How to Buy Bitcoin: Beginner Guide

A practical guide to buying Bitcoin safely — exchange selection, payment methods, security and self-custody storage. Step-by-step instructions for beginners and a clear path to advanced topics.

Introduction

Buying Bitcoin in 2026 is dramatically easier than it was even five years ago. Regulated exchanges, comprehensive insurance coverage, recurring-buy automation and well-developed mobile apps make Bitcoin accessible to mainstream investors worldwide. The January 2024 approval of US spot Bitcoin ETFs added a third pathway alongside direct exchange purchases and self-custody.

The accessibility improvement matters because the obstacles that prevented mainstream Bitcoin adoption for over a decade — confusing exchange interfaces, opaque fee structures, weak regulatory oversight, custody risk on the platforms holding the assets — have been substantially addressed. The 2022 collapses of FTX, Celsius, BlockFi and Voyager removed the worst-quality platforms from the market, and the survivors operate under regulatory frameworks that simply did not exist before 2024. The institutional infrastructure that ETFs and proof-of-reserves audits have built means a first-time buyer in 2026 faces lower operational risk than at any prior point in Bitcoin's history.

This guide walks through the practical steps of buying your first Bitcoin safely. Three pathways serve most retail investors:

- Centralised cryptocurrency exchanges — direct Bitcoin purchases via OKX, Coinbase, Kraken or similar. The most flexible path for direct ownership and recurring DCA.

- Spot Bitcoin ETFs — through standard brokerage accounts (Fidelity, Schwab, Vanguard in the US; Hargreaves Lansdown, IG, Trading 212, AJ Bell in the UK). Best for retirement accounts and tax-advantaged wrappers.

- Bitcoin ATMs and P2P platforms — convenient for small cash purchases or specific privacy needs but charge premium fees.

This guide focuses primarily on the centralised exchange path because it is the most flexible and offers the best fee economics for most retail buyers. The ETF and alternative paths are covered in summary, with cross-links to dedicated guides for the detailed decision frameworks.

One framing point before we start. Most first-time Bitcoin buyer mistakes are not about choosing the wrong exchange or paying slightly higher fees than necessary. They cluster around three operational failures: leaving Bitcoin on the exchange too long after purchase, overlooking 2FA or seed phrase backup until after a phishing attempt or device failure, and falling for "support staff" social engineering that targets new buyers specifically. The exchange selection matters but matters less than the operational discipline you build in the first weeks after your first purchase. We cover the exchange selection thoroughly because it is the natural starting point, but we want you to take away from this guide a framework for ongoing operational discipline rather than a one-off purchase walkthrough.

By the end of this guide you should be able to make your first Bitcoin purchase in under 30 minutes on whichever platform fits your jurisdiction, with clear next steps for moving funds to self-custody once your holdings exceed the threshold where exchange custody risk becomes meaningful.

Why Buy Bitcoin?

Bitcoin remains the world's most adopted cryptocurrency and the dominant digital store-of-value asset. As digital assets have moved from experimental to mainstream, Bitcoin has cemented its role as "digital gold" — a scarce, programmable monetary asset that can be self-custodied without intermediaries.

The investment case for Bitcoin combines several structural properties:

- Hard-capped supply — only 21 million BTC will ever exist; current new issuance is approximately 0.85% per year and decreasing through halvings

- Institutional adoption — spot ETFs, corporate treasury holdings (MicroStrategy and others), sovereign exposure (El Salvador adopted Bitcoin as legal tender in 2021, then made acceptance voluntary in 2025 under an IMF loan condition; it still holds BTC in its treasury)

- Network resilience — over 17 years of operation through multiple market cycles, regulatory pressures and technical challenges without protocol-level failure

- Self-sovereign property — direct ownership without bank or custodian intermediaries

For background on Bitcoin's technology, history and value proposition, see our complete Bitcoin guide. For the broader Bitcoin investment framework, see our Bitcoin investment fundamentals hub.

Best Places to Buy Bitcoin

The right exchange depends on your jurisdiction and experience level. Three exchanges serve the majority of retail buyers across markets.

Exchange comparison

| Exchange | Trading Fee | Payment Methods | Best For |

|---|---|---|---|

| OKX | 0.08-0.10% | Bank transfer, card, P2P | Global, incl. US spot via OKX US (some states excluded) — lowest fees, deep liquidity |

| Coinbase Advanced | 0.4-0.6% | Bank transfer, debit card, ACH | US beginners — most polished UX, regulated |

| Kraken | 0.25-0.40% (base tier) | Bank transfer, debit card | US and international — strong security record |

Geographic note: OKX launched a US platform (OKX US) in April 2025, offering spot trading in most US states — though it is spot-only (no derivatives or Web3 features) and excludes several states. For most US beginners, Coinbase or Kraken remain the simplest fully-regulated options. Outside the US, OKX offers the lowest fees and deepest BTC liquidity.

OKX — primary recommendation outside the US

OKX is a leading global cryptocurrency exchange with strong fundamentals for Bitcoin purchases:

- Amongst the lowest spot trading fees in the industry (0.08-0.10% maker/taker, lower with volume tiers)

- Deep BTC liquidity and tight spreads on major pairs

- Bank transfer, card and P2P payment methods

- Recurring-buy automation for DCA strategies

- Proof-of-reserves audited monthly; strong custody track record

- Integrated Web3 wallet for users who want to bridge into broader crypto activity

Coinbase — easiest entry for US beginners

Coinbase is the default choice for first-time US buyers:

- Extremely user-friendly interface, well-suited to first-time crypto purchasers

- Excellent customer support and educational resources

- Fully regulated in the United States; publicly listed (NASDAQ: COIN)

- Insurance coverage for digital assets in hot wallets

- Coinbase Advanced offers materially lower fees (0.4-0.6%) than the simple buy flow (~1.49%)

- Coinbase One ($29.99/month) waives trading fees on eligible buys up to a monthly volume cap, though the quoted-price spread still applies

Kraken — strong security pedigree, US and international

Kraken is the leading choice for security-focused US investors and a strong international option:

- One of the longest operating-history exchanges; never been hacked at the platform level

- Strong regulatory compliance across major jurisdictions

- Lower fees than Coinbase Advanced for most volume tiers

- Professional trading interface (Kraken Pro) for advanced users

- Proof of reserves and transparent custody practices

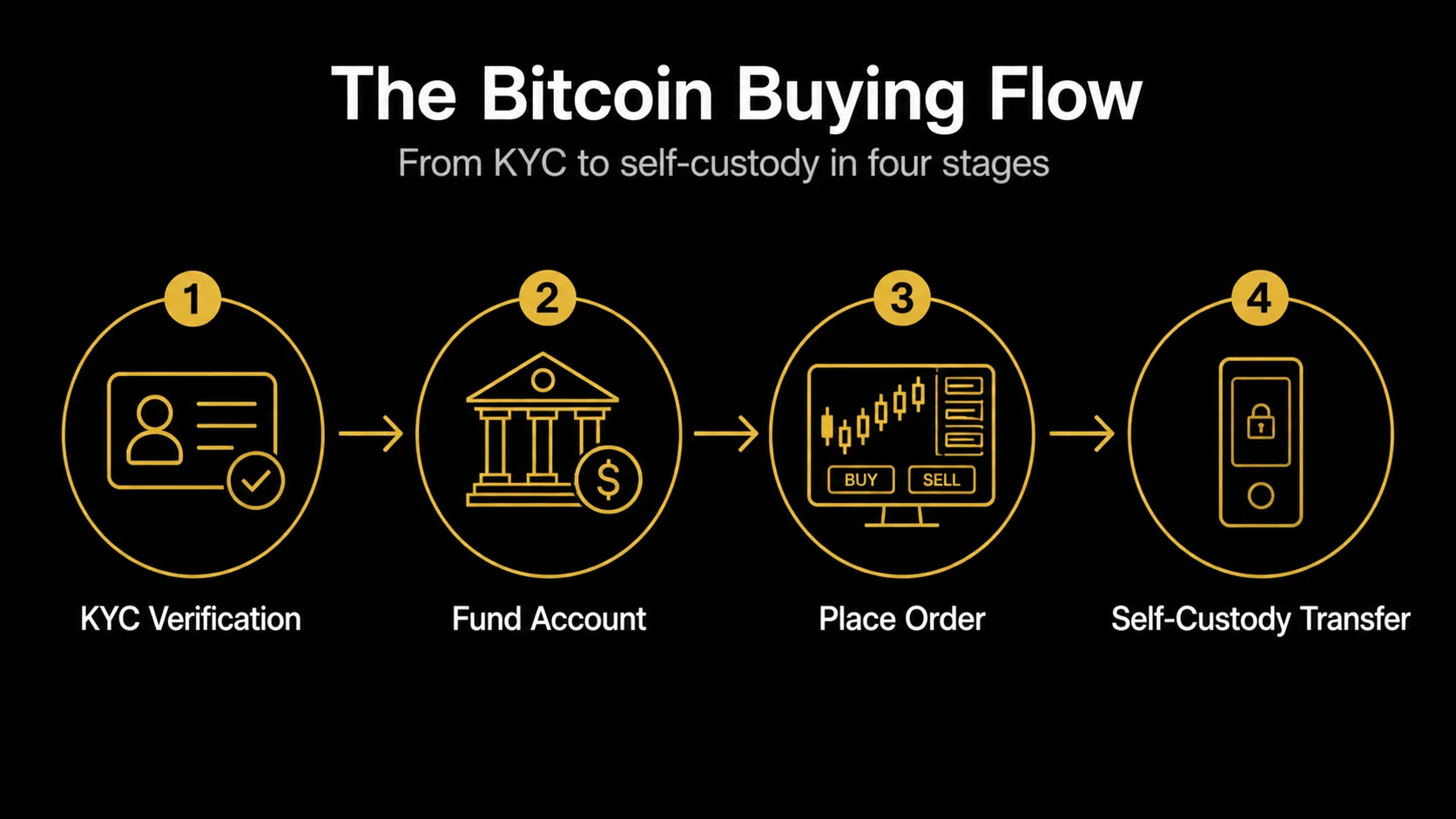

Step-by-Step Buying Process

Quick start checklist

- Choose a reputable exchange — OKX, Coinbase or Kraken

- Complete identity verification (KYC)

- Add a secure payment method

- Enable two-factor authentication (use an authenticator app, not SMS)

- Make your first Bitcoin purchase

- Transfer to a hardware wallet for long-term storage

Step 1: Choose your exchange

OKX is our default recommendation for the lowest fees and deepest BTC liquidity (its broadest product is outside the US; OKX US, launched 2025, is spot-only and excludes some states). For US residents, Coinbase is the easiest entry point for beginners; Kraken offers stronger security pedigree and lower fees on its Pro interface for more experienced traders.

Factors to consider when choosing:

- Fees — trading fees, deposit/withdrawal fees, payment-method fees

- Payment methods available — bank transfer, card, P2P depending on jurisdiction

- Security and regulation — two-factor authentication, insurance coverage, regulatory compliance

- Reputation and track record — operational history, proof of reserves, past incidents

- User interface — ease of use for beginners

Step 2: Create your account

Visit your chosen exchange's official website (verify the URL carefully — phishing sites are common) and sign up:

- Enter your email address and create a strong, unique password

- Verify your email address through the confirmation link

- Enable two-factor authentication (2FA) immediately, before any other action

- Use Google Authenticator, Authy or a hardware security key — avoid SMS-based 2FA where possible (vulnerable to SIM swapping)

Step 3: Complete identity verification (KYC)

All reputable exchanges require KYC verification to comply with anti-money-laundering regulations. The process typically requires:

- Personal information — full name, date of birth, residential address

- Government-issued ID — passport, driver's licence or national ID card

- Proof of address — utility bill or bank statement less than 3 months old

- Selfie verification — photo or video of yourself, sometimes holding your ID

Verification typically takes 1-3 business days. Some exchanges offer instant verification for smaller deposit limits, with higher limits unlocked after fuller verification.

Step 4: Add a payment method

Link your preferred payment method to fund your account. Each method has different fee and speed trade-offs:

Bank transfer (ACH or wire) — lowest fees

- Fees: usually free or very low (under 0.5%)

- Processing time: 1-5 business days for ACH, same day for wire transfer

- Best for: large purchases, regular recurring DCA

Debit card — instant but expensive

- Fees: 2-4% depending on exchange and card

- Processing time: instant

- Best for: small purchases, urgent deployment

Wire transfer — large amounts

- Fees: $15-25 + exchange fees

- Processing time: same day to 1 business day

- Best for: very large purchases ($10,000+)

Avoid credit cards. Most banks treat crypto purchases as cash advances, applying both purchase fees (2-4%) and cash advance interest from day one. The total cost typically exceeds 10% on a credit card purchase.

Step 5: Buy your first Bitcoin

With KYC complete and payment method connected, you can place your first order:

- Navigate to the "Buy" or "Trade" section

- Select Bitcoin (BTC) from the list of cryptocurrencies

- Choose your funded payment method

- Enter the amount in your local currency (USD, GBP, EUR) or in BTC

- Choose order type — market order for immediate execution, limit order for specific entry price

- Review transaction details, including all fees, before confirming

- Confirm the purchase

For your very first purchase, start with a small amount ($50-100) to get familiar with the workflow before committing larger capital. The full DCA execution framework — recurring buy automation, fee minimisation, hardware wallet routing — sits in our Bitcoin DCA strategy playbook.

Fee Structure

Total cost depends on the exchange, payment method, and any withdrawal you make to a hardware wallet.

Total cost example for a $1,000 Bitcoin purchase

- OKX (bank transfer) — approximately $0.80-$1.00 total cost (0.08-0.10%)

- Kraken (bank transfer) — approximately $2.50-$4.00 total cost (0.25% maker / 0.40% taker base tier)

- Coinbase Advanced (bank transfer) — approximately $4-6 total cost (0.40-0.60%)

- Coinbase simple buy (debit card) — approximately $39 total cost (~3.9%)

- Bitcoin ATM — $50-150 total cost (5-15%)

Trading fees

- OKX — 0.08-0.10% spot maker/taker (lower with volume tiers)

- Coinbase Advanced — 0.4-0.6% (Coinbase simple buy: ~1.49%)

- Kraken — 0.25% maker / 0.40% taker base tier on Kraken Pro (lower with 30-day volume)

Payment method fees

- Bank transfer (ACH) — usually free or under 0.5%

- Debit card — 2-4%

- Credit card — 2-4% + cash advance fees from your bank

- Wire transfer — $15-25 fixed fee plus exchange fees

Withdrawal fees

Moving Bitcoin off-exchange to your hardware wallet incurs two costs:

- Bitcoin network fee — $1-10 typically, varies with network congestion. Check current fee estimates before initiating large withdrawals; sending during low-congestion periods can save significant amounts on consolidating multiple smaller withdrawals.

- Exchange withdrawal fee — $0-25 depending on exchange and pricing model. Some exchanges charge flat fees regardless of withdrawal amount; others scale with the amount; some waive withdrawal fees for higher account tiers or specific tokens.

- Address verification time — not a monetary cost but worth budgeting. Always verify the destination address on the hardware wallet screen against the exchange screen before approving the transaction. This 30-second check has prevented many irreversible losses to clipboard-malware substitution attacks.

For tax-advantaged structures (US IRAs, UK ISAs/SIPPs), spot Bitcoin ETFs are typically the better path because direct Bitcoin in retirement accounts requires specialised infrastructure. The detailed ETF-versus-direct decision framework, including tax wrapper differences across US, UK and EU markets, sits in our spot Bitcoin ETF vs direct BTC framework.

Storage and Self-Custody Basics

Once you own Bitcoin, where you store it determines who actually controls it. Bitcoin storage options sit on a spectrum from custodial convenience to operational sovereignty.

Storage options ranked by security

- Exchange custody — your Bitcoin sits in the exchange's custodial wallet. Acceptable for small balances and active trading. Carries counterparty risk (Mt Gox, FTX and other major exchange failures have produced the largest historical retail Bitcoin losses).

- Software wallets — non-custodial wallets running on your phone or computer. Better than exchange custody for medium balances but vulnerable to malware on the device. Examples: Trust Wallet, Exodus, Electrum.

- Hardware wallets — physical devices that store private keys offline. The standard for serious holdings. Transactions must be signed on the device itself, which protects against malware on your computer.

The exchange-to-hardware-wallet workflow

For balances over approximately $1,000, the standard workflow is:

- Buy Bitcoin on the exchange

- Set up a hardware wallet (initialisation, seed phrase generation)

- Back up the seed phrase on metal backup hardware (eliminates fire and water risk)

- Transfer a small test amount from the exchange to verify the address works

- Transfer the larger balance once the test confirms successfully

- Run a recovery test before relying on the system for any meaningful balance

The detailed walkthrough — initialisation, seed-phrase backup options, transfer testing, recovery testing, multi-sig considerations — sits in our hardware wallet security guide.

Critical security rules

- Never share your seed phrase or private keys with anyone, including support staff impersonators

- Never type your seed phrase into any device, online form, photograph or cloud storage

- Always verify addresses on the hardware wallet display, not just the computer screen (clipboard malware is common)

- Buy hardware wallets directly from manufacturers, never through Amazon resellers (supply-chain compromise risk)

Buying Strategies (DCA vs Lump Sum)

How you accumulate Bitcoin matters more than which exchange you use. The two primary approaches are dollar-cost averaging (DCA) and lump-sum investment, with most investors using some combination.

Dollar-cost averaging (DCA)

DCA involves buying a fixed dollar amount of Bitcoin on a regular schedule (typically weekly or monthly) regardless of price. The strategy reduces timing risk and removes emotional decision-making from the process.

Benefits:

- Smooths out price volatility over time

- Reduces risk of buying at local market peaks

- Removes emotion from the buying decision

- Accessible to investors with limited capital — start with $50-100 per week or month

- Compatible with recurring-buy automation on most major exchanges

Lump sum

Investing a larger amount at once can be effective during market downturns or when you have high conviction about Bitcoin's long-term prospects. The trade-off is timing sensitivity — a poorly-timed lump sum during a market peak can result in extended drawdown periods before breakeven.

Hybrid approach

Many serious investors combine both: deploy approximately 50-70% of intended allocation as a lump sum to establish the position, then DCA the remaining 30-50% over the following 6-18 months. This captures most of the long-term return while spreading entry risk.

Allocation sizing

How much Bitcoin to buy depends on time horizon, income stability and existing wealth concentration. Common allocation patterns:

- Conservative (1-5%) — small alternatives sleeve, suitable for investors near retirement or with concentrated wealth

- Balanced (5-15%) — meaningful but not dominant component, suitable for investors with 10+ year horizons

- Aggressive (15-30%) — strong conviction allocation requiring multi-decade horizons and demonstrated behavioural tolerance

The detailed allocation framework — including the volatility-budget logic, three-tier sizing approach and rebalancing mechanics — sits in our Bitcoin portfolio allocation guide.

Common Mistakes to Avoid

Most retail Bitcoin losses come from preventable mistakes rather than from market downturns. The most common errors:

1. Buying during FOMO

Avoid buying Bitcoin just because the price is rising rapidly and social media is excited. The strongest behavioural pressure to buy typically occurs near local market peaks, which produces the worst long-term returns. Stick to your DCA schedule or pre-committed lump-sum plan rather than chasing momentum.

2. Using credit cards

Credit card purchases are typically the worst possible payment method for Bitcoin. Banks treat crypto purchases as cash advances, applying purchase fees (2-4%) plus cash advance interest from day one. Total cost can exceed 10% before you even own the Bitcoin.

3. Keeping large balances on exchanges

Exchange custody carries counterparty risk. Move significant balances (over approximately $1,000) to a hardware wallet for long-term storage. Mt Gox, FTX, Celsius, BlockFi and other major exchange failures have produced the largest historical retail Bitcoin losses.

4. Skipping hardware wallet setup

Many new investors keep Bitcoin on exchanges indefinitely because hardware wallet setup feels intimidating. The reality is that the full setup takes 2-4 hours and produces a permanent storage system. The detailed walkthrough in our hardware wallet guide makes the process straightforward.

5. Not running a recovery test

The most common backup-failure mode is discovering after a hardware wallet failure that the seed phrase backup does not actually work. Run a recovery test before transferring significant balances — initialise a second wallet from your backup and verify the addresses match.

6. Panic selling during drawdowns

Bitcoin's worst peak-to-trough drawdowns have reached 70-85% in prior cycles. The defensible working assumption for 2026 is that 50-70% drawdowns remain plausible. If you cannot sustain those drawdowns without selling, you are sized too aggressively.

7. Falling for scams and impersonation

Common scam patterns:

- Fake support staff messaging you about "account issues" — real support never DMs first

- "Investment opportunities" promising guaranteed returns — Bitcoin offers no guaranteed returns

- Phishing emails with urgent action required — verify URLs carefully before clicking

- Anyone asking for your seed phrase, private keys, or 2FA codes — these are always scams

Alternative Ways to Buy Bitcoin

Centralised exchanges are the most common path, but several alternatives serve specific needs.

Spot Bitcoin ETFs

Spot Bitcoin ETFs provide regulated Bitcoin exposure inside standard brokerage accounts:

- Available through any standard brokerage (Fidelity, Schwab, Vanguard, Hargreaves Lansdown, IG, Trading 212, AJ Bell and others)

- Best for retirement accounts (US IRAs, UK ISAs/SIPPs) and tax-advantaged wrappers where direct Bitcoin is impractical

- Annual expense ratio (typically 0.20-0.25%) replaces direct holding's no-fee structure

- No self-custody complexity, but no self-sovereignty either

The detailed ETF-versus-direct decision framework sits in our spot Bitcoin ETF vs direct BTC framework.

Bitcoin ATMs

Bitcoin ATMs allow cash purchases at physical locations:

- Available in many cities worldwide

- Higher fees (5-15%) than exchanges

- Useful for cash-only purchases or specific privacy needs

- Not appropriate for regular accumulation due to fee structure

Peer-to-peer (P2P) platforms

P2P platforms let you buy Bitcoin directly from other individuals:

- More payment method flexibility (cash, gift cards, payment apps)

- No KYC required on some platforms (creates compliance considerations in some jurisdictions)

- Higher scam risk than centralised exchanges

- Better suited to specific use cases than as a primary accumulation method

Regional Considerations

The general workflow is similar across jurisdictions, but specific operational details differ in ways that affect convenience, cost and tax treatment.

United Kingdom

UK buyers operate under FCA registration requirements that limit which exchanges can serve UK retail customers. Coinbase (CB Payments Ltd), Kraken (Payward Ltd) and Bitstamp UK Ltd are on the FCA cryptoasset register. OKX is not currently on the FCA cryptoasset register and serves UK users under the financial-promotions risk-warning regime, so UK retail buyers should prefer an FCA-registered exchange. Some non-FCA-registered exchanges have stopped accepting UK customers since the FCA cryptoasset financial promotion rules took effect in October 2023.

Three UK-specific considerations matter operationally:

- Faster Payments funding — most UK exchanges accept Faster Payments bank transfers, settling in minutes rather than the 1-3 days typical of US ACH. This makes UK exchange funding genuinely fast for non-card methods.

- Travel Rule compliance — UK exchanges are required to collect originator and beneficiary information for Bitcoin transfers above certain thresholds. This adds a small operational step when sending Bitcoin off the exchange to self-custody, particularly the first time you withdraw to a new wallet address.

- ISA capacity for ETP exposure — UK investors with unused ISA allowance should consider whether ISA-eligible Bitcoin ETPs through Hargreaves Lansdown, IG, Trading 212 or AJ Bell make more sense than direct exchange purchases. The ISA wrapper benefit dwarfs the expense ratio cost over multi-decade horizons. Direct exchange Bitcoin still serves strategic conviction allocation, but ISA-wrapped ETP exposure should usually come first if capacity exists.

European Union

EU buyers operate under the MiCA framework that came into effect during 2024-2025, providing harmonised regulatory treatment across member states. Major exchanges including OKX, Coinbase, Kraken and Bitstamp serve EU customers under MiCA-compliant authorisations. SEPA bank transfers replace ACH as the standard low-fee funding method.

Tax treatment varies materially by member state — Germany's 12-month tax-free rule favours direct holdings, France's flat 30% rate makes the wrapper choice neutral, Netherlands' wealth tax treatment changes the calculation entirely. For positions above approximately €25,000, the few hundred euros spent on a qualified local accountant before structuring the position pays back many times over.

Other jurisdictions

Worldwide, the OKX recommendation typically holds for non-US, non-UK markets where OKX is licensed. Local exchanges sometimes offer better local-currency funding methods or tax reporting integration. Singapore (Independent Reserve, Coinhako), Australia (Independent Reserve, Swyftx), Canada (Bitbuy, Newton, Shakepay) and Japan (bitFlyer, Coincheck) all have well-regulated local options. The choice between OKX and a local exchange usually depends on whether deeper liquidity (OKX) or local-currency support and tax reporting integration (local exchange) matters more for your specific situation.

Common First-Purchase Failures (and How to Avoid Them)

Most first-time Bitcoin buyer mistakes are predictable. Five patterns produce the majority of operational failures we see retail investors generate, and recognising them in advance protects you from outcomes that range from minor frustration to total loss of funds.

Failure 1: Falling for support staff impersonators

Within days of your first Bitcoin purchase, you will likely receive contact from people claiming to be exchange support staff. Email, SMS, social media DMs, even phone calls — the targeting is sophisticated. Every legitimate exchange explicitly says they will never request seed phrases, 2FA codes or passwords. Every impersonator request begins by asking for one of those.

The single rule that protects against this entire attack category: legitimate exchange support never initiates contact. If you receive a message claiming to be from your exchange, do not respond. If you have a genuine support need, log in to the exchange directly through the official URL (bookmarked, not clicked from messages) and use their in-app support chat.

Failure 2: SIM-swap-vulnerable 2FA

SMS-based 2FA was acceptable security for general internet accounts a decade ago. It is not acceptable security for cryptocurrency accounts in 2026. SIM-swap attacks specifically target crypto holders — attackers convince mobile carriers to port your phone number to their device, then receive your 2FA codes and drain your accounts.

The fix is straightforward: use authenticator apps (Google Authenticator, Authy, Microsoft Authenticator) or hardware security keys (YubiKey) for all cryptocurrency accounts. The setup takes 10 minutes per account and protects against the most common attack vector against retail crypto holders.

Failure 3: Hardware wallet from the wrong source

Hardware wallets purchased from anywhere other than the manufacturer's official website carry supply-chain compromise risk. Amazon, eBay, third-party resellers and "discount" listings have all been documented as vectors for hardware wallets that arrive with pre-generated seed phrases controlled by the attacker. The user transfers Bitcoin to the compromised wallet and loses it.

Always order hardware wallets directly from the manufacturer (ledger.com, tangem.com, trezor.io). The few dollars saved on third-party listings is not worth the risk of a complete loss. Verify the device tamper seal on arrival and initialise the wallet yourself — never use a hardware wallet that arrives with a pre-printed seed phrase, regardless of the source.

Failure 4: Seed phrase digitally stored

The seed phrase is the master key to your Bitcoin. Anyone with your seed phrase has total control over your funds. The most common storage failures: photographing the seed phrase, typing it into a notes app, storing it in cloud storage, emailing it to yourself, or saving it to a password manager.

The correct approach is physical-only storage: write the seed phrase by hand on paper or stamp it onto metal backup hardware. Store the physical backup in a secure location separate from the hardware wallet itself. Never photograph it, never type it into any device, never share it with anyone — including support staff, family members or "trusted advisers" who claim to need it.

Failure 5: Exchange complacency

Bitcoin sitting on an exchange long after the purchase is the highest single-incident loss vector for retail investors. Exchange custody is acceptable for small balances and active trading. It becomes problematic at amounts above approximately $1,000 in holdings, and unjustifiable above $5,000.

The fix is operational discipline: schedule quarterly transfers from exchange to hardware wallet for accumulated holdings above the threshold. Treat the exchange as a buying venue, not a custody platform. The investors who lost money in Mt Gox, FTX, Celsius and other exchange failures were not the early adopters who used exchanges briefly for trading — they were the longer-term holders who left funds on the platform "just for now" and never moved them.

Funding method tradeoffs across exchanges

Choosing payment method substantially affects realised purchase pricing through different combinations involving processing fees, transaction spreads, settlement timing, daily transaction limits, regional availability constraints, additional regulatory verification requirements, customer support quality, transaction reliability through volatile market periods, refund handling procedures, alongside cumulative friction across recurring purchase relationships. Investors typically evaluate funding methods through balanced consideration across operational convenience, total cost, settlement speed, daily transaction limits, secondary regulatory considerations, alongside individual preferences regarding particular banking relationships providing established support.

Bank transfers (ACH transfers, SEPA transfers, Faster Payments) typically provide lowest combined fee-and-spread cost across payment options across most regulated platforms supporting Bitcoin purchases through major financial markets. Settlement timing involving bank transfers extends typically across several business days, creating operational latency between initiating transactions alongside actual Bitcoin acquisition. Investors building positions across extended timeframes through systematic accumulation typically prioritise minimising aggregate transaction costs across cumulative purchases, favouring bank transfers despite slower settlement timing.

Debit card purchases provide instant Bitcoin acquisition without settlement latency, supporting investors particularly responsive towards immediate transaction completion. Combined fee-and-spread costs through debit card purchases substantially exceed bank transfer alternatives, representing meaningful aggregate operational expense across recurring transactions. Investors maintaining systematic recurring purchases through extended timeframes therefore typically experience materially better cumulative outcomes through bank transfer rather than card-based methods, although individual transactions sometimes specifically benefit through immediate settlement timing supporting particular operational requirements involving timing-sensitive purchases.

Wire transfers support larger transaction values exceeding typical bank transfer limitations, primarily benefiting investors purchasing substantial Bitcoin positions through individual transactions rather than systematic accumulation across recurring purchases. Fees involving wire transfers generally exceed alternative methods, justifying selection primarily through transaction value justifying additional cost. Investors completing substantial single purchases routinely select wire transfers despite increased fees, primarily because transaction value justifies premium relative aggregate cost percentage substantially below percentage applicable through alternative methods supporting smaller transaction values.

What to Do After Buying

1. Secure your investment

For balances over approximately $1,000, transfer to a hardware wallet for long-term storage. Smaller balances can remain on the exchange for active management, but operational discipline matters even at small balances — exchange security incidents do not respect position size.

2. Document your records

Keep accurate records of every Bitcoin transaction:

- Date and time of purchase

- Amount purchased (in BTC and in your local currency)

- Exchange and transaction ID

- Cost basis including all fees paid

- Wallet addresses used for storage

This documentation matters for tax compliance and for portfolio tracking. Most jurisdictions tax Bitcoin disposals (sales) but not purchases — accurate cost basis records ensure you only pay tax on actual gains.

3. Continue learning

Once you own Bitcoin, deeper context helps you make better long-term decisions:

- Bitcoin investment fundamentals hub — comprehensive Bitcoin investment framework

- Bitcoin portfolio allocation — detailed sizing framework

- Bitcoin cycle 2026 — how the halving cycle has changed in the post-ETF era

- Hardware wallet security hub — detailed self-custody guide

4. Set your strategy

Decide whether you are:

- Accumulating long-term — DCA into target allocation, hold through cycles

- Building a strategic position — combine lump sum with ongoing DCA towards target sizing

- Trading actively — different operational and tax considerations apply (active trading is outside the scope of this guide)

For most retail investors, the disciplined accumulation approach produces better long-term results than active trading. Bitcoin's structural properties favour patient holders who size correctly and stick to the plan.

Conclusion

Buying Bitcoin in 2026 is straightforward when you follow the standard workflow: choose a regulated exchange appropriate to your jurisdiction, complete KYC, fund with bank transfer for lowest fees, place your order, and transfer significant balances to a hardware wallet for long-term storage. The full setup takes 2-4 hours the first time and produces a permanent system you can rely on.

The most consequential decisions are not which exchange to use but how much to buy, how to space out purchases, and how to secure the result. The disciplined accumulation pattern — DCA into appropriate allocation, hardware wallet self-custody for serious balances, hold through cycles — has produced the best long-term outcomes for retail investors historically.

First-purchase quick-start checklist

If you want a condensed action plan for your first Bitcoin purchase, work through these steps in order:

- Choose your exchange based on your jurisdiction (in the US, Coinbase or Kraken; elsewhere, OKX for the lowest fees) and complete identity verification. Allow 24-48 hours for KYC to clear, longer for some non-US jurisdictions.

- Fund the account via bank transfer rather than card. Bank transfer fees are 80-95% lower than card fees, and the 1-3 day settlement time is acceptable for first-purchase scenarios where you are not trying to capture a specific price.

- Place your first purchase as a small test transaction — $50-100 — even if you intend to buy more. The test confirms your account works and lets you observe the fee structure before committing larger amounts.

- Configure 2FA properly using an authenticator app (Google Authenticator, Authy, or hardware security key like YubiKey). Never use SMS-based 2FA for cryptocurrency accounts; SIM-swap attacks specifically target crypto holders.

- Order a hardware wallet if your accumulation target exceeds approximately $1,000. Order directly from the manufacturer rather than from Amazon resellers (supply-chain compromise risk has been documented for cheap-price third-party listings).

- Set up recurring buys if you intend to DCA. Configure for the day after your salary deposit to ensure consistent execution.

- Document your cost basis from day one. Tax compliance requires accurate records of every purchase: date, amount, price, fees and exchange.

What to monitor in the first 90 days

The first three months after your initial purchase are the highest-risk window for operational mistakes. Pay attention to four signals:

- Phishing attempts — fake "exchange support" emails, SMS or social media messages will arrive within days of your first purchase. Legitimate exchange support never asks for seed phrases, 2FA codes or passwords. Any message requesting them is fraudulent.

- Account security alerts — log in once a week to verify your account remains secure, your 2FA is functional and your withdrawal whitelist (if configured) has not been modified.

- Recurring buy execution — confirm DCA purchases are executing on schedule and at expected amounts. Failed payments due to bank-side rejections occasionally happen and need addressing.

- Hardware wallet firmware updates — once you have a hardware wallet, install firmware updates promptly when issued by the manufacturer. Out-of-date firmware can have known vulnerabilities that updates address.

For deeper analysis of Bitcoin specifically as an investment, see our Bitcoin review. For detailed DCA setup walkthroughs across exchanges, see our DCA strategy playbook.

Sources & References

- Bitcoin.org — official Bitcoin documentation and resources

- U.S. Securities and Exchange Commission — spot Bitcoin ETF approval orders and exchange oversight

- UK Financial Conduct Authority — UK retail Bitcoin ETP and exchange regulation framework

- Bitcoin Portfolio Allocation

- Bitcoin DCA Strategy Playbook

- Spot Bitcoin ETF vs Direct BTC

- Hardware Wallet Security 2026 Hub

- What is Bitcoin: Complete Guide

- Bitcoin Review: Investment Analysis

Frequently Asked Questions

- How much Bitcoin should I buy?

- Only invest what you can afford to lose. Common allocation guidance ranges from 1-10% of investment portfolios depending on risk tolerance, time horizon and existing wealth. Start with the conservative tier (1-5%) and scale up only after you have demonstrated behavioural tolerance through a Bitcoin drawdown.

- Can I buy a fraction of a Bitcoin?

- Yes. Bitcoin is divisible to eight decimal places (1 satoshi = 0.00000001 BTC). You can buy as little as $1-10 worth on most major exchanges. You do not need to buy a whole Bitcoin.

- Is it safe to buy Bitcoin?

- Buying Bitcoin from reputable exchanges like OKX, Coinbase or Kraken is generally safe. The Bitcoin network itself has never been successfully attacked at the protocol level in over 17 years. However, cryptocurrency investments carry risks including price volatility, exchange counterparty risk, and operational risk if you self-custody.

- What is the best time to buy Bitcoin?

- There is no perfect time to buy Bitcoin. Most disciplined investors use dollar-cost averaging (DCA) — buying a fixed dollar amount on a regular schedule regardless of price — to remove timing risk and emotional decision-making from the process.

- Do I need to verify my identity to buy Bitcoin?

- Yes. All regulated exchanges require KYC (Know Your Customer) verification, including government-issued ID and proof of address. This is required by law in most countries to prevent money laundering and is the standard for any reputable platform.

- How long does it take to buy Bitcoin?

- After account verification (typically 1-3 business days), you can buy Bitcoin instantly with a debit card or within 1-5 business days with a bank transfer. The verification step is one-time; subsequent purchases are fast.

- What is the minimum amount I can buy?

- Most major exchanges allow Bitcoin purchases as small as $1-10, making Bitcoin accessible at any budget. Some exchanges have higher minimums for specific payment methods (bank transfers may require $20-50 minimum).