credit sleeve and should be sized at the level you would size a similar TradFi private-credit allocation.

Tokenised gold behaves like physical gold with an on-chain wrapper; size it the way you would size a precious-metals position. Tokenised real estate, where you decide to hold it at all, should be sized at the level you would size an illiquid private-market position. Conflating these four into a single "RWA" bucket is the single most common mistake in initial allocations.

Sources and References

The figures and events cited in this guide draw on primary issuer announcements, regulator filings, and tier-one financial press. Live AUM and TVL figures change quickly; check the primary source for the current value.

- BUIDL accepted as Binance collateral; BNB Chain launch (PRNewswire, 14 November 2025) — Ceffu off-exchange custody, Binance triparty banking partners, Wormhole interoperability

- BlackRock 8-K exhibit (SEC EDGAR) — disclosure underpinning the BUIDL $2.3B AUM figure

- Franklin Templeton BENJI suite ~$1.98B AUM (29 April 2026) — Stellar-anchored release, multi-chain availability

- Maple Finance TVL (DeFiLlama) — live TVL for Maple's onchain private-credit pools

- Securitize SPAC IPO and NYSE partnership (CoinDesk) — June 2026 vote schedule and NYSE Designated Digital Transfer Agent selection

- OKX parent Aux Cayes FinTech DOJ settlement (CNBC, 24 February 2025) — $504.4M penalty and three-year independent compliance monitorship through 2027

- Ledger Global-e third-party data leak (CoinDesk, 5 January 2026) — order-data exposure, hardware self-custody unaffected

- Kelp DAO and Aave rsETH recovery after the April 2026 exploit (The Block) — $292M exploit attribution and May 2026 operational recovery

- ESMA MiCA CASP register and transitional period — official EU regulator portal

- HMRC Cryptoassets Manual — UK CGT and miscellaneous-income framing for tokenised assets

- Sky's RWA-driven revenue model (The Token Dispatch) — RWA share of Sky protocol revenue at roughly 60%

Disclaimer: Cryptocurrency and tokenised real-world assets carry significant risk, including total loss of capital. This guide is for educational purposes only and does not constitute financial, legal, or tax advice. AUM, TVL, and yield figures are point-in-time references; verify against the primary source before making allocation decisions. Always consult a qualified professional for advice specific to your jurisdiction.

Frequently Asked Questions

- What does RWA tokenisation mean in 2026?

- RWA tokenisation (also spelt tokenization) wraps a claim on a real-world asset — a US Treasury bill, a private-credit loan, a square metre of an office block, an ounce of allocated gold — into a programmable on-chain token. As of mid-2026, the largest live category is tokenised US treasuries: BUIDL (BlackRock) at around $2.37B AUM (rwa.xyz live snapshot, June 2026; -11.67% over the prior 30 days) and the BENJI suite (Franklin Templeton) at roughly $1.98B AUM (Franklin Templeton press release, 29 April 2026). Tokenised private credit on Maple Finance sits near $2.1B TVL (DeFiLlama, May 2026), and the four leading retail-accessible tokenised-gold products together hold over $1B in backing.

- Is RWA tokenisation only for institutions, or can retail investors participate?

- Both. Most institutional treasury products (BUIDL, OUSG, Invesco Short Duration US Government Securities Fund — formerly Superstate USTB) are gated to accredited or qualified investors under Reg D / Reg S structures. A growing retail tier exists: USDY (Ondo) is open to non-US retail in supported jurisdictions, the BENJI suite extends to retail wrappers via Stellar and other chains, and tokenised gold (PAXG, XAUT) is retail-accessible globally on most centralised and decentralised exchanges. Always check the issuer's current jurisdictional matrix before depositing.

- What is the difference between a tokenised treasury and a stablecoin?

- A stablecoin (USDC, USDT, USDS) targets a $1 peg and typically pays no yield to the holder. A tokenised treasury token represents a share in a money-market or T-bill fund and pays the underlying yield (around 4-5% as of mid-2026, depending on the US short-end curve). Tokenised treasuries also carry redemption mechanics that differ from stablecoins: most products redeem T+1 or T+0 against the issuer rather than swapping freely on DEXs at peg.

- What are the biggest risks of holding tokenised real-world assets?

- Five categories: issuer risk (the underlying is custodied by a TradFi entity, so issuer insolvency or fraud impairs recovery); smart-contract risk (the on-chain token can be exploited — Kelp DAO's April 2026 $292M bridge exploit is a recent verified example, although Kelp completed operational recovery in May 2026 with backing restored above 100% by late May); redemption-gate risk (issuers can pause redemptions under stress); regulatory risk (jurisdictional engagement can shift in either direction — in November 2025 the SEC closed its multi-year Ondo investigation without charges, while Ondo's October 2025 Oasis Pro Markets acquisition expanded US tokenised-securities operations); liquidity risk (secondary-market depth varies and discounts can open during stress).

- How does tokenised real estate work, and is it actually liquid?

- Tokenised real estate uses an SPV or trust structure that owns the physical property and issues tokens representing fractional economic interest. Rental income flows through the SPV to token holders, typically in a stablecoin. Secondary liquidity is the honest weakness: most tokenised-real-estate platforms have thin order books, redemption windows tied to the SPV's quarterly or annual valuations rather than continuous markets, and several issuers carry active legal disputes. Retail investors should treat tokenised real estate as illiquid and verify each issuer's standing before depositing.

- What did Ondo Finance's November 2025 SEC investigation closure and October 2025 Oasis Pro Markets acquisition actually mean?

- In November 2025, the SEC closed its multi-year investigation of Ondo Finance without filing charges. Separately, Ondo completed its acquisition of Oasis Pro Markets — an SEC-registered broker-dealer, ATS, and transfer agent — on 6 October 2025, expanding US tokenised-securities operations rather than withdrawing from them. USDY remains structured under Reg S (excludes US persons; baseline since launch) and OUSG remains gated to US accredited investors and qualified purchasers under Reg D (baseline since launch). The realistic regulatory perimeter for tokenised treasuries in the US is one in which Ondo continues to operate and expand US-facing capability.

- How is RWA tokenisation taxed for UK residents?

- HMRC treats tokenised RWA disposals like any other crypto disposal: a sale, swap, or spend triggers a Capital Gains Tax event. Following the 30 October 2024 budget, CGT rates on disposals made on or after that date are 18% (basic-rate band) and 24% (higher- and additional-rate bands), against a £3,000 annual allowance for 2024/25 onwards. Yield received in the form of a stablecoin or additional tokens is generally treated as miscellaneous income at the GBP value on the day of receipt. Always check HMRC's Cryptoassets Manual for the latest position.

- What is the smart contract risk of holding tokenised treasuries on-chain?

- The smart-contract risk sits in two places: the on-chain token itself (transfer logic, allowlist controls, pause functions) and any DeFi protocol or bridge you route through. Major issuers (BlackRock, Franklin Templeton, Ondo) use audited contracts with allowlists that restrict transfers to whitelisted addresses, which reduces composability but limits attack surface. If you use third-party wrappers, bridges, or yield strategies layered on top of a tokenised treasury, you inherit each layer's risk — a point underscored by the April 2026 bridge-exploit episode.

- Which exchange should I use to access RWA tokens?

- For non-US retail investors looking for a one-stop entry venue with broad access to RWA-adjacent tokens and on-chain rails, OKX is one of the most widely used corridors. Note that OKX's parent entity, Aux Cayes FinTech, settled with the US Department of Justice in February 2025 (a $504.4M penalty for unlicensed money transmission) and operates under a three-year independent compliance monitorship through 2027 — verify your jurisdiction's eligibility on OKX directly. For US-eligible flows, domestic venues carry their own constraints; our step-by-step guide handles the jurisdictional matrix in detail.

- What is Sky's role in the tokenised real-world-asset market?

- Sky (formerly MakerDAO, rebranded August 2024) generates most of its protocol revenue from real-world-asset collateral — more than 60% of Sky's revenue comes from RWA exposures, according to The Token Dispatch's ecosystem coverage. Sky's USDS stablecoin (the upgraded successor to DAI) reached a $7.9B market cap by March 2026. RWA collateral on Sky includes tokenised treasury products and short-duration credit, channelled through Spark (the lending market within the Sky ecosystem).

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.