Crypto Inheritance with Multisig: Estate Planning, Keys Intact

A multisig lets you plan crypto inheritance without surrendering keys while alive — e.g. a 2-of-3 where you hold two keys and a lawyer or heir holds one, or a collaborative-custody service holds a recovery key. Most self-custody plans collapse at the point of handover: the heir cannot reconstruct the wallet, the seed phrase was never tested, or the executor does not know which coordinator software to open. Multisig changes the geometry of the problem. This guide covers the three key-distribution patterns that actually survive a death event, the documentation that supports them, the collaborative-custody role as a recovery partner, and the pitfalls that quietly defeat the whole exercise.

Introduction

Most readers arrive at "crypto inheritance" with a specific worry. They have built a self-custody stack — a hardware wallet, maybe several, a careful seed-phrase backup, perhaps a passphrase — and they cannot answer the question "what happens to this if I die tomorrow." The conventional answers all break in different ways. Hand the seed to a spouse and you have created a single point of failure for your living finances. Put the seed in a will and you have published it to whoever reads the will. Drop the seed into a safe-deposit box and you have introduced jurisdictional access delays, no testability path, and a bank employee who could in principle photograph the contents during a routine inspection.

Multisig changes the geometry of the problem. Instead of one piece of paper that grants total authority once revealed, you split authority across M-of-N keys held by different parties in different places, none of whom can move funds unilaterally — including yourself, in a 2-of-3 you no longer have a single device that can drain the wallet. The same property that makes multisig attractive for hot operational security (no single device compromise drains funds) is the property you want for inheritance: authority that cannot be unilaterally exercised while you are alive, yet can be reconstituted after a custodial event with appropriate documented release. That sentence is the entire architectural thesis of this guide. The rest of the page covers how to instantiate it.

This is a satellite of the C8 multisig cluster. It does not re-explain M-of-N mechanics — for the conceptual basis (how thresholds combine into a signature, why 2-of-3 versus 3-of-5, the BTC versus EVM mechanism difference), the cluster's multisig wallets complete guide owns the conceptual model (linked below in conclusion and related-resources). It does not walk through the operational setup of a Bitcoin multisig in Sparrow or Nunchuk, nor the deployment of a Safe contract on EVM — those operational walkthroughs live in the BTC setup and Safe setup satellites of this cluster. And before any of this applies cleanly, the underlying single-key hygiene has to be solid: see the single-key baseline before multisig custody for the C4 hygiene layer that sits beneath everything here.

What this page covers, in order:

- the inheritance problem in self-custody (why the conventional answers fail);

- the three numbered key-distribution patterns that actually work in practice (Pattern A self-plus-lawyer-plus-heir, Pattern B self-plus-heir-plus-collaborative-custody, Pattern C distributed family 3-of-5);

- collaborative-custody services as a recovery-key holder, including a candid framing of what you trade for what you get;

- the documentation and legal handover practices that make any of the patterns operable;

- and the heir-operability pitfalls that defeat well-built setups in the moment they matter.

The patterns are decision options rather than rankings — match the pattern to your holdings size, family complexity, and heir technical fluency. Each pattern has trade-offs, none of them is universally correct, and switching between them is a routine operation once the underlying multisig is in place.

The Inheritance Problem in Self-Custody

Run the thought experiment cleanly before any of the patterns make sense. You hold Bitcoin or Ethereum on a hardware wallet. The seed phrase is on a steel backup in a fireproof safe in your home, the passphrase is in your memory, and the daily-driver device is on your desk. You die tomorrow morning — heart attack, traffic accident, the routine failure modes of being mortal. What happens to the stack?

Without inheritance planning, the funds are functionally lost. The seed phrase is in your safe but nobody who survives you knows it is there, knows what it does, or knows what hardware to pair it with. The passphrase that gates the wallet is not written down anywhere; it died with you. The daily-driver device is bricked or PIN-locked, and even if your heir guesses the PIN, the passphrase prompt means the wallet they see is empty. Forensically the keys still exist in a probabilistic sense (the seed words are still on the steel) but operationally the funds are unreachable. The literature on lost cryptocurrency includes estimates in the millions of BTC that fit this exact profile — the holder died and the people who survived them could not assemble what they needed.

The conventional answers each break in a specific way. Spell them out so the multisig framing is calibrated against the alternatives rather than presented in isolation. The patterns later in the guide are a direct response to each failure mode below.

Failure mode one: seed known to no-one

The default configuration for a careful self-custodian. The seed lives on a steel backup, the passphrase lives in memory, the device sits on the desk. Operational security during life is excellent; inheritance probability is zero. Your heirs will eventually search the house, find an unmarked piece of steel with twenty-four English words on it, and have no idea what it does or how to use it. The cryptography is intact; the operability is gone. This is the failure mode that estate planning attempts to fix, and almost every fix introduces its own problem.

Failure mode two: seed shared with the heir while alive

The intuitive response: tell the heir what the seed is and where it lives, so they can use it when needed. The problem is structural rather than about trust. A seed phrase is total authority once it leaves your control. The heir can in principle sweep the wallet today, before any custodial event. You may trust them completely, and the trust may even be warranted, but you have replaced an inheritance plan with a permission for unilateral action. Real risks compound: heir compromise (their device is hacked, their cloud backup is breached, their notes are photographed), marital dispute (the heir is your spouse, and your relationship changes), joint accident (you die in the same car crash, and the seed is now in the same probate process you tried to avoid), or non-technical heir mishandling (they copy the seed into a phone notes app to remember it). The plan does not survive the first thing going slightly wrong.

Failure mode three: seed in a safe-deposit box

Better operational hygiene than handing the seed to a person, worse than it appears. Bank access on death is legally slow and jurisdiction-dependent — in many places the executor needs a court order or a death certificate plus a multi-week wait before the box is opened, and the contents are sometimes inventoried in the presence of a bank employee. The seed is then visible to whoever is present at the opening. There is no testing path while you are alive: you cannot rehearse the handover without periodically retrieving the seed, photographing the box, or otherwise creating exposure. And the seed, once retrieved, is again total authority — the same single-point-of-failure as failure mode two, just with a slower trigger.

Failure mode four: seed in a will

The legally-formal version of failure mode two. A will is read by at least the probate lawyer, often a court clerk, sometimes copies are filed in registries that human beings can in principle access. The will sits in a drawer or registry between the day you sign it and the day it is read — that window is months to decades, with no procedure for testing that the seed still works inside it. If you rotate the seed (a perfectly normal operational-security move) the will is now stale, and updating it requires a fresh legal instrument. The cryptography is fine; the legal envelope is operationally hostile to confidential cryptographic material.

Failure mode five: "just trust your spouse"

Some variant of "my wife knows where the seed is" or "my husband has the device." The plan survives until something inside your relationship changes. Joint accidents end both of you at the same time, leaving the same forensic-loss problem as failure mode one. Divorce splits the seed between two adversaries — a seed phrase cannot be partly assigned in a settlement, and the spouse who left now has total authority. Estrangement, dementia, or a serious illness on the spouse's side moves authority to a person no longer in a position to safeguard it. Trust is a real input to inheritance planning, but a plan that depends on a single relationship surviving every imaginable event is brittle by construction.

What you want is a property that none of the five failure modes deliver: authority that cannot be unilaterally exercised while you are alive, but can be reconstituted after a death event with appropriate documented release. M-of-N multisig delivers this structurally rather than as a procedural promise. The threshold blocks unilateral action by design; the documented release process for the third key (lawyer, service, or designated trustee) handles the post-event reconstitution; and the wallet remains operational every day in between because you can still sign with your M keys. The rest of the guide is the operational instantiation of that property in three patterns.

Multisig Key-Distribution Patterns

Three patterns cover the vast majority of practical inheritance setups. They are presented as numbered decision options rather than as rankings — none of them is universally correct, and the right pattern for you depends on your holdings size, family complexity, heir technical fluency, and willingness to pay an ongoing service fee for a third party in the loop. Read all three before picking; the trade-offs are different in kind, not just degree.

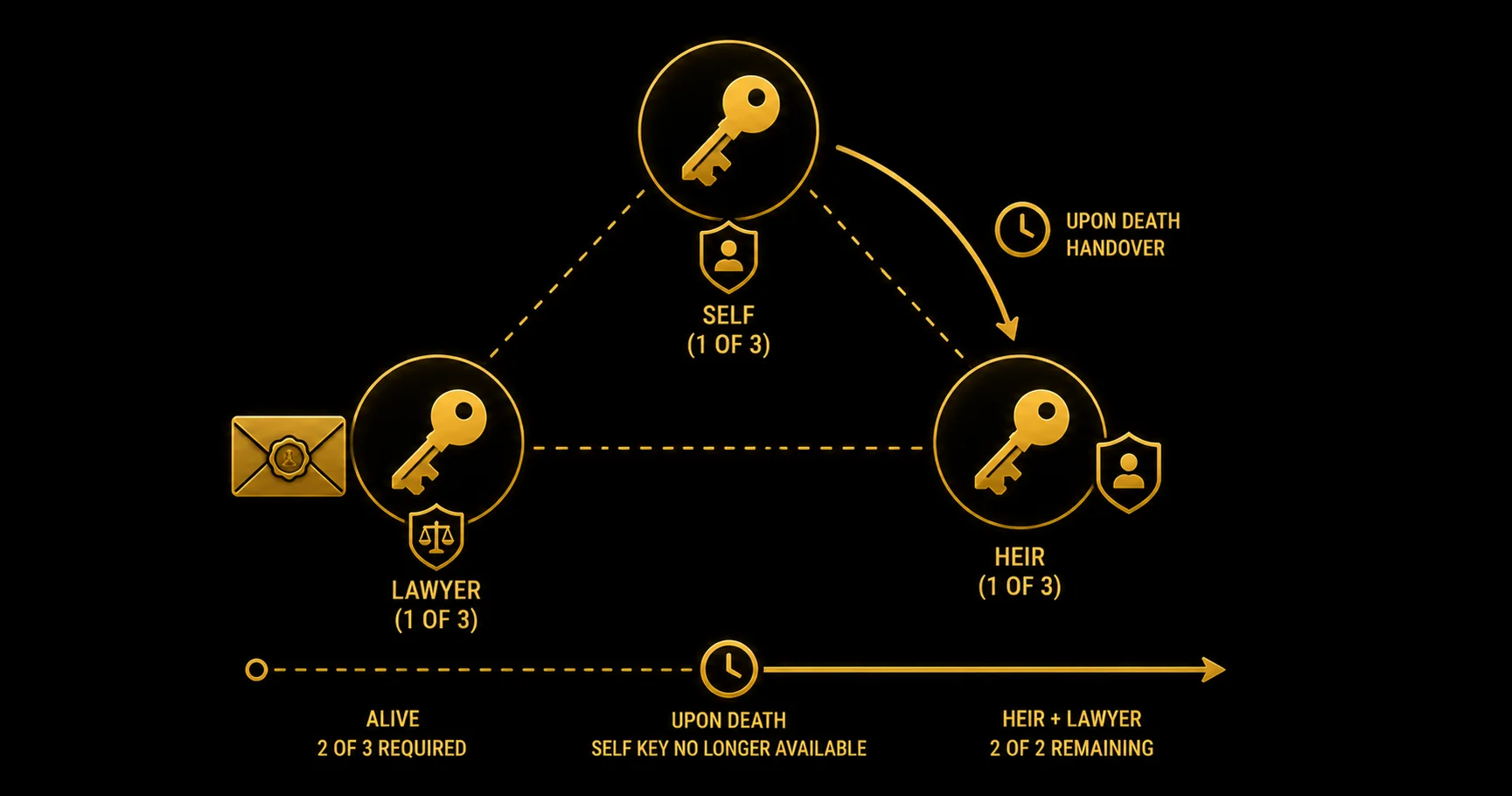

Pattern A — Self + lawyer + heir (2-of-3)

Configuration: you hold two keys (e.g. Keystone 3 Pro and Trezor Safe 7 at two different physical locations — home safe and a separate off-site location); a law firm holds one (sealed envelope or HSM, with release conditional on a death certificate and the engagement letter you signed when you set up the arrangement); the heir holds zero keys during your life.

During life: you sign with your two keys for every routine transaction. The lawyer's key never moves; it sits in the firm's secure storage and is not used in any signing flow. You operate the wallet exactly the way you would operate any 2-of-3 multisig where the third key is a backup — for every spend, you produce two signatures and the threshold is satisfied without any external coordination. The heir is uninvolved in operational flows entirely, which is exactly the point: nothing they do or fail to do affects your living finances.

Handover: on a custodial event, your executor receives the second of your two keys via the estate (you have documented where the device lives and what the unlock procedure is, in the same sealed-envelope packet that goes to the lawyer). The executor contacts the law firm and triggers the release procedure — death certificate, identity verification, the procedural artefacts the firm specified in the engagement letter. The law firm releases their key. The heir now has two keys, combines them in the named coordinator software, signs a recovery transaction to a wallet they control, and the inheritance is complete.

Variation: in some setups the heir holds one key from day one (their own hardware signer that they keep at their own home), and the lawyer's key serves as a recovery backstop only if either you lose one of your two keys or the heir loses theirs. The threshold is still 2-of-3; what changes is who holds the keys during your life. The variation makes the dry-run rule (covered later) easier because the heir's signer is already configured and tested.

Trade-offs: the strongest dependency is on the law firm's institutional continuity. A 2-of-3 set up with a small firm whose partner you trust in 2026 may have moved firms, retired, or been acquired by a larger practice in 2046. Build the firm-continuity clause into the engagement letter — what happens if the partner you engaged retires, what happens if the firm dissolves, what is the named successor — and confirm it annually. Crypto literacy varies across firms: some have estate-planning practices fluent in digital assets, some treat your sealed envelope as opaque paperwork and would not notice if it changed contents during a routine office move. Probe before you engage. The fee structure is typically a one-off setup charge plus an annual storage fee; both are modest compared with a collaborative-custody subscription, and the firm's role is much narrower (storage and release, not active multisig signing).

Pattern B — Self + heir + collaborative-custody service (2-of-3)

Configuration: you hold one key (a daily-driver hardware signer that you use for routine transactions); the heir holds one key (their own hardware signer, configured and tested while you are alive — see the heir-operability section); a collaborative-custody service holds the third as a recovery key. The service is not in the daily signing path; their key is for inheritance and disaster-recovery scenarios.

During life: you and the service co-sign for routine moves. The service runs verification on their side — checking that the request comes from you, looking at on-chain context, possibly enforcing time delays on large transactions — and signs on a documented schedule. The heir's key is uninvolved in operational flows; it is the inheritance backstop. The relationship is closer to an active multisig than Pattern A's purely-archival lawyer role: the service is in your routine signing loop, which means service uptime and quality matter to your daily operations, not just to your inheritance plan.

Handover: on a custodial event, the executor follows the service's documented inheritance procedure — typically a combination of death certificate, identity verification on the heir's side, and a procedural delay built into the service's inheritance product. The service releases their key (or signs a recovery transaction on the heir's behalf, depending on the service's specific architecture). The heir combines the service's released key with their own pre-configured signer, signs a recovery transaction to a wallet they control, and the inheritance is complete. The holder's living-day key is no longer required for the handover — which is structurally why this pattern is robust to scenarios where the holder's primary device is lost or unrecoverable at the moment of need.

Trade-offs: ongoing service fees are real and recurring (paid services with tiered pricing). Third-party trust is the more substantive consideration: the service must outlive you (institutional longevity over a multi-decade horizon), honour its inheritance procedure (operational reliability), and be jurisdictionally appropriate for both you and the heir (their procedures interact with the legal frameworks of the places involved). The flip side is that the service replaces a personal-relationship dependency with a contractual one — Pattern A depends on a law firm partner, Pattern B depends on a service-as-institution. Which dependency you prefer is a judgement about which kind of entity you trust more to be operating in twenty or forty years.

Pattern C — Distributed family (3-of-5)

Configuration: you hold two keys (at two different physical locations); two family members hold one key each (typically adult children, siblings, or a trusted parent-figure); a lawyer or institutional trustee holds the fifth. The threshold is 3-of-5 — any three of the five suffice to sign a transaction.

During life: you spend with your two keys plus one family member's key. No single relative has unilateral power because no single relative reaches the threshold alone; the involvement of one family member in each transaction is the daily signing pattern. This is more operational friction than Patterns A or B — coordinating three signatures per transaction (yours, yours, one family member's) is meaningfully heavier than two — but it is the price of the structural property that any three of the five reconstruct authority.

Handover: after a custodial event, any three of the surviving four signers reconstitute authority. The pattern is structurally robust to family-member loss (two of the four can still cover the threshold), to family conflict (the lawyer's key plus two family members can sign over the objection of any third party), and to law-firm continuity issues (three family members can sign without the lawyer's key). The handover does not depend on any single relationship surviving intact — which is precisely the multi-generational planning property that makes this pattern attractive for larger holdings or complex family dynamics.

Trade-offs: operational complexity is the largest cost — three signatures per transaction, more signer devices to maintain, more end-to-end testing to do. Attack surface grows with signer count: a 3-of-5 has five seed phrases to compromise rather than three, even though the threshold is higher. Family member fluency varies and turns key-management into a multi-generational education project. End-to-end testing of inheritance scenarios across five parties is heavier than testing across three. Best fit: larger holdings where the structural robustness is worth the operational tax, multi-generational planning where the wallet will outlive multiple key-holders, and family configurations where no single party should have outsized custody power.

Pattern A Worked Example — The Handover Walkthrough

Abstract pattern descriptions only become legible when you walk one through end-to-end. The sequence below is Pattern A at the moment of a custodial event — what actually happens, in order, from the day the death certificate is issued to the day the heir holds the funds. Treat this as the script you rehearse with your lawyer and your heir while alive, not as legal advice for any specific jurisdiction.

Day zero: the custodial event. The holder dies. The standard probate process begins on the legal side — executor named, estate opened, death certificate issued by the relevant civil registry. Crypto inheritance is one workstream inside the broader estate process, not a parallel track.

Day one to seven: executor inventory. The executor opens the sealed handover document the holder left with their personal effects (often stored alongside other key estate paperwork — passport, deeds, insurance policies). The document names the multisig wallet, the coordinator software (Sparrow for Bitcoin, Safe{Wallet} for EVM, Nunchuk for either), the chain or chains involved, the descriptor (BTC) or contract address (EVM) — all of which are public information — and the location of the holder's two signer devices. The document also names the law firm holding the third key and the partner-of-record. None of this includes a seed phrase; everything is descriptor-level or contract-level.

Day seven to fourteen: lawyer release process. The executor contacts the named partner at the law firm with a certified copy of the death certificate, identity documents, and the executor's letters of authority (or jurisdictional equivalent). The law firm follows the release procedure documented in the original engagement letter — typically a verification step where they confirm the death and the executor's authority, a waiting period built into the engagement to prevent rushed handovers, and a logged retrieval of the sealed key from secure storage. The law firm delivers the third key to the executor in the form pre-agreed (sealed envelope, encrypted USB stick handed in person, or another firm-specific method).

Day fourteen to twenty-one: heir setup. The executor delivers the second of the holder's two signer devices to the heir along with the sealed envelope from the law firm and the original handover document. The heir takes everything to a quiet workstation — air-gapped if they have the operational fluency, otherwise a freshly-imaged laptop running an offline OS — and installs the named coordinator software. They load the descriptor (BTC) or the Safe contract address (EVM) into the coordinator. For Bitcoin, the descriptor is a single line of text that names everything the coordinator needs to find the wallet: the script type wrapper (wsh(...) for P2WSH SegWit, or tr(...) for Taproot), the multisig predicate (sortedmulti(M, xpub1, xpub2, xpub3)), and the derivation path at which each xpub lives (typically the BIP 48 multisig path, e.g. m/48'/0'/0'/2' for P2WSH or m/48'/0'/0'/3' for Taproot). For EVM, the equivalent is just the Safe contract address plus the chain ID. The coordinator reads the descriptor or address and displays the multisig wallet read-only — read-only because the xpubs in the descriptor can derive every receive address the wallet has ever used, which is what reveals the balance, but they cannot sign. Signatures require private keys. The funds are visible; the threshold is not yet met because only the public-side material is loaded.

Day twenty-one to twenty-eight: recovery transaction. The heir connects the holder's second signer and the released third key (the lawyer's sealed envelope contents) to the coordinator. They construct a recovery transaction — moving the full balance to a new wallet they alone control, on a fresh seed-phrase-and-device that has nothing to do with the old multisig. They sign with the holder's device, sign with the released key, the threshold is met at 2-of-3, the transaction is broadcast. After confirmations, the funds are in the heir's new wallet and the original multisig is empty. The inheritance is operationally complete.

What the walkthrough surfaces: there is no moment that requires the heir to be improvising. Every step has a documented input (a device, a sealed envelope, a coordinator software name) and a documented output (a loaded wallet, a signed transaction, a broadcast confirmation). The dry-run rule — covered in the heir-operability section — is the discipline that makes this sequence work in practice. An heir who has rehearsed each step while you are alive can run the entire sequence in two or three evenings of focused work; an heir doing it for the first time during a grief scenario will get stuck on the coordinator software's UX before they reach the signing flow.

Collaborative Custody as a Recovery Partner

Collaborative-custody services occupy a specific architectural role in Pattern B and adjacent setups: they participate in an M-of-N as a key-holder, where the client retains enough keys to spend without them. Casa and Unchained are the two services that dominate the practical inheritance discussion in 2026; both are paid third-party collaborative-custody services where you trust the recovery key to an external party. That framing is the honest one — no euphemism, no marketing softening. The trade-offs are real, and so are the gains; the section below names both without manufacturing risk warnings the services do not actually carry.

The architectural role

The service's key is the third position in a 2-of-3 (Casa's standard model) or the second of three in a hybrid arrangement (Unchained's standard model where the third key is held by an independent agent — see below). You always hold enough keys to spend without the service in routine operation. The service's key is the safety net: a recovery path if your primary signer is lost, a release path for heir access via the service's documented verification process, a tie-breaker for some kinds of family disputes if the service's procedures contemplate it.

What you trade is twofold. First, a service fee — paid services with tiered pricing from individual to institutional levels; specific dollar figures change frequently and live verification at the moment of purchase matters more than any figure I could quote here. Second, third-party trust: the service has to survive long enough to handover, honour its verification process on the day it matters, and remain jurisdictionally appropriate for both the holder and the heir. The combination is a specific kind of structured dependency — not custodial in the regulatory sense (you hold keys, they hold a key, neither party can unilaterally move funds), but contractual and operational in ways that a fully solo multisig is not.

What you gain is a counter-party that does not depend on personal relationships, has documented inheritance procedures vetted by their other clients' experiences over years, and survives family-circumstance changes (a divorce does not change the service's key custody, where a "the spouse holds the third key" arrangement very much would). For non-technical heirs, the service's verification staff are an actual resource to lean on during the handover — a contrast with Pattern A where the heir is in a quiet room with a coordinator software they have to operate alone.

Casa — multi-asset collaborative custody

Casa operates a multi-asset collaborative-custody model. The supported asset set expanded in 2026 to include Bitcoin, Ethereum, USDT, and USDC under their inheritance product per The Block's coverage of the global expansion. The standard architecture is a 2-of-3 in which the client holds two keys and Casa holds one recovery key; the client retains spending authority at all times and Casa's key activates in defined recovery or inheritance scenarios per their documented procedures. The service runs across tiered levels from individual users to institutions, with the inheritance feature included in the upper tiers.

Unchained — Bitcoin-only collaborative custody

Unchained operates a Bitcoin-only model with a structurally distinct three-party arrangement. The standard 2-of-3 vault has the client holding one key, Unchained holding one key, and an independent third-party agent holding the third. The independent-agent role is the architectural feature that distinguishes Unchained from a single-counterparty service: the third key is not held by Unchained itself, which structurally lowers the failure mode where the service-as-entity becomes the single point of trust. Adjacent services include Bitcoin-backed loans and Bitcoin retirement accounts (the latter under a Wyoming Charter banking arrangement), so for clients who want BTC-only collaborative custody plus adjacent financial services from the same provider, the surface area is wider than Casa's.

When paid collaborative custody is worth the fee

The pattern fits cleanly when one or more of the following applies. Holdings are large enough that a single device failure or family complication is catastrophic on its own terms — say, the value of the stack exceeds what you would be comfortable losing entirely through any single failure. The heir is non-technical and could not navigate Sparrow or Safe{Wallet} alone in a grief scenario, and you do not have a tech-fluent backup person in the family who could shepherd them through. The family is multi-jurisdictional, and probate complexity benefits structurally from a third party with documented procedures rather than a single-jurisdiction lawyer who may not be effective across borders. The holder travels frequently or lives in a high-risk region where personal storage of multiple signer devices carries non-trivial physical-security cost.

When it is not worth the fee

The pattern is overkill when one or more of the following applies. Holdings are small enough that an annual service fee meaningfully eats into the yield or growth on the underlying assets — at that scale, Pattern A with a modest lawyer engagement is structurally cheaper for the same inheritance property. The heir is tech-fluent and can demonstrably operate the coordinator alone (you have run the dry-run, multiple times, and the heir can rebuild the wallet from descriptor without prompting). The holder has a maximalist preference against any third-party participation in custody, even non-custodial collaborative arrangements where the service does not hold the threshold of keys.

The full service-level comparison — pricing tiers, asset coverage, jurisdictional notes, the architectural differences between Casa's single-counterparty model and Unchained's three-party model with the independent agent, the integration patterns with Safe for clients who want both — lives in the Safe vs Casa vs Unchained full comparison (linked in conclusion and related-resources). This page covers only the architectural role of the recovery-key holder in inheritance setups; the commercial comparison sits in the compare cluster.

Documentation and Legal Handover

The keys exist; the handover document explains what to do with them. Without the document, even a perfectly distributed 2-of-3 is operationally inert at the moment of need — the executor and heir know they are looking at "crypto stuff" and have no idea which coordinator to install, which descriptor to load, or which law firm holds the third key. The document closes that gap. It is a piece of plain-English instruction sitting alongside cryptographic material (public information mostly, no seed phrases, no private keys), and it is the most consistently neglected component of self-custody inheritance plans.

This is a technical primer, not legal advice. Estate-planning law, tax treatment of crypto assets, probate procedures, and the specific contractual arrangements with a law firm are all jurisdiction-dependent and change over time. Consult a lawyer in your jurisdiction for the legal framework; what follows is the technical content that lives inside that framework.

Sealed-envelope contents

The handover envelope (kept with the lawyer, in a safe-deposit box, or with a designated trustee) contains a small set of well-named items.

- The coordinator software list: which application to install for the wallet (Sparrow or Nunchuk for Bitcoin, Safe{Wallet} for EVM Safe contracts), the canonical download URL, and the GPG or PGP key fingerprint for verifying release signatures.

- The wallet descriptor (Bitcoin) or Safe contract address plus chain ID (EVM): public information that points the coordinator at the multisig wallet without revealing any private material.

- A plain-English explanation of which other key-holders exist, in what role, and how to contact them ("the law firm of [name] holds the third key; contact partner [name] or their successor at [address]" and similar for any collaborative-custody service).

- A "last verified working: [date]" stamp confirming the setup was operational at a known point in time, typically the date of the most recent annual review.

What the envelope does not contain: seed phrases, private keys, passwords, or PIN codes for any device. Those live with the keyholders themselves (you, on your steel backups; the law firm or service, in their secure storage). The envelope is informational rather than authoritative; it tells the heir how to find authority once they have legal standing, not how to bypass the verification process.

What the lawyer needs to know

The law firm holding the third key needs to understand that they are holding cryptographic material rather than just paperwork — there is no casual reading or photographing of the contents during a routine office move. This is not obvious to firms whose estate-planning practice predates digital assets; spell it out in the engagement letter. They also need a documented release procedure on death certificate (some firms require specific clauses in the engagement to define the verification standard) and a succession plan if the partner you engaged retires before you do. The clause to ask for is something like "if [named partner] is no longer at the firm, the next senior partner in the estate-planning practice assumes the holding role under the same terms" — the specific language varies by jurisdiction, and the lawyer's own drafting will be appropriate to local norms.

Probe the firm's crypto literacy before engaging. Ask how they store cryptographic material today, whether they have written procedures for digital-asset release, and how many existing clients have similar arrangements. A firm with no answers to any of these questions is not a candidate; a firm with mature answers is rarer in practice than the marketing suggests. This is the search effort you save by going with a collaborative-custody service instead in Pattern B — the service has done the institutional homework on this question, where individual law firms vary widely.

Multiple copies of the right things

The descriptor or Safe address is public information. Storing it in multiple places (lawyer's envelope, safe-deposit box, trusted family member's keeping, encrypted cloud backup) is structurally fine — losing it is the inheritance failure mode you most want to prevent, and the data being public means redundancy is cheap. The handover instructions are confidential rather than secret — they reveal the structure of your setup but not the keys themselves, so storing the instruction document in fewer but well-chosen locations (lawyer plus one or two trusted parties) is a reasonable middle ground. Private keys and seeds belong with their keyholders only — never in the handover document, never in any redundant copy of it.

Annual review cadence

Treat the inheritance plan as a fire drill that runs annually. Once a year, ideally on a fixed calendar reminder, confirm a small checklist. The law firm or collaborative-custody service still exists in its current legal form (acquired? dissolved? merged?). The named partner or contact is still there. The heir's signer device still powers on and runs current firmware. For Bitcoin multisigs, the technical step worth doing is re-exporting the extended public keys (xpubs) from each of your three signers and confirming they match the xpubs saved in the descriptor exactly. This works as an integrity check because of how Bitcoin derives keys: under BIP 32, the same seed at the same derivation path always produces the same xpub on any conforming wallet, and BIP 48 specifies the standard derivation path for multisig wallets (m/48'/0'/0'/2' for P2WSH SegWit; m/48'/0'/0'/3' for Taproot). If a re-export today returns a different xpub than the saved descriptor, that drift is a warning: your signer's interpretation of the path has changed somehow, and the heir's reconstruction may not work the same way next time. For Safe multisigs, re-load the contract address into Safe{Wallet} and confirm the owner set and threshold display correctly. The named beneficiaries are still the right people for your current life circumstances. The handover document has been updated to reflect any changes from the previous year. Refresh the "last verified working" date stamp. The whole drill takes an evening if nothing has changed and is a multi-week project if something has — the value is the same either way, because you have either confirmed the plan or surfaced the gap before the gap turns into a crisis.

Heir-Operability Pitfalls

The most common failure mode of a well-built multisig inheritance plan is not technical or legal — it is that the heir cannot operate the setup at the moment they need to. The technical configuration is correct, the documentation is in place, the keys are distributed appropriately, and yet the handover stalls because the heir is touching Sparrow for the first time during a grief scenario and the software's UX has changed since the last documentation update. The pitfalls below cluster around this single root cause; the dry-run rule at the end of the section is the discipline that mitigates all of them simultaneously.

The "just import the seed phrase" pitfall

The most common misuse in practice: telling the heir, in informal conversation or in the handover document, "just import the seed phrase and the funds will appear." For a multisig wallet, the seed alone is not enough — you also need the descriptor (Bitcoin) or the Safe contract address (EVM) plus the other co-signers' extended public keys. Importing a multisig seed phrase into a single-sig wallet (which is what most coordinator software will do by default if you import a seed without a descriptor) produces a wallet that is structurally correct, addresses that are derivable, and a balance of zero — because the multisig funds live at a different address derived from the combined script, not at any single-sig address derivable from a single seed.

This is the Bitcoin multisig footgun in concentrated form, and it traps non-technical heirs first. The mitigation is structural: the handover document names the descriptor explicitly, says it is required, and tells the heir what to do with it ("load this file into Sparrow's File > Open Wallet"). And the dry-run rule is the operational test: can the heir, without you in the room, load the descriptor into the named coordinator and see the multisig wallet read-only? If they cannot do this today, the plan is broken.

The coordinator-software UX pitfall

Sparrow, Nunchuk, and Safe{Wallet} each have learning curves that are reasonable for a technically-inclined adult with a quiet afternoon and a working internet connection. The same software is hostile to a non-technical adult in grief, with limited time, unfamiliar with the hardware-signer concepts, and without anyone to ask. Specific friction points: wallet import flows that require you to select the correct wallet type (multisig versus single-sig), connect signer devices in a specific order, and handle USB or QR connectivity that may not work first time. Recovery flows that require the heir to understand the difference between a watch-only wallet and a spending wallet, and to know they need to connect signers in sequence. Transaction-construction UIs that assume familiarity with fee estimation, address verification, and the difference between a draft and a broadcast transaction. None of this is intuitive on first encounter.

The device pitfall

Hardware signers age. Firmware updates change interfaces between the day you set the multisig up and the day the heir needs to use it; some signers use coin-cell batteries with finite lives; some use USB-C connectors that may be deprecated in twenty years; some use proprietary cable types that may be harder to source than they are today. The mitigation is to plan for device replacement. Document the model name and version. If the device has been discontinued — a real possibility on a multi-decade horizon — document an alternative signer that is descriptor-compatible. The reason cross-vendor replacement works at all is BIP 32 determinism: under BIP 32, the seed phrase plus the derivation path is the full input to public-key generation, and any conforming hardware signer or software wallet that implements BIP 32 produces the same xpub from the same seed at the same path. A Keystone 3 Pro and a Coldcard Mk5 and a Trezor Safe 7, given the same seed and the same BIP 48 multisig path, all derive the same xpub. The heir does not need the original device brand — they need a device that implements the same BIP 32 derivation and supports the BIP 48 multisig path, and the descriptor in the handover document tells the coordinator exactly which path to use. The descriptor is the wallet; the device is replaceable. That is the structural property that makes the inheritance plan survive across the lifespan of any one hardware product.

The coordinator-software death pitfall

The application you used to set the multisig up in 2026 may not exist in 2046. Sparrow's developer may have moved on; Nunchuk's company may have been acquired and the product wound down; Safe{Wallet} may have rebranded or restructured. The mitigation is to bias towards coordinators with strong open-source provenance and reproducible builds — Sparrow Wallet, Nunchuk, and Electrum all have source code in public repositories that someone could in principle fork and rebuild even if the original maintainer disappeared. Avoid coordinators with proprietary on-chain dependencies or closed-source release pipelines, because those have no continuity guarantee independent of the company shipping them. The descriptor itself is a standardised text format (BIP 380 onward), which means a competently-built future coordinator can load it regardless of which specific software produced it in 2026.

Multisig-versus-single-sig framing for the heir

Worth saying explicitly because the conceptual confusion is real. A seed phrase in a single-sig setup is total authority — anyone with the seed can sweep the wallet. A single key in a 2-of-3 multisig has no authority alone; the threshold blocks unilateral action by design. The heir holding one of three keys cannot move funds on their own, and that is the structural property you have given them — protection against compromise, protection against being pressured to spend, protection against making a mistake during their first encounter with the coordinator software. Pair this framing with the explicit caveat that Tangem's multi-card system is key-redundancy backup rather than M-of-N multisig (a separate architecture entirely) — if the heir confuses the two on a future inheritance setup of their own, they will produce something that looks like a multisig and behaves like a single-sig with backup, which is structurally worse than either pure pattern done correctly.

The dry-run rule

The single discipline that turns every pitfall above from a hypothetical into a managed risk: before the setup is considered complete, the heir must independently — without you in the room, ideally a year before the day they would actually need to do it — load the wallet read-only from the descriptor or Safe contract address, observe a small testnet transaction or a tiny mainnet transaction you have constructed for the rehearsal, and demonstrate they could move funds with their available keys plus the recovery release. If the heir cannot do this today, in your kitchen, with you in the next room available for one phone call if absolutely needed, they cannot do it after a custodial event. The rehearsal does not have to be elaborate — an hour of focused work, on the heir's own laptop, ending in a transaction they signed and broadcast. The fact of having done it once changes the heir's confidence and your confidence in the plan; the absence of it is the gap that swallows otherwise-careful setups.

Conclusion

Three pattern families cover practically every workable multisig inheritance setup: Pattern A self-plus-lawyer-plus-heir (the simplest and structurally cheapest, dependent on a law firm's institutional continuity), Pattern B self-plus-heir-plus-collaborative-custody (more expensive ongoing, more robust to family-circumstance changes, dependent on a third-party service's longevity), Pattern C distributed family 3-of-5 (most operationally complex, most robust across family complexity and multi-generational horizons). Match the pattern to your holdings size, family complexity, and heir technical fluency. None of the three is universally correct, and switching between them as your life changes is a routine multisig rotation operation rather than a structural redo.

The single discipline that determines whether any of the patterns actually works is the dry-run rule. An untested handover is no handover — the multisig is operationally inert if the heir cannot load the descriptor, run the coordinator, and combine their key with the released recovery key under conditions that approximate the day they will eventually need to do it. The technical configuration matters; the documentation matters; the legal framework matters; the rehearsal matters more than any of them, because it is what surfaces the gaps in everything else.

Inheritance is the test multisig was built for. Single-sig "trust your spouse" plans and "seed in a will" arrangements both collapse at the handover for different reasons — total authority once revealed, no testability while alive, brittleness to relationship and jurisdictional changes. M-of-N gives you the structural property that single-sig structurally cannot: no single party (including you while alive) can move funds unilaterally, yet the documented release process reconstitutes authority on a custodial event. The mechanics for instantiating that property differ between BTC and EVM — see the hub for M-of-N mechanics, the Bitcoin multisig setup guide, and the Ethereum Safe multisig guide for the operational walkthroughs. For the service-level comparison of Safe versus Casa versus Unchained, the compare page covers the commercial axes.

Sources

- Casa — service overview: primary citation for Casa's multi-asset collaborative-custody architecture and the 2-of-3 inheritance model in which the client holds two keys and Casa holds one recovery key.

- The Block — Casa expands self-custody inheritance globally: independent coverage of Casa's 2026 global rollout adding Bitcoin, Ethereum, USDT, and USDC support to the inheritance product.

- Unchained — about page: primary citation for Unchained's Bitcoin-only collaborative-custody model, the 2-of-3 vault architecture with an independent third-party agent, and adjacent services including Bitcoin-backed loans and Bitcoin retirement accounts.

- Sparrow Wallet — Bitcoin desktop coordinator: open-source Bitcoin coordinator software referenced in the coordinator-longevity discussion and the Pattern A worked-example walkthrough.

- Nunchuk — Bitcoin multisig coordinator: open-source Bitcoin multisig software referenced as an alternative coordinator with mobile and desktop support.

- Safe — official protocol overview: primary citation for Safe (formerly Gnosis Safe, rebranded 2022), the EVM smart-contract multisig referenced as the coordinator software for any EVM Pattern A or Pattern B setup.

- Keystone — Keystone 3 Pro: hardware-signer manufacturer reference for the air-gapped, clear-signing device positioned as a long-term inheritance signer in any of the three patterns above.

Frequently Asked Questions

- Can I leave a seed phrase to my heir in my will?

- Technically yes, structurally no. A seed phrase in a will is visible to anyone reading the will — at minimum the probate lawyer, often a court clerk, sometimes copies in jurisdictions that require document filing. The will then sits in a drawer or registry for months between signing and the day it is read, with no procedure for testing that the seed still works during that window. A single seed is total authority once it leaves your control; you cannot revoke it, you cannot rotate it without rewriting the will, and you cannot verify the heir can actually use it before the day they need to. A multisig solves all three problems: each key holder has partial authority that does nothing alone, the configuration is testable while you are alive, and rotation is a routine operation. Use multisig key distribution rather than a will-embedded seed for any holding you would not be comfortable losing entirely.

- What is the simplest multisig inheritance setup?

- A 2-of-3 with you holding two keys at different physical locations and a lawyer or law firm holding the third. During your life you sign with your two keys and the lawyer's key never moves. On a custodial event your executor combines the second of your keys (released via the estate) with the lawyer's key (released against a death certificate per the engagement letter), and the heir gains access. Variations swap the lawyer for a collaborative-custody service or a designated trustee — the architectural property is the same. The single non-negotiable practice across every variation is testing the handover while you are alive, so the heir is not learning the coordinator software for the first time during the worst week of their life.

- Do Casa or Unchained replace a lawyer in my inheritance plan?

- They replace the lawyer-as-key-holder role with a structured paid service that has documented verification and a release process. They do not replace the legal will, the executor, or jurisdiction-specific probate procedure — those still apply to everything you own that is not crypto, and to the legal recognition of the heir's claim. Casa and Unchained are paid third-party collaborative-custody services where you trust the recovery key to an external party; the trade is service fees plus third-party dependency against personal-relationship dependency on a law firm. Full service-level comparison — pricing tiers, asset coverage, jurisdictional notes — lives in the Safe vs Casa vs Unchained comparison.

- What happens if I lose one of my own keys during my life?

- In a 2-of-3 you still spend with the remaining two keys, and the wallet remains operational. You then rotate to a new configuration: deploy a new multisig with a replacement signer device, transfer the funds, and update the handover documentation so the lawyer and heir have the current descriptor or contract address rather than the obsolete one. This is the reason annual review cadence matters — a setup that was correct two years ago may not match the current key set. The replacement workflow is routine and is structurally why multisig is more resilient than single-sig: a lost seed in single-sig is an existential event; a lost device in 2-of-3 is a Tuesday-afternoon rotation.

- Can my heir use a multisig wallet if they have never touched crypto?

- Not safely without preparation. A non-technical heir loading Sparrow, Nunchuk, or Safe{Wallet} for the first time in a grief scenario is in the worst possible state to debug a coordinator-software learning curve. The dry-run rule applies: before the setup is considered complete, the heir must demonstrate — without you in the room — that they can load the wallet read-only from the descriptor or contract address, observe transactions, and rehearse what they would do with the recovery key once it is released. Collaborative-custody services (Pattern B) reduce but do not eliminate the requirement; the service does verification on their side, but the heir still needs to operate their own signer device to combine with the released recovery key.

- What is the difference between handing over a seed phrase and handing over keys in a multisig?

- A seed phrase is total authority once it leaves your control. Anyone in possession of the seed can sweep the wallet immediately and irreversibly; there is no threshold, no verification, no recall. A single key in a 2-of-3 multisig has no spending authority on its own — the threshold blocks unilateral action. Combining keys at handover only produces authority alongside the documented release process for the recovery key. The structural difference is that multisig inheritance separates the moments of trust: you trust the law firm or service to hold the recovery key without using it during your life, and you trust the executor to combine the released keys with the heir's key after a custodial event. Each layer is verifiable on its own; a single seed phrase concentrates all of that trust into one piece of paper.

- How often should I review my inheritance setup?

- Annually. Treat it as a fire drill rather than an audit. The annual review confirms that the law firm or collaborative-custody service still exists in its current legal form, the heir's signer device still powers on and runs current firmware, the descriptor or Safe contract address still loads cleanly in the named coordinator software, and the named beneficiaries are still the right people (life happens — marriages, divorces, estrangements, new children). The handover document gets a fresh "last verified working" date stamp; the law firm gets a courtesy email confirming the contact partner is still there. A calendar reminder is enough — the entire drill takes an evening if nothing has changed, and is a multi-week project if something has.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.