Best L2s for DeFi 2026 Guide

You picked an L2 family from the hub — now you want the protocol-level picture. What actually runs on Arbitrum versus Optimism versus Base in 2026? Which ZK L2 has DeFi worth using yet? This satellite is a 2026 snapshot of the DeFi landscape per L2: which protocols anchor each chain, what is mature versus nascent, and how the Velodrome-into-Aerodrome consolidation reshaped Optimism's DeFi composition. Refresh annually — landscape shifts every six months.

Introduction

What this guide covers:

- The Arbitrum DeFi anchor stack: GMX V2 perps, Camelot V3 AMM, Aave lending — and the operational tradeoffs each carries

- Optimism's derivatives-and-lending centre of gravity around Synthetix, Aave and Uniswap

- Base as the fastest-growing AMM hub after the Velodrome-to-Aerodrome consolidation

- ZK L2 DeFi maturity: zkSync Era, Linea and Starknet TVL gaps, integration tooling gaps, and what's worth watching in 2026

- Cross-L2 DeFi strategies — when single-L2 deployment beats multi-L2, and the bridging cost calculus that decides it

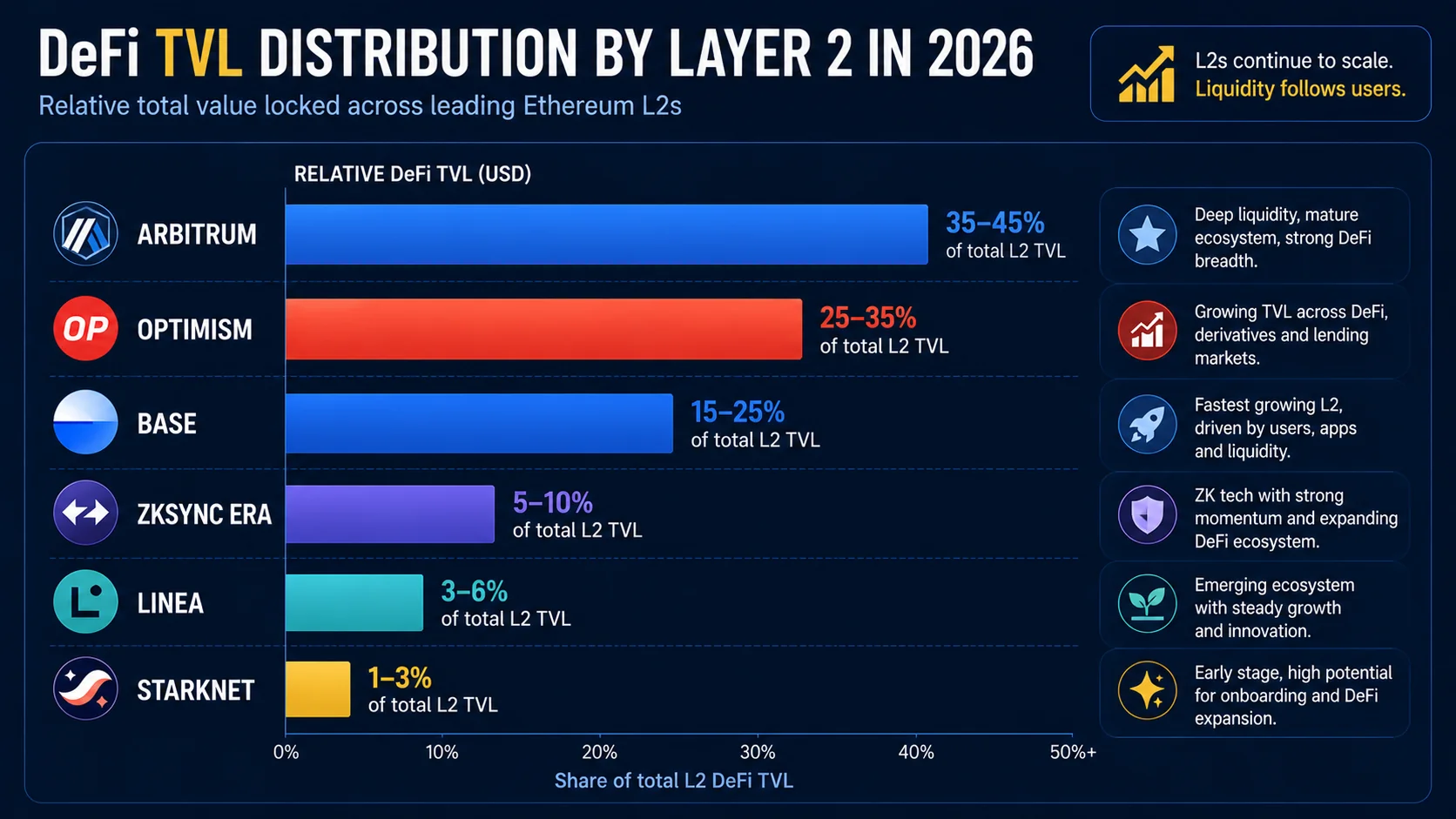

DeFi distribution across L2s is uneven and the unevenness matters. Not every DeFi protocol deploys on every chain. Deep perps liquidity lives on Arbitrum; derivatives infrastructure has its centre of gravity on Optimism; AMM volume has been migrating to Base since 2024; the ZK L2s remain an order of magnitude smaller for DeFi by total TVL. If you pick the wrong L2 for the strategy you want to run, you will pay it in either liquidity depth (worse fills), protocol availability (the thing you want to use is not deployed), or operational overhead (cross-L2 bridging to access protocols that live elsewhere).

This guide is a 2026 snapshot — the per-L2 picture below reflects the DeFi landscape as of mid-2026, with explicit annual refresh on the URL. The landscape genuinely shifts every six months at the level of detail relevant to where you deploy capital, so you should treat any landscape-snapshot guide (including this one) as accurate at the time of writing and worth re-verifying against DefiLlama and L2BEAT before any meaningful deployment. The 2027 refresh will live at a parallel URL.

The structure mirrors the four practical L2 families: Arbitrum (perps and yield), Optimism (derivatives and lending, re-anchored after the Velodrome-to-Aerodrome consolidation), Base (the fast-growing DEX hub), and the ZK L2s (nascent but worth tracking). A short cross-L2 strategies section covers when multi-L2 deployment makes sense and when single-L2 focus is better. For the broader L2 selection framework — which chain to use for which application beyond DeFi — see our Ethereum L2 complete guide.

One framing worth setting upfront: protocol selection on an L2 is a separate decision from chain selection. Pick the chain by deepest liquidity for your primary strategy, then pick the protocol within that chain by audit track record and incident history. The two decisions cluster around different signals — TVL trajectory and ecosystem coordination drive chain choice, while time in production and independent security-research coverage drive protocol choice. Treat the guide below as decision support for both axes rather than a ranking, because the right answer changes with strategy size and risk tolerance.

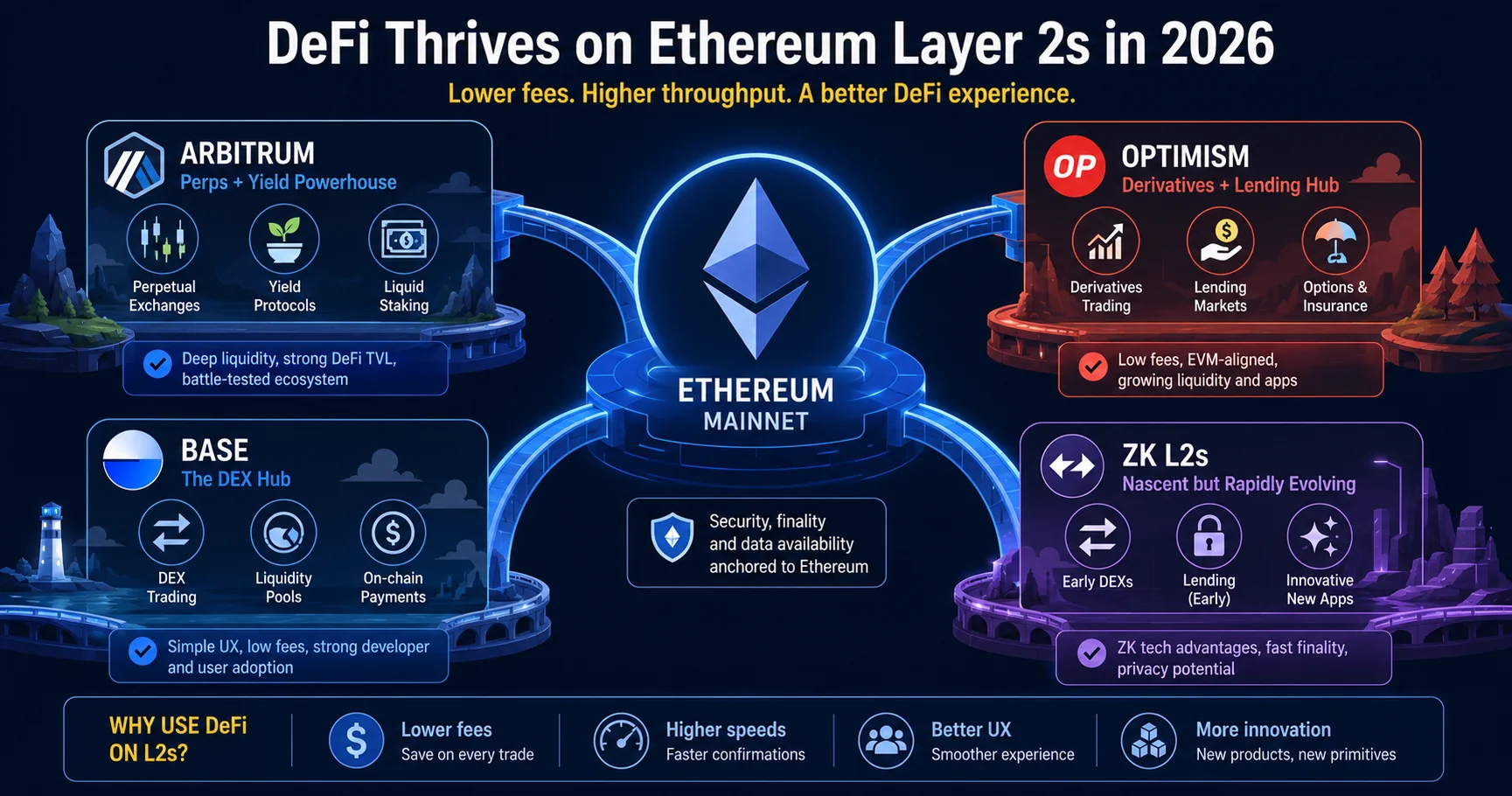

Arbitrum DeFi: Perps and Yield

Arbitrum is the deepest L2 for perpetual futures and a serious venue for yield strategies. The chain leads the L2 TVL rankings in mid-2026 and hosts the most mature perps engine in the L2 ecosystem (GMX), the most active alternative DEX (Camelot), and a full Aave deployment with deep liquidity for the major assets. If your strategy involves perps, yield-bearing positions, or any combination of the two, Arbitrum is the default pick.

GMX V2 — flagship perps engine

GMX is the perps DEX that anchors Arbitrum's commercial DeFi story. V2 is the current production version, with the GLV (GMX Liquidity Vault) and GM (GMX Markets) liquidity model. V1 had a roughly $40 million reentrancy exploit in July 2025 that fully compensated GLV liquidity providers; V2 was architecturally unaffected because of the separated market design that limits cross-pool exposure. The 2026 picture: V2 is the default for active perps trading, and the real-yield model continues to distribute trading-fee revenue to GMX and GLV stakers.

Pick GMX for perps on the major crypto pairs (BTC, ETH, SOL, plus mainstream altcoins) where the deeper L2 perps liquidity matters for execution. The user-experience is mature, the documentation is good, and the funding-rate structure is stable enough to model. The trade-off is that GMX is a single-venue dependency — if you are running serious perps size, you should consider holding a parallel position on a second venue (Synthetix on Optimism or a CEX) as resilience against any single-protocol incident.

A concrete sizing rule helps. If your perps position is under $10,000, GMX alone is fine — the operational simplicity of a single venue outweighs the diversification benefit. Between $10,000 and $100,000, you should hold the majority on GMX and a smaller tail position on a CEX or Synthetix as venue-risk hedge. Above $100,000, the venue split should be deliberate — perhaps 60/40 between GMX and one alternative — because the absolute downside of a single-protocol incident becomes material. The picture is not about whether GMX is safe (V2 has been operationally clean since launch) but about whether you want to be fully exposed to any single L2 protocol for capital that you cannot afford to write down.

Camelot DEX (V3) — Arbitrum-native AMM

Camelot is the second-most-active Arbitrum DEX and the chain's native AMM project. V3 introduced concentrated-liquidity primitives and the GRAIL/xGRAIL real-yield token model. TVL sits in the high-tens-of-millions range on Arbitrum directly, with additional cross-chain deployment via Camelot's Orbit framework that extends the protocol to other Arbitrum-derived chains.

Pick Camelot for Arbitrum-native pair liquidity that Uniswap might not have the depth on — particularly for newer Arbitrum-launch tokens that list on Camelot first. For mainstream pairs (ETH/USDC, ARB/USDC) Uniswap on Arbitrum often has better execution. For the long tail of Arbitrum-native tokens, Camelot is the natural venue.

Aave on Arbitrum — lending depth

Aave's Arbitrum deployment is a full V3 lending market with deep liquidity for the major assets (ETH, USDC, USDT, WBTC) and meaningful liquidity for ARB and a curated set of altcoins. The supply rates are the standard variable-rate model; borrow rates depend on utilisation; the interface and risk model are the same as Aave V3 on any other deployment. For any L2 lending position above a few thousand dollars, Aave Arbitrum is the default starting point.

Concrete numbers help calibrate expectations. USDC supply rates on Aave Arbitrum typically sit in the 3-6 per cent range during normal market conditions, climbing to 8-12 per cent during high-utilisation periods (post-airdrop deployment, leveraged farming cycles). ETH supply rates are usually lower, in the 1-3 per cent range, with occasional spikes during leverage-cycle peaks. If you are choosing between Aave Arbitrum and Aave on a different L2 for the same asset, the rate differential is usually less than 1 per cent on the supply side — pick based on which chain your other strategy components live on, not on rate-shopping.

Operational note: May 2026 state-update lag

Arbitrum experienced a state-update lag of roughly 12 hours 58 minutes on 9-10 May 2026 (against a typical interval of about 1 hour 1 minute). The operational impact on DeFi user-experience was minimal during the event — soft confirmations continued on L2, and transactions kept processing. For the full security context, see our L2 security tradeoffs satellite.

Worked example — Arbitrum yield-farming session

A concrete day-in-the-life. You start with $10,000 of USDC on Arbitrum (deposited via exchange-native withdrawal — Binance or OKX both support direct Arbitrum withdrawals). The session: deposit $7,000 of USDC into Aave Arbitrum to earn the supply rate; use $2,000 of USDC as the funding source for a small GMX perps position (long ETH, 2x leverage); leave $1,000 of USDC as gas buffer plus opportunistic Camelot LP allocation. Total fees for the setup phase: under $1 in L2 gas across all transactions during normal conditions. The Aave supply earns continuous yield; the GMX position pays funding (or earns it, depending on direction); the Camelot LP earns trading-fee revenue plus GRAIL emissions if applicable. The whole session lives on a single L2 — no cross-L2 bridging required.

The same session on Ethereum mainnet would have cost an order of magnitude more in fees during the setup phase, and the GMX equivalent (which is L2-native) would not exist in the same form. This is the structural reason Arbitrum dominates the active DeFi-user market in 2026 — the fee profile makes the strategy economical at scale, and the protocol stack is mature enough that the workflow is genuinely lower-friction than the mainnet alternative.

Optimism: Derivatives and Lending

Optimism is the derivatives-and-lending L2 with Synthetix as the long-running anchor and full Aave plus Uniswap deployments providing the supporting infrastructure. Optimism is also the OP Stack progenitor — the codebase that Base, Ink, Unichain and Soneium share. The cross-Superchain composability roadmap is the most interesting structural development for Optimism DeFi over the 2026-2027 horizon. The chain's DeFi composition has been re-anchored over the past year following the Velodrome-to-Aerodrome consolidation that moved ve(3,3) liquidity infrastructure to Base.

Synthetix — derivatives and perps

Synthetix is the derivatives protocol native to Optimism and the chain's most distinctive DeFi anchor. The protocol issues synthetic assets (synths) collateralised by SNX and provides perpetual-futures markets via the V3 architecture. The debt-pool model means SNX stakers collectively underwrite the synth supply; trading-fee revenue flows back to stakers. Synthetix has been on Optimism since 2021 — the integration is mature, the documentation is extensive, and the developer ecosystem around Synthetix V3 has grown meaningfully through 2025-2026.

Pick Synthetix on Optimism for synthetic-asset exposure (a position in synthetic gold or oil, for example, without the off-chain custody overhead), for certain perps pairs that benefit from the debt-pool architecture, and for the integration ecosystem (Kwenta, Polynomial and other Synthetix-anchored interfaces). For mainstream crypto perps with the deepest L2 liquidity, Arbitrum GMX is usually the better venue; for the Synthetix-specific design, Optimism is the answer.

A practical decision frame: if you can describe the position you want to take in terms of "I want exposure to X without holding the underlying asset" (synthetic crypto basket, synthetic forex pair, synthetic commodity), Synthetix is the natural fit. If you can describe the position as "I want to be long or short a specific crypto pair with leverage", GMX is usually the better venue. The two protocols solve adjacent but distinct problems. If your strategy mixes both, you should hold capital on both chains and budget the cross-L2 bridging cost as a deliberate part of the strategy's expected return — see section 2.6 below for the cross-L2 framework.

Aave on Optimism — standard lending depth

Aave's Optimism deployment is a V3 lending market with deep liquidity for ETH, USDC, USDT and WBTC, plus meaningful OP token liquidity. The supply and borrow rate dynamics are the standard Aave V3 model. For routine lending positions on Optimism, Aave is the default starting point — same as on Arbitrum, with comparable liquidity depth on the major assets. A concrete reference point: USDC supply rates on Aave Optimism typically sit within 50 basis points of Aave Arbitrum during normal conditions, so you should not rate-shop across the two — pick based on which chain your other positions live on. The exception is when one chain has an active leverage cycle driving utilisation, which can open a 1-2 per cent rate spread that is worth capturing.

Uniswap on Optimism — canonical AMM

Uniswap V3 (and V4 where deployed) is the canonical AMM on Optimism with deep liquidity for L2-native trading. For mainstream pair execution (ETH/USDC, OP/USDC), Uniswap is the default. The fees, the front-end and the smart-contract behaviour are identical to Uniswap on any other deployment, so the operational model is straightforward.

The OP Superchain context

Optimism is the OP Stack progenitor — the rollup codebase that Base, Ink, Unichain and Soneium share. The Superchain coordination thesis is that chains running the same codebase can eventually share sequencer infrastructure (the late-2026 shared-sequencer target), share cross-chain message-passing primitives, and ultimately function as a coherent multi-chain liquidity zone rather than as siloed L2s. For DeFi specifically, the Superchain thesis matters because it implies cross-Superchain liquidity routing without the friction of generic cross-chain bridging. The implementation is still on a 2026-2028 roadmap; the strategic implication is that holding DeFi positions across multiple OP-stack chains will become structurally cheaper over time.

Velodrome — predecessor lineage

Velodrome pioneered the ve(3,3) liquidity-emissions model on Optimism and ran successfully for several years; it is merging into Aerodrome's AERO token in Q2 2026 as the consolidated OP-Superchain ve(3,3) vehicle, with VELO holders receiving 5.5 per cent AERO during the merger conversion. For Base-side DEX activity in 2026, Aerodrome (covered in the next section) is the surviving entity. Velodrome is no longer an active recommendation for new ve(3,3) liquidity deployment.

OP Superchain ecosystem implication

Optimism's position as the OP Stack progenitor matters for DeFi capital decisions even though the chain itself is not the largest by TVL. The Superchain coordination thesis — chains running the same codebase eventually sharing sequencer infrastructure, cross-chain message-passing primitives, and liquidity routing — is the structural argument for holding Optimism-native exposure even when comparable TVL exists elsewhere. As of mid-2026, the practical Superchain benefit is limited to shared codebase upgrades (Optimism, Base, Ink, Unichain, Soneium all inherit Cannon fault-proof improvements together). The shared-sequencer roadmap targeting late 2026 would meaningfully change the picture if it ships, enabling near-instant cross-Superchain transactions without external bridge infrastructure.

The practical capital-allocation read: if you believe the Superchain coordination thesis ships substantially over 2026-2028, Optimism-anchored positions become more valuable because the chain's protocols (Synthetix, Aave Optimism, Uniswap) gain access to a unified Superchain liquidity layer. If you are sceptical that the cross-chain coordination ships meaningfully, Optimism positions are valued purely on their standalone merit — which is solid but not differentiated versus Arbitrum or Base alternatives. Watch the Superchain shared-sequencer milestone progression quarterly; if it slips repeatedly past late 2026, treat the coordination thesis as deprioritised and rebalance accordingly.

Base: Emerging Hub

Base is the fastest-growing L2 by DeFi metrics over the 2024-2026 window. Aerodrome alone holds the majority of Base DEX liquidity. Coinbase's smart-wallet integration provides a user-onboarding advantage that no other L2 currently matches at scale, and the on-ramp from Coinbase fiat funding to Base wallet is the smoothest path for new DeFi users. The chain's DeFi composition is genuinely different from Optimism's despite sharing the OP-stack codebase — Base attracted a distinct set of protocols and a distinct user base.

Aerodrome — flagship Base DEX

Aerodrome is the flagship Base DEX and the surviving entity from the Q2 2026 Velodrome merger. TVL sits in the $1.2-1.3 billion range, representing roughly 70 per cent of all Base DEX liquidity. The protocol uses the ve(3,3) emissions model that Velodrome pioneered on Optimism, with Aerodrome's vote-escrowed AERO token (veAERO) governing emissions to specific liquidity pools. The protocol has been through multiple security audits (Spearbit, Code4rena) and the post-merger consolidation has positioned Aerodrome as the unified DEX vehicle for the OP Superchain.

Pick Aerodrome for Base-native DEX activity, particularly for assets that have Aerodrome as their primary liquidity venue. The veAERO emissions structure creates incentive for projects to bribe veAERO holders to direct emissions towards their pools — the active "bribe-economy" on Aerodrome is the practical reason emissions tend to follow new high-volume token launches. For routine large-pair swaps (ETH/USDC, USDC/USDT), Uniswap on Base or Aerodrome both work; for Base-native tokens, Aerodrome is usually the deeper venue. If you are providing liquidity, you should check the current veAERO emissions schedule before committing — the pools receiving the largest emissions weekly are usually the most efficient places to deploy LP capital, and the emissions rotation can shift the right answer week to week.

Uniswap on Base — canonical AMM

Uniswap V3 (and V4 where deployed) provides the canonical AMM on Base with deep liquidity for the major pairs. The deployment is functionally identical to Uniswap on any other chain. For mainstream pair swaps, Uniswap is the default; Aerodrome's edge is on Base-native pairs and on assets where the ve(3,3) emissions model has directed liquidity.

Aave on Base — lending depth

Aave's Base deployment is a V3 lending market with growing liquidity. Coverage is narrower than on Arbitrum and Optimism (fewer supported assets), but the major assets (ETH, USDC, cbETH for Coinbase-issued staked ETH) have meaningful depth. The lending model is the standard Aave V3 design.

Coinbase smart-wallet integration — onboarding differentiator

Base's most distinctive feature is the deep Coinbase smart-wallet integration, which enables passwordless and passkey-based wallets directly on Base without the usual seed-phrase setup overhead. The smart-wallet stack uses ERC-4337 account abstraction to provide the passkey signing flow; Coinbase handles fiat funding directly into the smart wallet; the user is onboarded to a working Base wallet in a few minutes without the traditional Web3 friction.

For new DeFi users — particularly users coming from a CEX-first background — the Base smart-wallet flow is the lowest-friction onboarding path in the L2 ecosystem. The trade-off is that the smart-wallet flow is Coinbase-coupled at the moment, so users who want fully self-sovereign custody from day one should use a standard wallet (MetaMask, hardware wallet) on Base instead. Both paths work — pick based on the user's preferred custody model.

The Coinbase smart-wallet design has implications beyond onboarding speed. Smart wallets enable transaction batching (multiple DeFi actions signed in a single user prompt), social recovery (designated guardians can restore access if you lose the passkey), and per-app spending limits — features that the standard MetaMask EOA flow cannot match without additional ERC-4337 plumbing. For routine Base DeFi interaction, the smart-wallet flow produces fewer confirmation prompts and a calmer UX than the constant approve-and-sign cycle that EVM mainnet users are accustomed to. The trade-off is the Coinbase-dependency lock-in: the smart wallet's recovery and per-app permission features depend on Coinbase's infrastructure rather than purely on the user's private key.

For a concrete sense of the onboarding speed: a new user with a funded Coinbase account can deploy capital into an Aerodrome liquidity pool in roughly five minutes from start to confirmed position. The flow is Coinbase passkey-wallet creation, fiat-to-USDC swap, Base smart-wallet auto-fund, Aerodrome pool deposit — total time including wallet signing prompts is under five minutes on a normal-conditions L2. The equivalent flow with a fresh MetaMask plus a hardware wallet plus a separate fiat on-ramp typically runs 20-40 minutes. The trade-off is custody concentration in the Coinbase ecosystem versus fully self-sovereign control. For exploratory users learning what DeFi feels like, the lower-friction path is usually the right starting point; for users committing meaningful long-term capital, the hardware-wallet path is the right destination.

ZK L2 DeFi: Nascent But Growing

The ZK L2 DeFi picture in 2026 is an order of magnitude smaller than the OP-stack picture by total TVL, but real protocols with real liquidity exist on each major chain. The pace of DeFi protocol development on ZK L2s accelerated through 2025-2026 as the underlying chain ecosystems matured, and the picture below is worth tracking quarterly as TVL trajectories evolve. Pick a ZK L2 for DeFi when you specifically want the validity-proof security model, when you are experimenting with newer designs, or when you want exposure to the long-term ZK ecosystem development. For maximum liquidity depth on routine DeFi positions, OP-stack chains remain the deeper-liquidity choice.

Practical sequencing for users new to ZK L2s: spend your first few hours on testnet (no real capital at stake), then deploy a small test amount through the canonical bridge to verify wallet integration, only then scale to meaningful position size after the operational mechanics feel routine. The user-flow differences between EVM L2s and Cairo-native Starknet are larger than they appear in documentation. Wallet setup, address format, signing prompts and protocol approval patterns all differ meaningfully on Starknet versus the EVM-compatible alternatives.

zkSync Era — SyncSwap

SyncSwap is the most active DEX on zkSync Era with TVL in the single-digit-millions range directly on Era plus additional cross-chain deployment. The protocol uses concentrated-liquidity primitives and has been a steady presence on zkSync Era since the chain's mainnet launch. For mainstream pair swaps on Era (ETH/USDC, ZK/USDC), SyncSwap is the default.

The trade-off is that liquidity depth is meaningfully smaller than OP-stack DEXes — large trades may have visible slippage that the same trade on Arbitrum or Base would not have. A concrete sizing rule: under $5,000 per trade, SyncSwap on Era will execute close to spot; between $5,000 and $20,000, expect mild slippage in the 0.1 to 0.5 per cent range depending on pair; above $20,000 you should split the order across multiple smaller fills or route through a mainstream OP-stack DEX instead. The same trade-off applies for any L2 DEX where TVL is meaningfully smaller than the per-trade size you want to execute.

Linea — ramping but limited

Linea's DeFi ecosystem is limited as of mid-2026. ConsenSys-ecosystem deployments are ramping but have not reached OP-stack scale. The Q1 2026 Type-1 zkEVM upgrade improved Linea's EVM-equivalence story and is gradually attracting more deployments, but the practical DeFi picture is still smaller than zkSync Era's. Pick Linea for deployments where you want true EVM equivalence and are willing to operate with smaller liquidity pools; for routine DeFi, the OP-stack chains and zkSync Era both offer deeper venues.

Starknet — Cairo-native ecosystem

Starknet uses the Cairo virtual machine, not the EVM, so the DeFi tooling is genuinely different. The main Cairo-native protocols include Ekubo (concentrated-liquidity AMM, Starknet-native design) and JediSwap (Uniswap V2-equivalent, Cairo-native). Starknet's total TVL remains under $200 million as of mid-2026, much smaller than the OP-stack peers. The chain's account-abstraction-native design produces cleaner application-level UX (gasless transactions paid in arbitrary tokens, social recovery as a default) that EVM L2s require ERC-4337 plumbing to match.

Pick Starknet for applications that benefit from Cairo's specific properties (account abstraction, computation-heavy workloads, novel cryptographic primitives) or for ZK ecosystem support. The trade-off is the smaller liquidity pool, the Cairo learning curve for developers, and the wallet-incompatibility (Argent X and Braavos are the standard Starknet wallets — your MetaMask address does not work on Starknet directly). A practical sizing rule for Starknet: under $1,000 you can experiment freely, the friction is part of the learning; between $1,000 and $10,000 you should run a small test transaction first to confirm wallet-flow and AA-paymaster behaviour; above $10,000 the position should be a deliberate Starknet-specific bet rather than a routine DeFi allocation, given the meaningfully smaller liquidity pool and different recovery story compared to EVM L2s.

Scroll — contracted

Scroll's DeFi ecosystem contracted significantly through 2024-2026 alongside the chain's TVL collapse, and Scroll is not currently recommended for new DeFi deployments. If you have existing Scroll positions, monitor the chain's status pages and DefiLlama TVL trajectory; if you are deciding where to deploy new capital, the other ZK L2s above are the better starting points.

ZK L2 capital allocation considerations

The ZK L2 protocol picture is genuinely younger than the OP-stack picture, and the practical implication is sizing discipline. A working rule for ZK L2 DeFi capital: do not allocate more to any single ZK L2 protocol than you would allocate to an early-stage application on Ethereum mainnet, because the protocol-side maturity gap is meaningful. SyncSwap on zkSync Era has the longest production track record amongst the ZK DEXs covered, but its single-digit-million TVL means any large trade visibly moves price. Linea protocols are mostly in early-deployment phase as of mid-2026 with shorter audit-and-incident histories. Starknet's Cairo-native protocols (Ekubo, JediSwap) are the most distinctive technically but operate at smaller TVL and have a smaller pool of independent security researchers than the EVM-compatible DEXes.

For an ETH-denominated position holder considering ZK L2 deployment, the cleaner framing is exposure-first not yield-first. You allocate to a ZK L2 because you want exposure to that chain's ecosystem trajectory, want to support a specific technical direction (Cairo, MetaMask-native onboarding), or want a small hedge against OP-stack concentration. Pure yield-chasing on ZK L2s usually leads you back to the OP-stack chains because the deeper liquidity venues offer better risk-adjusted rates at any meaningful size. Sizing rule: keep total ZK L2 DeFi exposure under 20 per cent of your DeFi portfolio for the typical retail user until the ZK ecosystems mature past the current TVL gap.

Cross-L2 DeFi Strategies

Most DeFi users start with a single L2 and stay there. The single-L2 approach is the right default for capital under roughly $50,000 — the simplicity is worth more than the marginal optimisation from spreading across chains, and the operational overhead of bridging multiple times per month adds up in both fee and attention costs. Multi-L2 deployment makes sense when you have a specific reason to use protocols that live on different chains, when you want to hedge L2-specific risk, or when capital size makes the diversification meaningful.

When multi-L2 is right

The strongest reason for multi-L2 deployment is protocol-specific liquidity. If you want to run perps on GMX (Arbitrum) and synthetic-asset exposure on Synthetix (Optimism), you cannot avoid being on both chains — the protocols are L2-specific. Similarly, if you want significant Aerodrome veAERO governance exposure (Base) plus a separate Aave Arbitrum lending position, the protocols live on different chains and bridging the assets is the unavoidable cost of accessing both.

The second reason is L2-specific risk hedging. Holding 100 per cent of your DeFi capital on a single L2 concentrates the exposure to that chain's sequencer reliability, security council, governance and commercial sustainability. Spreading across two or three L2s reduces the concentration. For long-horizon positions in particular, this hedge is worth the bridging cost.

When single-L2 is right

Single-L2 focus is the right default for smaller positions, for fee-sensitive workflows, and for users who value operational simplicity. The bridging cost (both in dollars and in attention) is non-trivial for users moving funds frequently, and the diversification benefit is small until the position size is large enough that single-chain concentration starts to matter. For most retail users with under $50,000 in DeFi capital, pick the L2 that best fits your primary strategy and stay there. A specific dollar example: at $20,000 deployed entirely on Arbitrum, the operational overhead is roughly $40 per year in periodic transaction fees and perhaps two hours of monitoring time across a year.

The same $20,000 split 60/40 across Arbitrum and Optimism roughly doubles both the operational fees and the monitoring overhead while adding modest diversification benefit. The trade is rarely worth it at this size unless you have a specific protocol-availability reason to be on both chains.

Three concrete cross-L2 scenarios

Scenario one — the active perps trader with a synthetic-asset position. You allocate $20,000 to perps trading on Arbitrum (GMX V2 for the depth) and $8,000 to a Synthetix synthetic-commodity position on Optimism. The two positions serve different strategic purposes: perps is your active leveraged exposure, synthetic gold is your defensive hedge. Bridging between them happens only when you rebalance — perhaps quarterly, at a one-time fast-bridge cost in the $20-$40 range per crossing. Annual operational overhead: roughly $80-$160 in bridge fees plus a few hours of monitoring across two chains. Worth it because the protocol availability is the determining factor; neither position has a viable single-chain substitute.

Scenario two — the Base-anchored DeFi user dabbling in Arbitrum perps. You hold $30,000 of liquidity on Aerodrome (Base) earning emissions plus trading-fee revenue. You also want to run a small $3,000 perps experiment on GMX (Arbitrum) — not a major position, just learning the venue. The $3,000 spent on perps and the $30,000 LP position do not need to interact. Bridge $3,000 once, run the experiment, decide later if you want to scale up. The bridging cost on $3,000 at the 0.1 per cent fast-bridge fee is about $3 — trivial relative to the learning value. The mistake here would be over-bridging: do not move LP capital between chains chasing yield differentials of a few basis points; the bridging cost will eat the marginal yield within weeks.

Scenario three — the conservative diversifier with three-chain exposure. You hold $90,000 of DeFi capital and want to limit single-chain concentration risk for the long term. A three-chain allocation might land at $40,000 Arbitrum (Aave lending plus a small GMX position), $30,000 Optimism (Synthetix derivatives plus Aave), and $20,000 Base (Aerodrome veAERO governance plus Aave). Each chain hosts complementary protocols. Annual operational overhead climbs to roughly $300-$500 in periodic bridge and gas fees plus perhaps eight hours of monitoring across three status pages and three DefiLlama dashboards. At $90,000 capital, that overhead is fractional and the concentration-risk reduction is meaningful. Three chains is roughly the upper limit before operational complexity overwhelms the diversification benefit — beyond three chains, the marginal hedge benefit shrinks while the monitoring overhead compounds.

Decision tree

The practical decision tree: if your primary strategy is perps and yield, pick Arbitrum. If your primary strategy is derivatives or you specifically want the Synthetix model, pick Optimism. If your primary strategy involves Aerodrome veAERO or you are onboarding through Coinbase, pick Base. If your primary strategy involves ZK-specific design (account-abstraction-native applications, Cairo-native protocols), pick the relevant ZK L2 — Starknet for AA-native, zkSync Era for the broader EVM-compatible ZK DeFi.

If your strategy spans multiple of the above, you are in multi-L2 territory and should explicitly budget the bridging cost as part of the strategy's expected return. A concrete sizing rule: if you bridge $5,000 of USDC across the OP-stack family (Arbitrum → Optimism → Base) once a month using a fast-bridge service, you should budget roughly $15-$30 per month in bridge fees plus the L2 gas overhead — call it $25 per month total, or about $300 per year.

If your multi-L2 strategy's expected excess return over the single-L2 alternative is less than $300 per year on a $5,000 position, you are paying friction without capturing the benefit. The multi-L2 setup makes sense above roughly $20,000-$50,000 position size where the fee fraction shrinks and the diversification benefit grows. For the cross-L2 fee economics — what bridging actually costs, canonical vs third-party bridge trade-offs, withdrawal mechanics — see our L2 fees and bridging satellite.

Common L2 DeFi mistakes

Three recurring mistakes show up across new and experienced L2 DeFi users. First, chasing the highest advertised APY without checking the underlying protocol audit and operational track record. A 25 per cent APY on a six-month-old protocol with one audit carries materially more tail risk than an 8 per cent APY on Aave with five years of production track record and many independent audits. Match yield expectations to protocol maturity; if you cannot explain the source of yield in one paragraph, the yield is probably riskier than it appears.

Second, bridging the same capital repeatedly chasing small yield differentials. A 0.5 per cent APY differential between Aave on Arbitrum versus Aave on Optimism does not justify a $20-$30 bridging round-trip cost on positions under $20,000. Move capital between chains based on protocol-availability decisions, not on rate-shopping. Third, treating L2-specific governance tokens (ARB, OP, AERO) as primary investment exposure rather than as governance utility. Token-emission yields can be attractive in the short term but the tokens often face structural inflation pressure that erodes long-term value; size governance-token positions accordingly.

Conclusion

The 2026 per-L2 DeFi picture is structurally settled around four practical families. Arbitrum is the perps-and-yield L2 anchored by GMX V2, Camelot V3 and Aave. Pick it for active perps trading and yield-farming workflows. Optimism is the derivatives-and-lending L2 anchored by Synthetix, Aave and Uniswap. Pick it for synthetic-asset exposure and Synthetix-specific design. Base is the fastest-growing DEX hub anchored by Aerodrome (and the Velodrome-to-Aerodrome consolidation), plus the Coinbase smart-wallet onboarding advantage. Pick it for ve(3,3) emissions exposure and for new-user onboarding via passkey wallets. The ZK L2s (zkSync Era, Linea, Starknet) are an order of magnitude smaller for DeFi but watchable. Starknet stands out for account-abstraction-native applications.

This is a 2026 snapshot. The landscape genuinely shifts every six months at the level of detail that matters for capital deployment. Treat this guide as accurate at the time of writing and re-verify against DefiLlama and L2BEAT before any large deployment. The 2027 refresh will live at a parallel URL with the same per-L2 structure and an updated protocol picture.

Risks worth weighting. DeFi protocols carry smart contract risk — a vulnerability or upgrade bug can cause partial or total loss of deposited capital regardless of which L2 hosts the protocol. Leveraged positions on perps venues like GMX or Synthetix carry liquidation risk if the underlying asset moves against you past your maintenance margin. Liquidity provision on AMMs like Aerodrome or Camelot exposes you to impermanent loss when the pair ratio shifts, especially on volatile token pairs. Stablecoin deposits are not risk-free either: a depeg event (USDC March 2023 dropped to $0.88, UST May 2022 collapsed to zero) can erase value before you have time to exit. Size positions accordingly and never deploy capital you cannot afford to write down.

A practical monitoring cadence: check DefiLlama for the L2 chains you hold capital on once per quarter (about ten minutes) — look at TVL trajectory, top-protocol concentration, and any new entrants. Check L2BEAT for stage progressions on the same L2s once per quarter (another ten minutes) — Stage 0 → Stage 1 transitions are leading signals of maturity, and security-council changes can shift your trust assumptions. Cross-reference any protocol you have meaningful capital in with its own status page and team Twitter at the same cadence. Twenty minutes per quarter is the realistic monitoring overhead for staying current with a multi-L2 DeFi position; you should budget it as a recurring task rather than as an ad-hoc check during stressful events.

Key takeaways:

- Pick Arbitrum for active perps trading and yield-farming workflows anchored by GMX V2, Camelot V3 and Aave

- Pick Optimism for synthetic-asset exposure and lending — the Synthetix-and-Aave depth is the centre of gravity

- Pick Base for ve(3,3) emissions exposure via Aerodrome and for new-user onboarding via Coinbase smart wallet

- Treat ZK L2 DeFi as watchable rather than allocatable today; the TVL gap is an order of magnitude and integration tooling lags

- Re-verify against DefiLlama and L2BEAT before any large deployment — the landscape shifts every six months at the level of detail that matters

For the broader L2 selection framework — chain selection considerations beyond DeFi protocol specifics — return to the Ethereum L2 complete guide. For the fee and bridging mechanics that underlie cross-L2 strategy decisions, see our L2 fees and bridging satellite. For the security analysis that informs single-vs-multi-L2 deployment decisions, see our L2 security tradeoffs satellite.

Sources

- DefiLlama — L2 / rollup chains: live TVL data per L2 chain. The primary source for verifying the per-L2 protocol-and-liquidity picture in this guide.

- L2BEAT — scaling summary: neutral L2 reference for chain-level economics, stage progression and security comparisons.

- DefiLlama — GMX protocol page: live TVL and volume data for GMX V2 on Arbitrum.

- DefiLlama — Aerodrome protocol page: live TVL data for Aerodrome on Base.

- DefiLlama — Synthetix protocol page: live data for Synthetix on Optimism, including debt pool size and protocol revenue.

Frequently Asked Questions

- Which L2 has the deepest DeFi liquidity?

- Arbitrum and Optimism by total TVL as of mid-2026. Arbitrum leads on perps liquidity (GMX, Camelot) and yield. Optimism leads on derivatives (Synthetix) and lending (Aave). Base is the fastest-growing L2 by DeFi metrics — Aerodrome alone holds the majority of Base DEX liquidity. ZK L2 DeFi remains an order of magnitude smaller than OP-stack DeFi by total TVL, with SyncSwap on zkSync Era as the most active ZK DEX. For deepest immediate liquidity on any specific asset, check DefiLlama directly — the picture shifts every few months.

- Should I use perps on Arbitrum or Optimism?

- Pick Arbitrum (GMX) for perps on crypto majors and altcoins — the GMX V2 perps engine is the deepest L2 perps liquidity venue with broad pair coverage. Pick Synthetix on Optimism for synthetic-asset exposure and for certain perps pairs that benefit from Synthetix's debt-pool architecture. The two are complementary rather than competitive — many active L2 perps traders hold positions on both. For execution-quality on the largest crypto pairs, Arbitrum GMX is the default. For exotic pairs or for users who specifically want the Synthetix model, Optimism is the pick.

- Why is Velodrome merging into Aerodrome?

- The merger consolidates ve(3,3) liquidity infrastructure across the OP Superchain into a single token (AERO) on Base, with Aerodrome as the surviving entity. Velodrome pioneered the ve(3,3) model on Optimism and ran successfully for several years; the merger reflects the Superchain coordination thesis (single liquidity venue for shared OP-stack chains) and the empirical reality that Base accumulated the larger DEX-side TVL by 2025-2026. VELO holders received 5.5 per cent AERO during the merger as the conversion mechanic. For Base-side DEX activity in 2026, Aerodrome is the entity to use — Velodrome is no longer an active recommendation.

- Are ZK L2 DeFi protocols mature enough to use?

- Depends on what you want to use. SyncSwap on zkSync Era has real liquidity in the single-digit-millions range and is the most active ZK DEX. Linea has limited mature DeFi as of mid-2026 — ConsenSys ecosystem deployments are ramping but not yet at OP-stack scale. Starknet has Cairo-native protocols (Ekubo, JediSwap) with smaller TVL and different tooling than EVM L2s. For routine DeFi positions (lending, swap, yield), OP-stack chains are the deeper-liquidity choice. For experimentation with newer designs or for chains you specifically want to support, ZK L2s are watchable but should be sized smaller than OP-stack positions.

- Why doesn't this guide cover Polygon zkEVM DeFi?

- Polygon zkEVM Mainnet Beta sunsets on 1 July 2026. We do not recommend deploying DeFi capital on a sunsetting L2. Funds locked in DeFi protocols at the sunset deadline cannot be reclaimed through the migration path because those protocols themselves stop processing transactions. Externally-owned account balances on Polygon zkEVM will migrate to Ethereum L1 through the official claim guide, but DeFi-locked capital is a different story. If you currently have DeFi positions on Polygon zkEVM, exit before the deadline. For the broader sunset context, see our L2 security tradeoffs satellite.

- Can I use the same wallet for DeFi across multiple L2s?

- Yes for every EVM L2 — Arbitrum, Optimism, Base, zkSync Era, Linea all use the same Ethereum-style address as your mainnet wallet, so you can reuse your MetaMask (or hardware wallet) address across all of them. You need to add each L2's network configuration to your wallet separately (chain ID, RPC URL, currency symbol, explorer URL). Starknet is the exception — the Cairo VM uses a different address format, so a Starknet wallet is technically distinct (Argent X and Braavos are the standard Starknet wallets). For OP-stack and ZK-EVM chains, one wallet covers all of them.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.