Crypto Lending Interest Rates

Understand how lending interest rates work in 2025. Learn about rate drivers, platform comparisons, risk factors, and strategies to maximise your lending returns safely.

Introduction

Crypto lending rates are driven by one thing: borrowing demand. When traders need to borrow USDC to short or leverage, lending rates rise. When demand drops, so do rates. In March 2025, Aave's USDC supply rate hit 12% during a BTC rally as leverage demand spiked. Two weeks later, it settled back to 4%. Understanding this mechanism -- and the specific factors that shift borrowing demand -- is the difference between earning 3% and 10% on the same asset.

Current rate ranges across platforms vary significantly by asset type. Stablecoins (USDC, USDT, DAI) yield 2-10% depending on platform and lock-up terms. BTC yields 1-6%, lower because fewer borrowers need BTC for trading strategies. ETH yields 2-8%, partly because native staking at roughly 3.5% APY competes directly with lending for depositor capital. Major altcoins (SOL, ADA) yield 3-12% but carry higher volatility risk that can wipe out months of interest in a single drawdown.

A structural shift worth understanding: tokenised US Treasury products from BlackRock (BUIDL), Ondo (USDY), and others now offer 4.5-5% yields backed by government securities. This has set an effective floor for crypto lending rates — any platform offering less than 5% on stablecoins must justify the additional smart contract or counterparty risk you take on compared to this near-risk-free benchmark. These numbers shift weekly on DeFi protocols and quarterly on CeFi platforms.

The critical distinction is between CeFi and DeFi risk profiles. CeFi platforms (Nexo, Binance Earn, Coinbase) offer fixed or semi-fixed rates with counterparty risk -- if the platform goes bankrupt (Celsius, BlockFi), you lose your deposit. DeFi protocols (Aave, Compound, Morpho) offer variable rates with no counterparty risk but smart contract risk instead. Neither approach is inherently safer; the risks are simply different.

For UK-based lenders, there are additional considerations worth noting upfront. HMRC treats all crypto lending interest as miscellaneous income, taxed at your marginal rate -- 20%, 40%, or 45% depending on your income band. Your annual capital gains allowance of £3,000 does not apply to lending income. Additionally, the FCA's restrictions on crypto promotions mean that several high-yield platforms cannot actively market to UK residents, though you can still access them directly. This guide breaks down specific rates by platform, explains what drives rate changes, and provides concrete strategies for each risk tolerance level.

Quick Overview

Crypto lending rates in 2025 are mainly variable, responding to market demand, platform liquidity, and regulatory changes. Stablecoins typically offer APRs of 2-10%. Meanwhile, volatile assets can range from 3% to 15% depending on market conditions and platform incentives.

Key factors affecting rates

- Borrowing demand and use rates

- Platform liquidity and reserve levels

- Regulatory environment and compliance costs

- Market volatility and risk premiums

Interest Rate Landscape

Market Overview

The lending market in 2025 has matured greatly. It has clearer regulatory frameworks and more advanced risk management. Interest rates have generally stabilised compared to the volatile periods of 2022-2023, but still offer attractive yields compared to traditional finance.

Total value locked (TVL) in lending protocols has reached new highs. It has over $50 billion across major platforms. This increased liquidity has led to more competitive rates and better user terms. Institutional adoption has also grown. It has pension funds and corporate treasuries allocating portions of their portfolios to lending strategies.

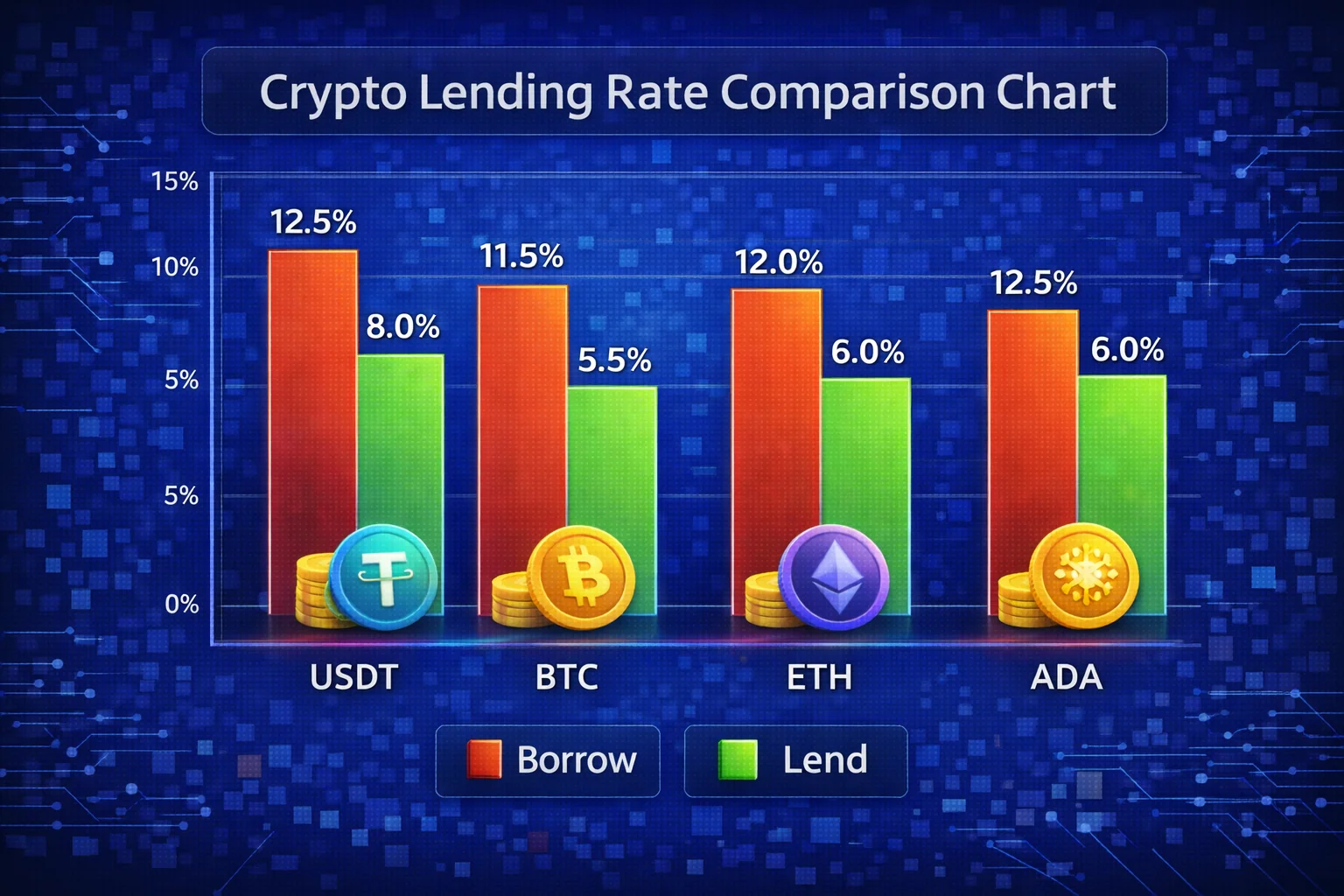

Current Rate Ranges by Asset Type

| Asset Category | Typical APR Range | Platform Type | Risk Level |

|---|---|---|---|

| Stablecoins (USDC, USDT, DAI) | 2-10% | CeFi & DeFi | Low-Medium |

| Bitcoin (BTC) | 1-6% | mainly CeFi | Medium |

| Ethereum (ETH) | 2-8% | CeFi & DeFi | Medium |

| Major Altcoins (SOL, ADA, DOT) | 3-12% | Mixed | Medium-High |

| Smaller Altcoins | 5-25% | mainly DeFi | High |

Platform-Specific Rate Analysis

Top CeFi Platform Rates (September 2025)

| Platform | USDC APR | BTC APR | ETH APR | Special Features |

|---|---|---|---|---|

| Nexo | 8-12% | 4-6% | 5-7% | Loyalty tiers, insurance |

| Binance Earn | 3-8% | 1-3% | 2-5% | Flexible/locked terms |

| Coinbase | 2-5% | 1-2% | 2-4% | FDIC insurance (USD) |

| Kraken | 3-6% | 1-4% | 2-6% | Regulated, transparent |

Leading DeFi Protocol Rates

| Protocol | USDC APR | ETH APR | Token Rewards | use Rate |

|---|---|---|---|---|

| Aave V3 | 4-8% | 2-5% | None | 75-85% |

| Compound V3 | 3-7% | 1-4% | COMP tokens | 70-80% |

| Morpho | 5-9% | 3-6% | MORPHO tokens | 80-90% |

| Euler | 4-8% | 2-5% | EUL tokens | 65-75% |

Regional Rate Variations

Interest rates can vary greatly by geographic region because of regulatory differences, local demand, and platform availability:

- United States: Generally lower rates because of regulatory compliance costs, but higher security

- European Union: Moderate rates with strong consumer protections under MiCA regulation

- Asia-Pacific: Higher rates in some jurisdictions but varying regulatory clarity

- Emerging Markets: Often highest rates but increased regulatory and operational risks

Seasonal Rate Patterns

Crypto lending rates exhibit predictable seasonal patterns:

- Q1 (Jan-Mar): Typically higher rates because of tax-loss harvesting and new year allocations

- Q2 (Apr-Jun): Moderate rates with increased institutional activity

- Q3 (Jul-Sep): Often lower rates because of summer trading lull

- Q4 (Oct-Dec): Variable rates depending on market sentiment and year-end positioning

What Drives Crypto Lending Rates

main Rate Drivers

1. Supply and Demand Dynamics

The basic driver of lending rates is the balance between lenders (supply) and borrowers (demand). High borrowing demand relative to available liquidity tends to push rates up. Meanwhile, excess liquidity tends to drive rates down.

- use rates: Higher use (borrowed/total supplied) increases rates

- Seasonal patterns: Rates often spike during bull markets and DeFi seasons

- use demand: Increased trading activity drives borrowing for margin positions

2. Platform-Specific Factors

- Reserve requirements: Platforms maintain reserves affecting available liquidity

- Risk management: Conservative platforms offer lower but more stable rates

- Operational costs: Compliance, insurance, and operational expenses impact net rates

- Competitive positioning: Platforms adjust rates to attract or retain users

3. Market Conditions

- Volatility: Higher volatility increases risk premiums and borrowing costs

- Liquidation risk: Assets with higher liquidation risk command higher rates

- Correlation: Highly correlated assets may have similar rate movements

- Market sentiment: Bull markets increase use demand and rates

4. Regulatory Environment

- Compliance costs: Regulatory requirements increase operational expenses

- Geographic restrictions: Limited access can affect supply/demand balance

- Insurance requirements: Mandatory insurance reduces net yields to lenders

- Capital requirements: Banking-style regulations may limit lending capacity

CeFi vs DeFi Rate Dynamics

centralised Finance (CeFi) Platforms

CeFi platforms like Nexo, Binance, and Coinbase offer managed lending experiences with several characteristics:

CeFi Rate Characteristics:

- Promotional rates: Often feature limited-time high APR offers

- Tiered systems: Higher balances may earn better rates

- Rate caps: Maximum amounts eligible for advertised rates

- Flexible terms: Usually offer both flexible and fixed-term options

- Insurance coverage: Some platforms provide deposit insurance

Pros and Cons:

| Advantages | Disadvantages |

|---|---|

| User-friendly interfaces | Counterparty risk |

| Customer support | Lower transparency |

| Regulatory compliance | Potential rate changes |

| Insurance options | KYC requirements |

decentralised Finance (DeFi) Protocols

DeFi lending protocols, such as Aave and Compound. Because well as newer platforms, offer algorithmic rate setting with full transparency.

DeFi Rate Characteristics:

- Algorithmic rates: Rates adjust automatically based on use curves

- Real-time updates: Rates can change with every block

- Token incentives: more rewards through governance tokens

- Composability: Ability to use receipt tokens in other protocols

- No minimums: Usually no minimum deposit requirements

Rate Calculation Examples

DeFi protocols typically use use-based models. Here's how rates are calculated:

Aave Interest Rate Model

Aave uses a kinked interest rate model with the following formula:

- Base rate: 0% (minimum rate when use is 0%)

- Slope 1: 4% increase up to 80% use

- Slope 2: 75% increase from 80% to 100% use

- Optimal use: 80% for most stablecoins

Example calculation for USDC at 85% use:

- Base rate: 0%

- Rate from 0-80%: 80% × 4% = 3.2%

- Rate from 80-85%: 5% × 75% = 3.75%

- Total supply APR: 0% + 3.2% + 3.75% = 6.95%

Compound Interest Rate Model

Compound uses a different approach with continuous rate adjustments:

- Base rate per year: 2%

- Multiplier per year: 5%

- Jump multiplier per year: 109%

- Kink: 80%

Formula:

- If use ≤ kink: borrowRate = baseRate + (use × multiplier)

- If use > kink: borrowRate = baseRate + (kink × multiplier) + ((use. kink) × jumpMultiplier)

- supplyRate = borrowRate × use × (1. reserveFactor)

Token Reward Calculations

Many protocols offer more rewards in governance tokens:

- Emission rate: Tokens distributed per block/second

- Pool allocation: Percentage of emissions for each asset

- User share: Your deposit / total pool deposits

- Token price: Current market value of reward tokens

Example COMP reward calculation:

- Daily COMP emissions to USDC pool: 100 COMP

- Your USDC deposit: $10,000

- Total USDC pool: $100,000,000

- Your share: 0.01%

- Daily COMP earned: 100 × 0.0001 = 0.01 COMP

- If COMP = $50: Daily reward = $0.50

- Annual reward APR: ($0.50 × 365) / $10,000 = 1.83%

Fixed vs Variable Rate Strategies

Variable Rate Lending

Most lending platforms use variable rates that adjust based on market conditions.

Advantages:

- Capture rate increases during high-demand periods

- No lockup periods. maintain liquidity

- Benefit from platform incentive programs

- Easier to rebalance across platforms

Disadvantages:

- Rate uncertainty and potential decreases

- Need for active monitoring and management

- Exposure to platform policy changes

- Potential for sudden rate drops

Fixed Rate Lending

Some platforms offer fixed-rate products. But these are less common in the crypto space.

Advantages:

- Predictable returns for planning purposes

- Protection against rate decreases

- Reduced need for active management

- Better for conservative strategies

Disadvantages:

- Miss out on rate increases

- Usually require lockup periods

- Limited availability and selection

- Often lower rates than variable peaks

Hybrid Strategies

Many experienced lenders use a combination approach:

- Core allocation: 60-70% in stable, variable rate platforms

- Opportunistic allocation: 20-30% chasing higher rates

- Fixed allocation: 10-20% in fixed rates for stability

Risk Factors Affecting Rates

Platform-Specific Risks

- Counterparty risk: Platform insolvency or mismanagement

- Regulatory risk: Changes in legal status or compliance requirements

- Operational risk: Technical failures or security breaches

- Liquidity risk: Inability to withdraw funds when needed

Market Risks

- Interest rate risk: Rates may decrease after commitment

- Currency risk: Exposure to volatile crypto asset prices

- Correlation risk: many positions affected by same events

- Systemic risk: Broader crypto market or DeFi protocol failures

Smart Contract Risks (DeFi)

- Code vulnerabilities: Bugs leading to fund loss

- Oracle failures: Price feed manipulation or failures

- Governance attacks: Malicious protocol changes

- Composability risks: Failures in connected protocols

Smart contract risk is concrete, not theoretical. Euler Finance — a well-audited lending protocol — lost $197 million in March 2023 through a flash loan attack exploiting a single function interaction between donation and liquidation logic. The attacker returned the funds after negotiation, but lenders were locked out for weeks during that uncertainty. Cream Finance suffered three separate exploits totalling over $130 million across 2021–2022. Even protocols with multiple audits carry residual risk; the question is whether the additional yield justifies the exposure. For stablecoin positions above £10,000, Nexus Mutual or similar on-chain coverage (typically 2–3% annually) can bring that risk to a manageable level, though coverage capacity per protocol is limited and worth checking before depositing.

Counterparty Risk: The CeFi Lesson

The Celsius collapse in July 2022 illustrates counterparty risk most clearly. At its peak, Celsius held $12 billion in customer deposits and marketed 18% APY on stablecoins — rates that required taking on significant leverage and credit risk internally to generate. When crypto prices fell and borrowers defaulted, Celsius froze withdrawals with no warning. Lenders who expected daily access found their funds locked in a bankruptcy proceeding. BlockFi followed in November 2022 after the FTX collapse, leaving approximately $1 billion in retail deposits entangled in proceedings that took years to resolve partially. Both platforms had been offering rates 3–6 percentage points above what regulated competitors like Nexo and Coinbase provided — a premium that, in retrospect, reflected the additional risk rather than superior operations. When a CeFi platform's advertised rate is materially higher than its regulated peers for extended periods, that gap deserves scrutiny before depositing.

Monitoring and improvement Strategies

key Monitoring Practices

Regular Rate Checks

- Weekly reviews: Check rates across your active platforms

- Rate alerts: Set up notifications for large changes

- use tracking: Monitor DeFi protocol use rates

- Incentive updates: Track changes in token reward programs

Performance Metrics

- Net APR: Account for fees, taxes, and token reward volatility

- Risk-adjusted returns: Consider platform and asset risks

- Opportunity cost: Compare with staking and other alternatives

- Liquidity premium: Value the ability to withdraw quickly

Advanced Monitoring Tools

Automated Tracking Solutions

- DeFiSaver: Automated position management and rebalancing

- Instadapp: DeFi portfolio improvement and automation

- Yearn Finance: Automated yield farming strategies

- Harvest Finance: Yield improvement with auto-compounding

Rate Comparison Platforms

- DeFi Rate: Real-time comparison of lending rates across protocols

- Loanscan: complete lending rate aggregator

- DeFi Prime: Curated list of DeFi lending platforms

- Staking Rewards: Comparison of staking vs lending yields

Analytics and Research Tools

- Dune Analytics: Custom dashboards for protocol analysis

- DefiLlama: TVL tracking and protocol comparisons

- Token Terminal: Financial metrics for DeFi protocols

- Messari: basic analysis and protocol research

improvement Strategies

Platform Diversification Framework

| Allocation | Platform Type | Risk Level | Purpose |

|---|---|---|---|

| 40-50% | Tier 1 CeFi (Nexo, Binance) | Low-Medium | Stable base yield |

| 30-40% | Blue-chip DeFi (Aave, Compound) | Medium | Higher yields with transparency |

| 10-20% | Emerging protocols | High | Capture new opportunities |

| 5-10% | Liquid reserves | Low | Emergency access |

Dynamic Rebalancing Strategies

Threshold-Based Rebalancing

- Rate differential threshold: Move funds when rate difference exceeds 1-2%

- Minimum position size: Only rebalance amounts above $1,000 to justify gas costs

- Cooling period: Wait 7-14 days between moves to avoid overtrading

- Platform health check: Verify platform stability before moving funds

Calendar-Based Rebalancing

- Monthly review: complete portfolio assessment

- Quarterly rebalancing: Major allocation adjustments

- Annual strategy review: Update risk tolerance and goals

- Tax-loss harvesting: Year-end improvement for tax efficiency

Risk-Adjusted improvement

Sharpe Ratio Calculation

Calculate risk-adjusted returns using the Sharpe ratio:

- Formula: (Portfolio Return. Risk-Free Rate) / Portfolio Volatility

- Risk-free rate: Use US Treasury or stablecoin base rate

- Portfolio volatility: Standard deviation of monthly returns

- Target Sharpe ratio: Aim for >1.0 for good risk-adjusted performance

Maximum Drawdown Management

- Set limits: Maximum 20% allocation to any single platform

- Correlation analysis: Avoid overexposure to correlated risks

- Stress testing: Model performance during market downturns

- Recovery planning: Strategies for rebuilding after losses

Tools and Resources

Portfolio Management Tools

- Zapper: Portfolio tracking across many protocols

- DeBank: complete DeFi portfolio management

- Zerion: Mobile-first DeFi portfolio tracker

- Rotki: Open-source portfolio tracking and tax reporting

API Integration

- Platform APIs: Direct integration for automated monitoring

- Price feeds: CoinGecko, CoinMarketCap for token valuations

- DeFi APIs: The Graph Protocol for on-chain data

- Notification services: Discord, Telegram bots for alerts

Spreadsheet Templates

Create complete tracking spreadsheets with:

- Platform allocation and current rates

- Historical performance tracking

- Risk metrics and correlation analysis

- Tax reporting and cost basis tracking

- Rebalancing triggers and decision logs

Rate Outlook and Trends

Regulatory Impact

Increasing regulatory clarity in major jurisdictions is expected to:

- Stabilise rates as compliance costs become predictable

- Reduce extreme rate volatility through better risk management

- Increase institutional participation, adding liquidity

- Create clearer distinctions between compliant and non-compliant platforms

Technology Developments

- Layer 2 scaling: Reduced transaction costs enabling smaller position management

- Cross-chain protocols: Better rate arbitrage opportunities

- Automated strategies: Yield farming and rate improvement tools

- Insurance products: Better risk management and potentially lower rates

Market Maturation

- More advanced risk pricing models

- Increased competition leading to better user terms

- Greater integration with traditional finance

- More stable, sustainable rate structures

Tax and Regulatory Considerations

Tax Implications of Crypto Lending

Income Tax Treatment

In most jurisdictions, crypto lending interest is treated as ordinary income:

- Accrual basis: Income recognised when earned, not when withdrawn

- Fair market value: Interest valued at time of receipt

- Token rewards: more income at token's FMV when received

- Compounding: Reinvested interest creates more taxable events

Record Keeping Requirements

- Transaction logs: All deposits, withdrawals, and interest payments

- Platform statements: Monthly or annual statements from each platform

- Token valuations: USD value of all token rewards at receipt time

- Cost basis tracking: Original purchase price and dates for all assets

Tax improvement Strategies

- Tax-loss harvesting: realise losses to offset lending income

- Timing withdrawals: Manage income recognition across tax years

- Retirement accounts: Use tax-advantaged accounts where possible

- Geographic arbitrage: Consider tax-friendly jurisdictions

UK-Specific Tax Mechanics

For UK residents, HMRC treats crypto lending interest as miscellaneous income, reported under the "Other income" section of Self Assessment (SA100, box 17). The income is recognised at the point each interest payment is received — not when you withdraw from the platform. If a protocol compounds interest automatically (as Aave does with aTokens appreciating in value), each block where your token balance increases is technically a taxable receipt, though in practice HMRC expects you to report the annualised total rather than thousands of micro-events.

The practical record-keeping approach: export your transaction history from each platform at tax year end (5 April) in CSV format. Nexo, Binance, and Coinbase all offer these exports natively. For DeFi protocols, Etherscan's transaction history or a tool like Koinly or CoinTracker can reconstruct your interest accruals from on-chain data, with Koinly pricing each receipt at its sterling value at the time of the transaction. Keep these exports for at least six years, as HMRC can open enquiries that far back for offshore income.

The Personal Savings Allowance does not apply to crypto lending income — it only covers interest from banks and building societies. However, if your total lending income from all crypto sources falls below £1,000 in a tax year, HMRC's trading allowance (or the miscellaneous income allowance) may eliminate the tax liability entirely. Above that threshold, income is taxed at 20% for basic-rate taxpayers and 40% for higher-rate taxpayers, which means a gross 7% APY becomes approximately 4.2% net after higher-rate tax — worth factoring into every platform comparison.

Regulatory Compliance

Know Your Customer (KYC) Requirements

Most regulated platforms require identity verification:

- Identity documents: Government-issued ID and proof of address

- Source of funds: Documentation of crypto acquisition

- Ongoing monitoring: Periodic re-verification and updates

- Reporting thresholds: Automatic reporting for large transactions

Anti-Money Laundering (AML) Compliance

- Transaction monitoring: Platforms monitor for suspicious activity

- Reporting requirements: Suspicious activity reports to authorities

- Sanctions screening: Compliance with international sanctions lists

- Enhanced due diligence: more checks for high-risk customers

Jurisdiction-Specific Regulations

United States

- SEC oversight: Some lending products may be considered securities

- State regulations: Varying state-level licensing requirements

- CFTC jurisdiction: Derivatives and futures-related lending

- Banking regulations: FDIC insurance for USD deposits on some platforms

European Union

- MiCA regulation: complete crypto asset regulation framework

- GDPR compliance: Data protection requirements for user information

- National implementations: Country-specific licensing and oversight

- Passporting rights: EU-wide service provision for licensed entities

Best Practices for Rate improvement

Getting Started Framework

Phase 1: Foundation (Months 1-2)

- Education: Complete crypto lending courses and read platform documentation

- Small start: Begin with $100-500 on 1-2 reputable platforms

- Risk assessment: Understand and document your risk tolerance

- Setup tracking: Create spreadsheets or use portfolio tools

Phase 2: Expansion (Months 3-6)

- Platform diversification: Add 2-3 more platforms

- Asset diversification: Experiment with different cryptocurrencies

- Strategy testing: Try both CeFi and DeFi options

- Performance analysis: Compare actual vs expected returns

Phase 3: improvement (Months 6+)

- Advanced strategies: use yield farming and token rewards

- Automated tools: Use APIs and bots for monitoring

- Tax improvement: use tax-efficient strategies

- Continuous improvement: Regular strategy reviews and updates

Advanced Strategies

Yield Farming Integration

- Liquidity provision: Combine lending with DEX liquidity provision

- Leveraged farming: Borrow to increase farming positions (high risk)

- Cross-protocol strategies: Use lending receipts in other protocols

- Impermanent loss hedging: Balance farming with stable lending

Rate Arbitrage Techniques

- Cross-platform arbitrage: Exploit rate differences between platforms

- Temporal arbitrage: Time entries and exits based on rate cycles

- Geographic arbitrage: Access region-specific rates and platforms

- Asset arbitrage: Convert between assets to capture rate premiums

Token Farming improvement

- Emission schedules: Time entries to maximise token rewards

- Vesting strategies: improve token claim timing for tax efficiency

- Governance participation: Use tokens for voting and more rewards

- Token diversification: Manage exposure to governance token volatility

Risk Management Framework

Position Sizing Rules

- Maximum platform exposure: No more than 20% on any single platform

- Asset concentration limits: Maximum 40% in any single cryptocurrency

- Geographic diversification: Spread across many jurisdictions

- Liquidity requirements: Maintain 10-20% in highly liquid positions

Emergency Procedures

- Platform failure protocol: Steps to take if a platform becomes insolvent

- Market crash response: Predetermined actions during severe downturns

- Regulatory changes: Adaptation strategies for new regulations

- Personal emergencies: Quick liquidation procedures for urgent needs

Insurance and Protection

- Platform insurance: prioritise platforms with deposit insurance

- DeFi insurance: Consider protocols like Nexus Mutual for smart contract coverage

- Self-insurance: Maintain emergency funds in traditional accounts

- Legal protection: Understand legal recourse in different jurisdictions

Regulatory Impact on Interest Rates

The European Union's MiCA regulation affects cryptocurrency lending platforms operating in EU markets, requiring enhanced capital reserves and compliance procedures that may influence interest rate structures.

Platforms must maintain operational reserves equivalent to 2% of managed assets, potentially reducing yields by 0.2-0.5% annually to cover regulatory compliance costs and capital requirements.

United States regulatory developments, including potential stablecoin legislation and SEC guidance on cryptocurrency lending products, create uncertainty that affects platform risk premiums and interest rate offerings. Regulatory clarity could reduce risk premiums by 1-2% annually, while continued uncertainty may keep rates elevated as platforms price in compliance and legal risks throughout 2025.

Singapore's progressive regulatory framework enables competitive interest rates through operational efficiency and regulatory certainty, with licensed platforms offering rates 0.5-1% higher than jurisdictions with unclear regulatory environments.

The Monetary Authority of Singapore's clear guidelines reduce operational risks and enable more aggressive rate competition amongst licensed providers while maintaining complete consumer protection measures.

Practical Rate Monitoring

Where to Track Rates

DefiLlama's lending dashboard (defillama.com/protocols/Lending) remains the most reliable free tool for comparing DeFi lending rates across protocols. It aggregates real-time supply APY data from Aave, Compound, Spark, and dozens of smaller protocols, sorted by total value locked.

For CeFi platforms, you need to check each platform directly — Nexo, Binance Earn, and Crypto.com update their rate pages daily, though promotional tiers change without notice. Bookmark these pages and check them on a fixed schedule rather than reacting to social media rate announcements, which are often outdated by the time you see them.

When to Move Capital

The critical rule for rate-chasing: your rate differential must exceed three times your total transaction costs before moving capital between platforms. If switching from Compound to Aave costs you $15 in gas fees and withdrawal time, you need to earn at least $45 more over your intended holding period to justify the move.

For a $10,000 USDC position held for 90 days, a 1.5% APY improvement generates roughly $37 — barely enough to cover the switch. At $50,000, that same differential produces $187, making the move clearly worthwhile. Calculate your break-even period before every reallocation.

Monitoring Frequency by Position Size

How often should you check rates? It depends on your position size. If you are lending under $5,000, monthly reviews are sufficient — transaction costs eat into small positions too aggressively for frequent moves. For $5,000 to $50,000, fortnightly checks strike the right balance between optimisation and overthinking.

Above $50,000, weekly monitoring makes sense because even small rate differentials produce meaningful returns at scale. Positions above $200,000 justify setting up automated alerts through DefiLlama's notification system or a simple script that pings you when rates on your platform drop below a threshold you define.

Cross-Platform Rate Comparison

Current Rate Ranges by Platform

As of early 2026, stablecoin lending rates vary considerably across platforms. On the DeFi side, Aave V3 offers USDC supply rates between 3% and 5% APY depending on network utilisation, whilst Compound V3 sits slightly lower at 3% to 4%. These rates fluctuate in real time based on borrowing demand — during periods of high leverage activity, Aave rates can spike above 8% for hours or days before settling back. Spark Protocol, built on MakerDAO infrastructure, typically offers 4% to 6% on DAI deposits.

CeFi platforms offer more predictable but tiered rates. Nexo's base stablecoin rate starts at 4% to 8% APY, rising to 12% to 16% for Platinum-tier users who hold a significant proportion of their portfolio in NEXO tokens and lock funds for fixed terms.

Binance Earn provides 3% to 6% on flexible stablecoin products, with higher rates available through locked savings and Launchpool. Crypto.com's Earn programme ranges from 3% flexible to 8.5% for three-month CRO-staked locks, though these tiers have been adjusted multiple times since 2024.

Transaction Costs to Move Between Platforms

Before chasing higher rates, you must account for the full cost of moving. On Ethereum mainnet, a token approval plus transfer costs roughly $3 to $8 in gas during normal conditions, but depositing into a DeFi protocol adds another $5 to $15 for the contract interaction. Withdrawals from CeFi platforms often carry flat fees — Binance charges 1 USDC per withdrawal on Ethereum, whilst Nexo allows a limited number of free withdrawals per month depending on your loyalty tier.

If you are moving between DeFi protocols on the same chain, total round-trip costs typically run $15 to $40. On Layer 2 networks like Arbitrum or Base, the same operations cost under $1, making frequent rebalancing far more practical for smaller positions.

Rate Arbitrage in Practice

Worked Example: Moving $50K USDC from Compound to Aave

Suppose you have $50,000 USDC deposited in Compound V3 earning 3.5% APY, and you notice Aave V3 has been consistently offering 5.2% APY for the past week. The rate differential is 1.7 percentage points, translating to $850 per year in additional yield, or roughly $71 per month.

Your costs to execute the move include withdrawing from Compound (approximately $12 in gas), approving and depositing into Aave (approximately $18 in gas), and the opportunity cost of being unlent during the transition — perhaps two hours, which at 5.2% APY on $50,000 amounts to roughly $0.59. Total cost: around $31.

Your break-even point arrives in about 13 days. If you expect the rate differential to persist for at least two months, the move generates roughly $110 in net additional yield after costs. That is a straightforward decision.

However, if the differential is only 0.5% — producing $250 per year or $21 per month — your break-even stretches to 45 days, and the risk of rates converging before you recoup costs rises substantially. In practice, most experienced lenders only move capital when the annualised differential exceeds 1% on positions above $25,000, or 2% on positions below that threshold.

When Arbitrage Does Not Work

Rate spikes on DeFi platforms are often short-lived. A borrowing surge might push Aave's USDC rate to 8% for 48 hours before settling back to 4%. If you move capital to chase the spike, you arrive after the peak and earn the lower rate whilst having paid full transaction costs.

The reliable arbitrage opportunities come from structural differences — CeFi loyalty tiers, protocol incentive programmes, or sustained differences in borrowing demand across chains — rather than from momentary rate spikes. Monitor the seven-day moving average rate rather than the spot rate before making any reallocation decision.

What Changed in 2025-2026

MiCA Regulation Reshapes European Lending

The Markets in Crypto-Assets Regulation (MiCA), fully enforced across the EU from mid-2025, has had a measurable impact on lending rates for European users. Platforms operating under MiCA licences face higher compliance costs — capital reserves, audit requirements, and mandatory insurance — which they pass through as slightly lower APYs compared to unregulated competitors.

However, MiCA-licensed platforms have attracted significant institutional capital precisely because of that regulatory clarity, and some have seen their total lending pools grow by 40% to 60% since licensing. For retail lenders, the practical effect is a trade-off: rates on compliant platforms like Nexo and Crypto.com run 0.5% to 1% lower than offshore alternatives, but counterparty risk is materially reduced.

Ethena USDe and the Yield Disruption

Ethena's USDe synthetic dollar disrupted stablecoin lending markets throughout 2025 by offering sUSDe staking yields of 15% to 25% during bullish funding rate periods. This pulled capital away from traditional lending protocols, temporarily depressing rates on Aave and Compound as supply thinned.

However, sUSDe yields are directional — they depend on positive perpetual futures funding rates, which can turn negative during bearish markets. In Q4 2025, sUSDe yields dropped below 5% for several weeks during a market correction, sending capital flooding back to conventional lending. If you are considering USDe yields, understand that they are structurally different from lending rates: you are earning the carry trade, not interest from borrowers, and the risk profile reflects that difference.

Tokenised Treasuries Set a New Floor

Perhaps the most significant structural shift has been the growth of tokenised US Treasury products — BlackRock's BUIDL, Franklin Templeton's BENJI, Ondo's USDY, and others — offering 4.5% to 5% yields backed by short-duration government securities. These products have effectively set a risk-free rate floor for crypto lending markets.

Why would you lend USDC on Compound at 3.5% when you can earn 4.8% in a tokenised Treasury fund with substantially lower smart contract risk? As a result, DeFi lending protocols have had to offer rates above this floor to attract capital, which has been healthy for lenders but has compressed margins for platforms. When evaluating any lending rate below 5%, ask yourself whether you are being adequately compensated above the tokenised Treasury alternative.

Conclusion

Crypto lending rates in 2025-2026 reward informed capital allocation, not passive deposits. The combination of tokenised Treasury competition, MiCA compliance costs, and periodic yield disruptions from products like Ethena USDe means you cannot simply park stablecoins on one platform and forget about them. Track rates using DefiLlama, apply the 3x transaction cost rule before moving capital, and size your monitoring effort to your position — monthly for small balances, weekly for large ones.

The most reliable path to strong risk-adjusted returns is straightforward: diversify across two to three platforms spanning both CeFi and DeFi, favour regulated platforms for the bulk of your capital, and treat the tokenised Treasury floor of 4.5% to 5% as your minimum threshold for taking on smart contract or counterparty risk. Any lending rate below that floor should prompt you to question whether the risk is worth it when a near-risk-free alternative exists.

For UK residents specifically, keep meticulous records of every interest payment across all platforms. HMRC expects you to report crypto lending income on your Self Assessment tax return, and the tax liability at your marginal rate can meaningfully reduce your effective yield. A gross 8% APY becomes roughly 4.8% after higher-rate tax. Factor this into every platform comparison you make, especially when weighing CeFi convenience against DeFi rates.

Rates will continue shifting as regulation, protocol innovation, and macro conditions evolve. Your edge comes from understanding the mechanics well enough to respond calmly rather than chase every spike. Build your monitoring habits, set clear thresholds for when to act, and resist the temptation to over-optimise — the transaction costs and tax friction of constant rebalancing often erode the very gains you are chasing. Start with a small allocation, track your actual net returns honestly, and scale up only when your process consistently beats the tokenised Treasury baseline.

Sources & References

Frequently Asked Questions

- What drives crypto lending interest rates?

- Crypto lending rates are influenced by factors such as borrowing demand, platform liquidity, collateral requirements, market volatility, the regulatory environment, and platform-specific incentive programs.

- Are stablecoin lending rates more predictable?

- Stablecoin rates are generally more stable than volatile crypto assets, but they still fluctuate based on use rates, platform policies, and market demand for use.

- Should I choose fixed or variable rates?

- Variable rates offer flexibility and can capture rate increases. Meanwhile, fixed rates provide predictability. Choose based on your risk tolerance and market outlook.

- How often should I monitor lending rates?

- Check rates weekly for DeFi protocols and monthly for CeFi platforms. Set up alerts for large rate changes and regularly monitor platform announcements.

- What's a good diversification strategy?

- Spread funds across 3-5 reputable platforms, mix CeFi and DeFi options, diversify across different asset types, and maintain some highly liquid positions for flexibility.

- How do I calculate net returns?

- Calculate net APR by subtracting platform fees, transaction costs, and tax implications from gross rates. Also consider the volatility and liquidity of any token rewards.

- What are the biggest risks to watch?

- Key risks include platform insolvency, regulatory changes, smart contract vulnerabilities, market volatility, and liquidity constraints during stress periods.

- Are promotional rates sustainable?

- Promotional rates are typically temporary marketing tools. Always check the terms, duration, and the rates that revert after the promotional period ends.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.