Crypto Loan-to-Value (LTV) Ratio Guide

Complete guide to understanding, calculating, and optimising LTV ratios for safe cryptocurrency borrowing in 2025.

Introduction

The loan-to-value (LTV) ratio is the single number that determines whether your crypto loan survives a market crash or gets liquidated. The formula is simple -- LTV = (Loan Amount / Collateral Value) x 100% -- but the consequences of getting it wrong are severe. During the May 2022 crash, borrowers at 75% LTV on volatile altcoins were liquidated within hours, losing their collateral plus 5-15% in liquidation penalties. Borrowers at 35% LTV on the same assets rode out the storm without a margin call.

Here is what the numbers look like across major platforms as of mid-2026. On Nexo, Bitcoin and Ethereum max LTV is 50% with liquidation at 83.3%. On Aave, ETH max LTV is 80% with liquidation at 82.5% — a buffer of just 2.5%. On Compound, ETH collateral factor is 82.5%. On Sky (formerly MakerDAO, rebranded August 2024), ETH-A vaults still require 170% minimum collateralisation (effectively 58.8% max LTV), and the underlying vault contracts continued to operate through the rebrand. These differences matter enormously: borrowing at 75% LTV on Aave gives you a 7.5% price buffer before liquidation, whilst the same LTV on Nexo would exceed the platform maximum entirely.

A worked example makes the risk concrete. You deposit 5 ETH at $3,000 each ($15,000 collateral) and borrow $7,500 USDC on Aave (50% LTV). Your health factor is 1.65 -- comfortable. If ETH drops 20% to $2,400, your collateral is now $12,000 and your LTV jumps to 62.5% (health factor 1.32). If ETH drops 40% to $1,800, your collateral is $9,000, LTV is 83.3%, and you are past Aave's 82.5% liquidation threshold -- the protocol automatically sells up to 50% of your collateral at a 5% discount. You lose roughly $2,250 in ETH plus the penalty. Had you borrowed at 33% LTV ($5,000), ETH would need to fall 60% before liquidation.

This guide covers platform-specific LTV limits, worked liquidation examples at different price levels, and practical strategies for choosing the right LTV for your risk tolerance. The golden rule: your target LTV should be no more than 50-65% of the platform's maximum, giving you a meaningful buffer against the 20-40% drawdowns that occur regularly in crypto markets. For borrowers using volatile altcoins like SOL or AVAX as collateral, that target should be even lower — closer to 40-50% of the maximum — because altcoins can drop 30% in a single day during sell-offs, leaving almost no time to react. Throughout this guide, every recommendation includes the specific LTV ranges, liquidation prices, and platform mechanics so you can make informed borrowing decisions rather than guessing at safe levels.

What is the LTV Ratio in cryptocurrency loans?

The Loan-to-Value (LTV) ratio measures how much you can borrow relative to your collateral value. It's the fundamental metric determining loan size and liquidation risk.

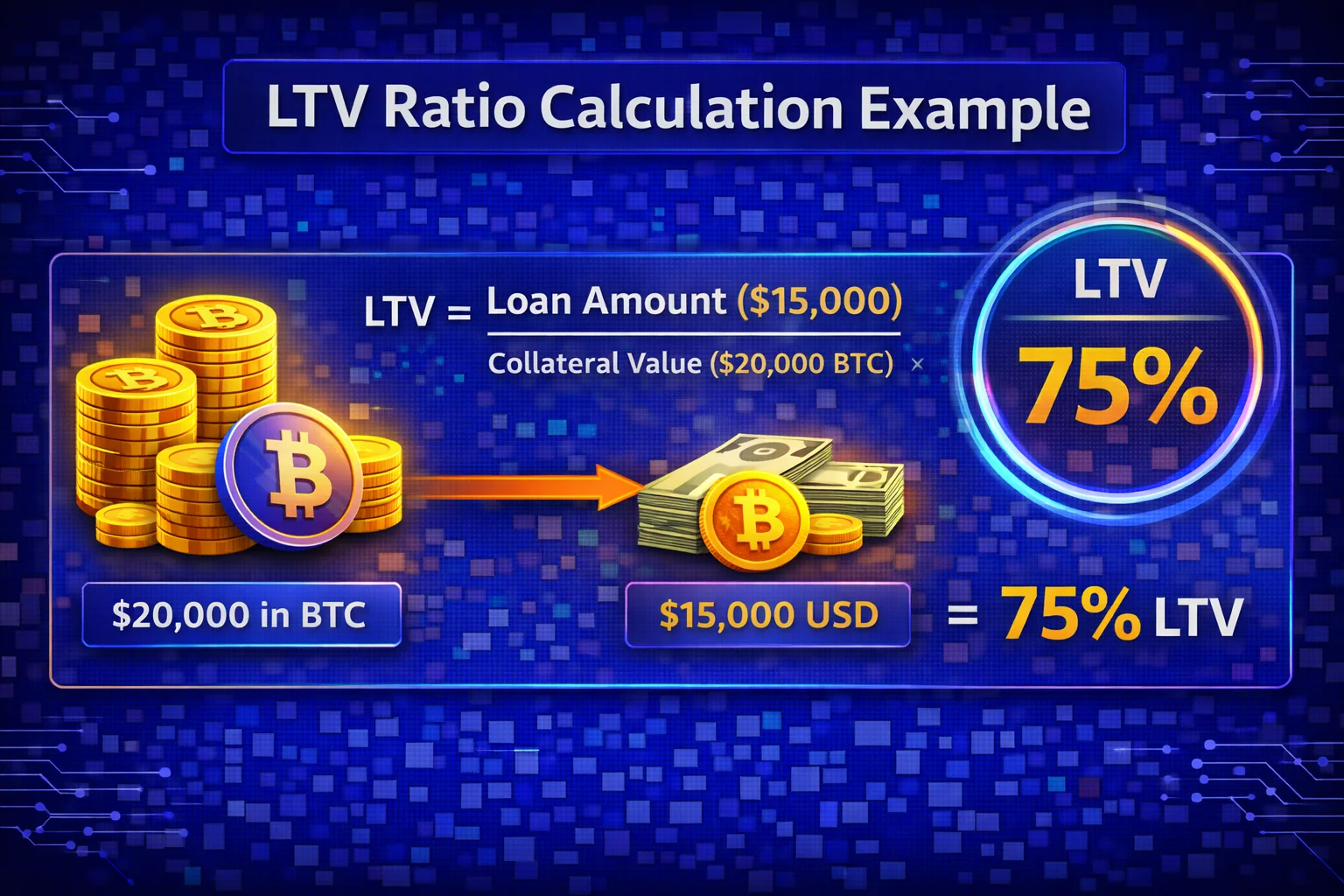

LTV Formula

LTV = (Loan Amount / Collateral Value) × 100%

Simple Example

- Collateral: $10,000 worth of Bitcoin

- Loan: $5,000 USDT

- LTV: ($5,000 / $10,000) × 100% = 50%

Why LTV Matters

- Determines Loan Size: Higher LTV = more borrowing capacity

- Affects Liquidation Risk: Higher LTV = closer to liquidation

- Impacts Interest Rates: Some platforms charge more for higher LTV

- Reflects Risk Level: Lower LTV = safer position

Understand collateral basics in our collateral guide.

How to Calculate LTV Ratio

Step-by-Step Calculation

Step 1: Check Your Collateral Value

Look up the current price of your crypto on CoinGecko or your exchange. If you hold 2 ETH and ETH trades at £2,500, your collateral is worth £5,000. Use the price at the moment you deposit — not what you paid for it.

Step 2: Decide How Much to Borrow

Determine the exact amount you need in stablecoins or fiat. If you need £2,000 for a specific expense, borrow exactly £2,000 — not more "just in case." Extra borrowing increases your LTV and liquidation risk for no benefit.

Step 3: Calculate Your LTV

LTV = (Loan Amount / Collateral Value) × 100. In this example: £2,000 / £5,000 = 40% LTV. This is a healthy ratio — your collateral could drop 50% before reaching a typical 80% liquidation threshold on Aave. Write down your LTV and your liquidation price before confirming the transaction.

Reverse Calculation: How Much Can You Safely Borrow?

If you hold £10,000 in ETH and Aave offers 80% max LTV, the maths says you can borrow up to £8,000. Do not do this. At 80% LTV, a 5% ETH drop puts you in liquidation territory. Instead, calculate your safe borrowing limit at 40-50% LTV:

- Collateral: £10,000 in ETH

- Maximum loan (80% LTV): £8,000 — dangerous, liquidated by a 5% dip

- Moderate loan (50% LTV): £5,000 — survives a 35% crash before liquidation

- Conservative loan (35% LTV): £3,500 — survives a 50%+ crash, sleep-at-night comfortable

The difference between 50% and 80% LTV is not 30% more borrowing power — it is the difference between surviving a normal market correction and losing your collateral to automated liquidation bots at the worst possible time.

Dynamic LTV Changes

Price Increase Scenario

- Initial: $10,000 collateral, $5,000 loan = 50% LTV

- ETH +20%: $12,000 collateral, $5,000 loan = 41.7% LTV

- Result: LTV improves, safer position

Price Decrease Scenario

- Initial: $10,000 collateral, $5,000 loan = 50% LTV

- ETH -20%: $8,000 collateral, $5,000 loan = 62.5% LTV

- Result: LTV worsens, approaching liquidation

Interest Impact on LTV

Loan value increases over time due to interest:

- Month 1: $5,000 loan at 8% APR

- Month 6: $5,200 loan (with interest)

- LTV Change: 50% → 52% (if collateral stable)

Platform LTV Limits

CeFi Platform LTV Ratios

Nexo

- Bitcoin: Up to 50% LTV

- Ethereum: Up to 50% LTV

- Stablecoins: Up to 90% LTV

- Altcoins: 20-33% LTV

- Liquidation: Varies by tier and asset

Crypto.com

- Bitcoin/Ethereum: Up to 50% LTV

- Stablecoins: Up to 50% LTV

- Other Assets: 25-40% LTV

YouHodler

- Bitcoin: Up to 70% LTV

- Ethereum: Up to 70% LTV

- Stablecoins: Up to 90% LTV

- Note: Higher LTV = higher risk

DeFi Protocol LTV Ratios

Aave

- Bitcoin (WBTC): 70% max LTV, 75% liquidation

- Ethereum: 80% max LTV, 82.5% liquidation

- Stablecoins: 75-80% max LTV

- E-Mode: Up to 97% LTV for correlated assets

Compound

- Bitcoin (WBTC): 70% collateral factor

- Ethereum: 82.5% collateral factor

- Stablecoins: 75-85% collateral factor

Sky (formerly MakerDAO)

- ETH-A: 170% min collateral (58.8% max LTV)

- WBTC-A: 175% min collateral (57.1% max LTV)

- USDC-A: 101% min collateral (99% max LTV)

Understanding Liquidation Thresholds

Liquidation threshold is always higher than max LTV:

- Max LTV: Maximum you can borrow initially

- Liquidation Threshold: LTV at which liquidation triggers

- Buffer: Difference between max and liquidation

Example (Aave ETH):

- Max LTV: 80%

- Liquidation: 82.5%

- Buffer: 2.5% (very small!)

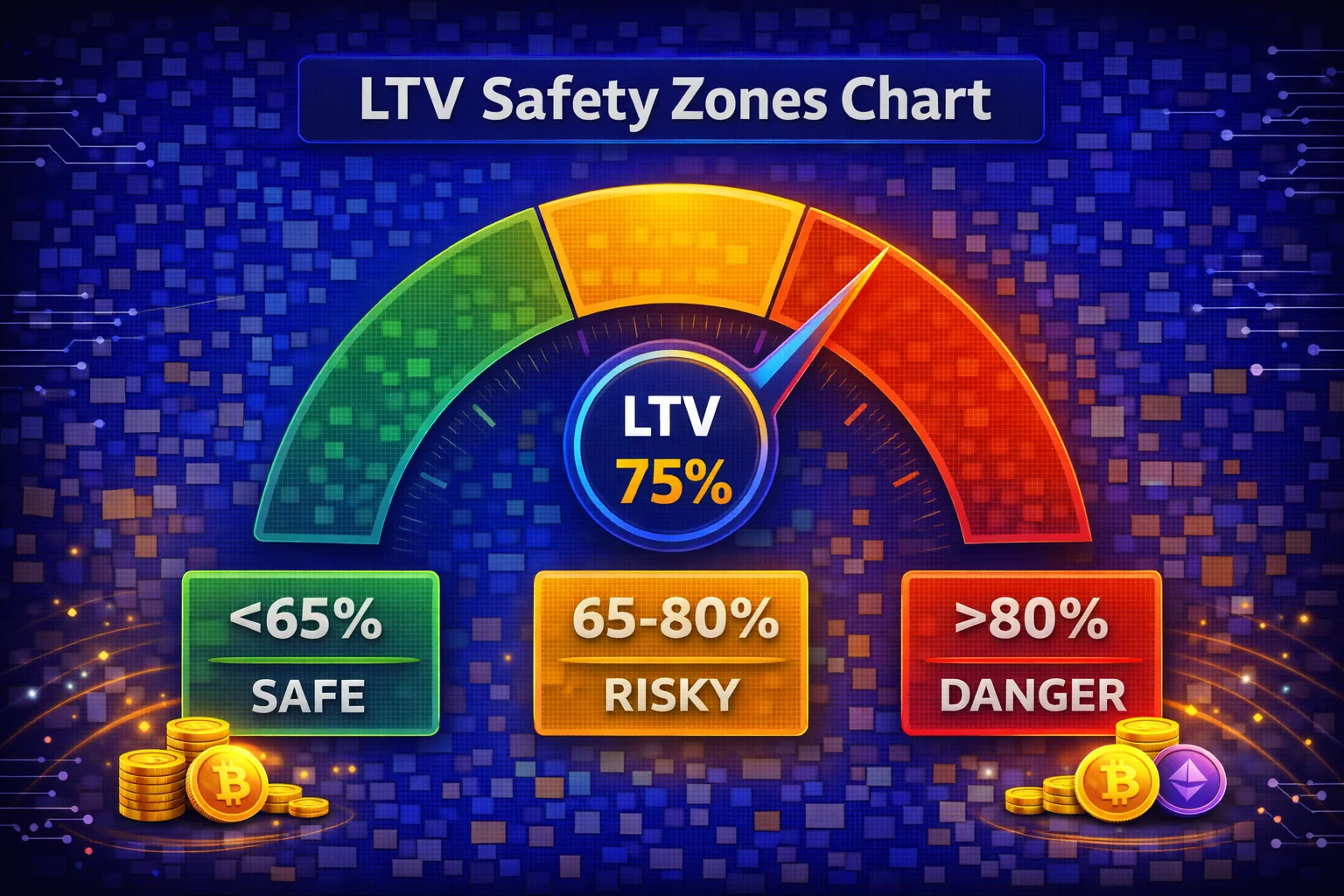

Optimal LTV Ratios for Safety

Conservative LTV Recommendations

By Asset Volatility

- Bitcoin (Low Volatility): 30-40% LTV

- Ethereum (Moderate): 25-35% LTV

- Major Altcoins (High): 20-30% LTV

- Stablecoins (None): 70-80% LTV

By Risk Tolerance

- Conservative: 20-30% LTV (large buffer)

- Moderate: 30-40% LTV (balanced)

- Aggressive: 40-50% LTV (higher risk)

- Dangerous: 50%+ LTV (not recommended)

LTV Strategy by Market Conditions

Bull Market

- Strategy: Can use slightly higher LTV (40-50%)

- Reason: Collateral likely to appreciate

- Caution: Bull markets end suddenly

Bear Market

- Strategy: Use very low LTV (20-30%)

- Reason: Collateral likely to depreciate

- Safety: Large buffer protects from crashes

High Volatility

- Strategy: minimise LTV (20-25%)

- Reason: Rapid price swings increase risk

- Alternative: Use stablecoin collateral

Choosing the right LTV ratio is ultimately about understanding the relationship between your borrowing need and your tolerance for forced liquidation. A borrower who needs £5,000 for a time-sensitive business expense has a different risk calculus than someone farming yield with borrowed stablecoins. The first borrower faces a concrete deadline and cannot afford to lose their collateral to a flash crash at the wrong moment, making a 25-30% LTV the only sensible choice. The second borrower can unwind their position at any time, making a slightly higher LTV of 35-40% acceptable because they have the flexibility to repay the loan if market conditions deteriorate.

The concept of "safe" LTV is relative to the specific collateral asset and the historical volatility of that asset. Bitcoin, despite its reputation for volatility, has never dropped more than 50% within a seven-day period since 2019. Ethereum has experienced drops of up to 55% in a single week during extreme events like the May 2022 Terra collapse. Altcoins such as SOL, AVAX, and LINK regularly experience 30-40% weekly drawdowns during bear markets. These historical patterns suggest that a 35% LTV on Bitcoin provides a buffer against all but the most extreme weekly scenarios, whilst the same LTV on a mid-cap altcoin like AVAX leaves you uncomfortably close to liquidation during routine market corrections.

UK borrowers should also consider the timing dimension of LTV management. If you borrow against ETH at 35% LTV in January and ETH rises 40% by April, your effective LTV has dropped to 25% — well within the conservative zone. Many borrowers use this collateral appreciation to borrow additional stablecoins, returning their LTV to 35%. While this strategy captures the upside of collateral appreciation, it also means you are continuously increasing your total debt. If ETH then drops 30% from its April peak, your larger debt position results in a higher LTV than if you had left the original loan unchanged. This ratcheting effect catches many borrowers off guard because they focus on the LTV percentage without tracking the absolute debt growth.

For positions above £10,000, consider splitting your collateral across two platforms rather than concentrating on one. Depositing half your ETH on Aave and half on Nexo, each at 35% LTV, provides diversification against platform-specific risks including smart contract exploits, governance parameter changes, or sudden rate increases. If Aave governance votes to reduce the ETH liquidation threshold from 82.5% to 80%, only half your position is affected. This split does increase management overhead, but for larger portfolios the protection against concentrated platform risk justifies the extra ten minutes per week of monitoring.

The relationship between LTV and interest rates is often overlooked. On CeFi platforms like Nexo, higher LTV tiers may carry higher interest rates. Borrowing at 50% LTV on Nexo costs 6.9% APR for non-loyalty users, whilst borrowing at 33% LTV costs the same rate — there is no reward for lower LTV on this platform. On Aave, however, borrowing rates are uniform regardless of your individual LTV. The implication: on platforms with flat rate structures, there is no economic incentive to borrow less (beyond liquidation protection), while on tiered platforms, maintaining a lower LTV can simultaneously reduce both your liquidation risk and your borrowing cost.

LTV optimisation Examples

Example 1: Conservative Bitcoin Loan

- Collateral: 1 BTC at $50,000

- Target LTV: 30%

- Loan Amount: $15,000

- Liquidation Buffer: 40-50% price drop before liquidation

Example 2: Moderate Ethereum Loan

- Collateral: 10 ETH at $2,500 = $25,000

- Target LTV: 35%

- Loan Amount: $8,750

- Liquidation Buffer: 35-45% price drop

Example 3: Stablecoin Efficiency

- Collateral: $50,000 USDC

- Target LTV: 75%

- Loan Amount: $37,500

- Risk: Minimal (stablecoin depeg only)

LTV Management Strategies

Monitoring Your LTV

Daily Checks

- Check current LTV on platform dashboard

- Compare to your target safe LTV

- Note distance to liquidation threshold

- Track collateral price trends

Alert Setup

- Warning Level: LTV reaches 45% (if target is 35%)

- Action Level: LTV reaches 50%

- Critical Level: LTV reaches 55%

Improving Your LTV

Method 1: Add Collateral

Current: $10,000 collateral, $5,000 loan = 50% LTV

Add $2,000 collateral:

- New collateral: $12,000

- New LTV: $5,000 / $12,000 = 41.7%

- Improvement: 8.3 percentage points

Method 2: Repay Loan

Current: $10,000 collateral, $5,000 loan = 50% LTV

Repay $1,000:

- New loan: $4,000

- New LTV: $4,000 / $10,000 = 40%

- Improvement: 10 percentage points

Method 3: Combination

- Add $1,000 collateral

- Repay $500 loan

- New LTV: $4,500 / $11,000 = 40.9%

LTV Rebalancing Schedule

Monthly Rebalancing

- Review LTV on 1st of each month

- If above target, add collateral or repay

- If well below target, consider borrowing more

Event-Based Rebalancing

- After 10% Price Drop: Check and adjust

- After 20% Price Drop: Immediate action

- After Profit Taking: Repay portion of loan

Advanced LTV Strategies

Laddered LTV Approach

Implement multiple loans with different LTV ratios to optimise risk and capital efficiency. This strategy involves creating several smaller positions rather than one large loan, allowing for more granular risk management and flexible adjustment options.

- Conservative Tier (25% LTV): Core position with maximum safety margin

- Moderate Tier (35% LTV): Balanced risk-reward positioning

- Aggressive Tier (45% LTV): Higher yield with increased monitoring requirements

Dynamic LTV Management

Adjust your target LTV based on market conditions, volatility levels, and personal risk tolerance. During bull markets, you might accept higher LTV ratios, while bear markets require more conservative positioning.

- Bull Market Strategy: Target 40-50% LTV for maximum capital efficiency

- Bear Market Strategy: Target 20-30% LTV for enhanced safety margins

- Sideways Market: Target 30-40% LTV for balanced approach

- High Volatility: Reduce target LTV by 10-15 percentage points

Cross-Platform LTV optimisation

Different lending platforms offer varying LTV limits and liquidation thresholds. Advanced users can optimise their overall position by utilising multiple platforms strategically, taking advantage of each platform's unique features and risk parameters.

- Platform A: Conservative LTV for stable income generation

- Platform B: Moderate LTV for balanced growth

- Platform C: Higher LTV for short-term opportunities

Split collateral across multiple loans with different LTV ratios:

- Loan 1: 30% LTV (ultra-safe)

- Loan 2: 40% LTV (moderate)

- Loan 3: 50% LTV (aggressive)

- Benefit: Diversified risk, partial liquidation only

Dynamic LTV Adjustment

- Bull Market: Gradually increase LTV to 45-50%

- Bear Market: Reduce LTV to 25-30%

- Sideways: Maintain moderate 35-40%

Learn protection strategies in our liquidation protection guide.

Psychology of LTV Management

Emotional Decision-Making Traps

Understanding psychological factors helps maintain disciplined LTV management during market volatility.

Common Psychological Mistakes

- Greed During Bull Markets: Borrowing at maximum LTV when prices rise, assuming they'll continue. This leaves no buffer for inevitable corrections.

- Fear During Bear Markets: Panic-closing positions at losses instead of adding collateral. Often results in realising losses unnecessarily.

- Overconfidence Bias: Believing "this time is different" and ignoring historical volatility patterns. Markets always revert to volatility eventually.

- Anchoring to Entry Price: Refusing to adjust strategy when market conditions change fundamentally.

Disciplined LTV Framework

Rule-Based Approach

Remove emotions by following predetermined rules. Write these down before your first loan and tape them next to your monitor:

- Maximum LTV Rule: Never exceed 50% LTV regardless of market sentiment. During the November 2021 peak, borrowers who stretched to 70% LTV on ETH were liquidated within 60 days as ETH fell from £3,400 to £1,700

- Rebalancing Rule: Add collateral when LTV exceeds 45%, no exceptions. Automate this with DeFi Saver for Aave positions (costs 0.25% per trigger) or rely on Nexo's margin call notifications for CeFi loans

- Profit-Taking Rule: Repay 20% of loan when collateral appreciates 30%+. This locks in improved LTV and reduces your total interest cost. On a £10,000 loan at 8% APR, repaying £2,000 after a rally saves £160 in annual interest

- Emergency Rule: Close position if unable to maintain safe LTV for 30+ days. Borrowing against crypto should never require you to inject new money you cannot afford to lose. If you are scrambling to find collateral top-ups, the position is too large for your financial situation

Stress Testing Your LTV

Before borrowing, test your strategy against actual historical scenarios — not hypothetical ones:

- May 2021 crash: BTC dropped 53% in 10 weeks (£44,000 to £20,700). At 40% LTV, your position would have reached 85% LTV — past liquidation on most platforms. At 30% LTV, you would have reached 64% LTV — uncomfortable but survivable

- 2022 bear market: BTC fell 77% over 12 months. ETH fell 82%. Any LTV above 25% on BTC or 20% on ETH would have been liquidated at some point during this decline. Only borrowers at extremely conservative ratios survived without intervention

- March 2020 "Black Thursday": BTC dropped 40% in a single day. Even DeFi protocols struggled — MakerDAO experienced a liquidation crisis where some vaults were liquidated at $0 because liquidation bots failed during extreme network congestion. This is why CeFi platforms like Nexo, which provide margin call warnings and partial liquidation, offer a practical safety advantage during flash crashes

If you cannot survive the 2022 scenario (77% BTC decline) without adding collateral or closing the loan, reduce your LTV or loan size. That bear market was not historically unusual — BTC has experienced 80%+ drawdowns in every cycle since 2011.

Worked LTV Stress Test for a UK Investor

You hold 2 BTC (purchased at £15,000 each, current price £50,000, total value £100,000). You borrow £30,000 GBP via Nexo at 30% LTV to fund a buy-to-let deposit without selling BTC and triggering £67,000 in CGT gains.

- Comfortable zone (BTC above £30,000): LTV stays below 50%. No action needed. Monitor weekly

- Warning zone (BTC £22,000-30,000): LTV reaches 50-68%. Add stablecoin collateral or repay £5,000-10,000 of the loan. At Nexo's 8.9% APR (Gold tier), the annual interest on £30,000 is £2,670 — factor this into your cash flow

- Danger zone (BTC below £22,000): LTV exceeds 68%. Nexo will issue a margin call. You need £5,000-10,000 in additional collateral within 24 hours. If you cannot provide it, Nexo liquidates the minimum BTC needed to restore the ratio. The forced sale triggers CGT on any gain above your £15,000 per-BTC cost basis

- Liquidation (BTC at £18,000): LTV hits Nexo's 83.3% threshold. Automatic liquidation sells approximately 0.5-1.0 BTC at market price. Even during a crash, HMRC treats this as a disposal: if BTC is liquidated at £18,000 and your cost basis is £15,000, you owe CGT on the £3,000 gain per BTC — despite losing money in practical terms because the liquidation happened during a crash

Advanced LTV Management Strategies

Dynamic LTV Rebalancing

Professional borrowers implement systematic rebalancing strategies to maintain optimal LTV ratios. This involves setting specific thresholds for adding collateral or reducing debt based on market conditions and volatility patterns.

Automated Rebalancing Systems

Advanced platforms offer automated tools that monitor your LTV ratio continuously and execute predefined actions when thresholds are reached. These systems can automatically add collateral from connected wallets or partially repay loans to maintain safe LTV levels.

Multi-Asset Collateral optimisation

Sophisticated borrowers diversify collateral across multiple assets to reduce correlation risk. By using a basket of uncorrelated assets (Bitcoin, Ethereum, stablecoins, and tokenised real-world assets), you can achieve more stable LTV ratios even during market volatility.

Cross-Platform LTV Arbitrage

Different platforms offer varying LTV ratios for the same assets. Advanced users can exploit these differences by borrowing on platforms with higher LTV limits while maintaining conservative ratios, then using borrowed funds on platforms with better rates or features.

Platform Comparison Strategy

Regularly compare LTV offerings across platforms. For example, if Platform A offers 70% LTV on ETH while Platform B offers 60%, you might use Platform A for borrowing while keeping your actual LTV at 40% for safety, giving you more borrowing capacity.

Hedging Strategies for LTV Protection

Professional borrowers use derivatives to hedge against adverse price movements that could increase their LTV ratios. This includes using perpetual swaps, options, or futures to create delta-neutral positions.

Perpetual Funding Arbitrage

By shorting perpetual contracts equal to your collateral value, you can create a market-neutral position that generates funding rate income while protecting against LTV increases due to price drops.

Institutional LTV Management

Large borrowers and institutions employ sophisticated risk management frameworks that include stress testing, value-at-risk calculations, and correlation analysis across their entire portfolio of crypto loans.

Portfolio-Level LTV optimisation

Instead of managing individual loan LTVs, institutions optimise at the portfolio level, considering correlations between different collateral assets and borrowing positions across multiple platforms and strategies.

LTV Management Across Market Cycles

Bull Market LTV Strategies

During bull markets, collateral values increase, naturally reducing LTV ratios. This creates opportunities to either borrow more or maintain ultra-conservative ratios for maximum safety. However, bull markets can also create overconfidence, leading to dangerous LTV increases.

Bull Market Best Practices

- Resist overleverage: Don't increase borrowing just because LTV ratios improve

- Take profits: Use improved ratios to partially repay loans and lock in gains

- Prepare for reversals: Bull markets don't last forever; maintain conservative ratios

- Diversify timing: Don't add all collateral at market peaks

Bear Market LTV Management

The 2022 bear market tested every borrower's LTV discipline. BTC fell from $69,000 (November 2021) to $16,000 (November 2022) — a 77% decline over 12 months. ETH dropped from $4,800 to $880 (82%). Borrowers who started the bear market at 30% LTV had time to adjust. Those at 60% LTV faced liquidation within the first major leg down.

Bear Market Survival Tactics

- Emergency stablecoin reserve: Keep at least 20% of your collateral value in USDC or USDT, ready to inject instantly. If your loan is backed by £20,000 in ETH, hold £4,000 in stablecoins on the same platform. This buys you an additional 20% price drop buffer before liquidation

- Gradual deleveraging: As prices decline, repay 10-20% of your loan with each 15% market drop. This progressively reduces your LTV even as collateral values fall. If you cannot afford to repay, your position is too large for your financial situation

- Exit thresholds: Set a hard rule: if your collateral drops below a price level you believe is structurally broken (for example, ETH below its previous cycle high), close the loan entirely rather than continuing to add collateral into a potentially deeper decline

Sideways Market optimisation

Range-bound markets offer unique opportunities for LTV optimisation. With reduced volatility, borrowers can operate at slightly higher LTV ratios while implementing systematic rebalancing strategies.

Range Trading with Loans

In sideways markets, some borrowers use their loans for range trading strategies, buying at support levels and selling at resistance while maintaining strict LTV discipline throughout the process.

Regulatory and Tax Implications of LTV Management

UK Tax Implications of LTV Management

The core tax advantage of crypto borrowing for UK investors: borrowing against crypto is NOT a disposal event for CGT purposes. If you bought 1 BTC at £20,000 and it is now worth £60,000, selling triggers a £40,000 gain (taxable at 24% for higher-rate taxpayers after the £3,000 annual allowance = approximately £8,880 in CGT). Borrowing £20,000 against that same BTC costs roughly £1,000-2,800 in annual interest depending on the platform, while preserving the asset for future appreciation. The tax saving alone can exceed the interest cost.

Tax Events in LTV Management

- Depositing collateral: NOT a taxable disposal under HMRC guidance — you retain beneficial ownership

- Liquidation: IS a taxable disposal at the liquidation price. Gain or loss calculated against your Section 104 pool cost basis. A forced liquidation during a crash often produces a gain (because your cost basis may be lower than the crash price) — resulting in tax owed despite losing money in practical terms

- Repaying a loan by selling crypto: The sale is a CGT disposal. If you sell ETH to generate USDC to repay an AAVE loan, the ETH sale triggers CGT

- DeFi Saver auto-repay: Each automated collateral sale is a separate taxable disposal. If DeFi Saver triggers 5 times during a crash, that is 5 CGT events to track. Use crypto tax software from day one

- Interest payments: If paid in crypto (some DeFi protocols deduct from collateral), the crypto used is a disposal for CGT purposes. If paid in fiat, no CGT event — but the interest expense is NOT tax-deductible for individual UK borrowers unless the loan is for a qualifying business purpose

UK Regulatory Status of Crypto Lending

The FCA currently regulates crypto firms for AML purposes, not as lending businesses. Crypto loans are not covered by the Consumer Credit Act, which means FCA consumer protections (affordability checks, cooling-off periods, unfair terms provisions) do not apply. FSCS deposit protection (£85,000) does not cover any crypto lending platform. Borrowers have no FOS complaints process if a platform disputes their collateral valuation or liquidation timing.

The Financial Services and Markets Act 2023 granted the FCA broader powers over crypto, and specific lending regulations are expected in 2025-2026. Until then, UK crypto borrowers rely entirely on the platform's terms of service and their own risk management. Choose platforms with EU or UK FCA registration (Nexo holds both), published proof of reserves, and a track record through the 2022 bear market.

Getting Started: Your First Crypto Loan in 7 Steps

Step 1: Decide How Much to Borrow and Why

Define the exact purpose and amount before opening any platform. Borrowing £5,000 for a house deposit has different LTV requirements than borrowing £500 to buy a dip. The larger the loan and the longer the expected duration, the lower your starting LTV should be. For loans you intend to hold for 6+ months, target 30-40% LTV. For short-term needs (under 30 days), 50% LTV is acceptable if you monitor daily.

Step 2: Choose Your Platform Based on Your Collateral

If you hold BTC or ETH and want simplicity, Nexo offers instant credit lines with no fixed repayment schedule — borrow today, repay whenever you choose. If you hold DeFi tokens or want lower rates, Aave provides the cheapest borrowing costs (variable, currently 2-5% for stablecoins) but requires managing a MetaMask wallet and paying Ethereum gas fees. For BTC-only holders who want zero DeFi complexity, Nexo or Binance Loans are the practical choices.

Step 3: Calculate Your Liquidation Price

Before depositing a single pound of collateral, calculate the exact price at which you would be liquidated. Use this formula: Liquidation Price = (Loan Amount ÷ Collateral Quantity) ÷ (1 - Liquidation Threshold). For example, depositing 1 ETH at £3,000 and borrowing £1,500 USDC on Aave (liquidation threshold 82.5%): Liquidation Price = (£1,500 ÷ 1) ÷ 0.825 = £1,818. If ETH drops below £1,818, you face liquidation. Ask yourself: has ETH ever traded at £1,818 in the past 2 years? If yes, your LTV is too high.

Step 4: Deposit Collateral and Borrow

On Nexo: transfer crypto to your Nexo account, navigate to the credit line section, select the amount to borrow and the currency (GBP, EUR, USDC), and confirm. Funds appear in your account within minutes. On Aave: connect MetaMask, deposit collateral via the "Supply" tab, switch to the "Borrow" tab, select the stablecoin and amount, confirm the transaction (gas cost: £5-30 depending on network congestion).

Step 5: Set Up Monitoring and Alerts

On Nexo, enable email and push notification alerts (enabled by default). On Aave, use DeFi Saver's free monitoring tier — connect your wallet, set health factor alerts at 1.5 and 1.2, and receive Telegram or email notifications. Also set a CoinGecko price alert at your calculated liquidation price from Step 3.

Step 6: Establish Your Emergency Plan

Keep 20% of your borrowed amount in stablecoins in the same wallet (for DeFi) or the same platform (for CeFi), ready to inject as emergency collateral. Write down the exact steps you will take if the price drops 20%, 40%, and 60%. Decide in advance whether you will add collateral, partially repay, or accept liquidation at each level. Making these decisions calmly in advance prevents panic decisions at 3am during a crash.

Step 7: Monthly Review

Set a monthly calendar reminder to review: current LTV, interest accrued, collateral price trend, and whether the loan still serves its original purpose. If rates have spiked or market conditions have deteriorated, consider partial repayment. If your collateral has appreciated significantly and your LTV has dropped below 25%, consider withdrawing excess collateral to reduce platform exposure.

Advanced LTV Strategies and Professional Risk Management

Worked LTV Scenarios Across Market Conditions

Scenario 1: Conservative approach (recommended for most borrowers). You deposit 3 BTC at $60,000 ($180,000 collateral) on Nexo and borrow $54,000 USDC (30% LTV). Nexo's liquidation threshold for BTC is 83.3% LTV. For your LTV to reach 83.3%, your collateral value would need to fall to $64,830 -- meaning BTC would need to drop to approximately $21,600, a 64% decline. Even during the 2022 bear market (BTC fell from $69,000 to $16,000, roughly 77%), you would have had time to add collateral or partially repay. At 30% LTV, you can sleep through a crash.

Scenario 2: Moderate risk (experienced borrowers). You deposit 10 ETH at $3,000 ($30,000 collateral) on Aave and borrow $15,000 USDC (50% LTV). Aave's ETH liquidation threshold is 82.5%. Your liquidation price is approximately $1,818 per ETH (a 39% drop). During the May 2022 crash, ETH fell 40% in a week. At 50% LTV, you would have been liquidated. This is why DeFi Saver automation matters: set it to auto-repay when health factor drops below 1.5 (roughly 55% LTV equivalent), boosting back to 1.8. Cost: 0.25% per automation trigger plus gas.

Scenario 3: Aggressive (not recommended). Same 10 ETH on Aave, but borrowing $22,500 USDC (75% LTV). Your liquidation price is $2,727 per ETH -- just a 9% drop. A normal daily fluctuation can liquidate you. Aave's 2.5% buffer between max LTV (80%) and liquidation (82.5%) provides almost no protection. This is gambling, not borrowing.

Automated LTV Protection Tools

DeFi Saver is the most popular automated LTV management tool. It monitors your Aave, Compound, or MakerDAO position and automatically repays debt (selling collateral) or adds collateral (if you have pre-deposited funds) when your health factor crosses a threshold you define. Cost: 0.25% service fee per automation transaction plus Ethereum gas fees. Setup takes 5 minutes through their web interface. For a $50,000 position, expect to pay $5-20 per automation trigger depending on gas prices.

Instadapp provides one-click leverage adjustment and cross-protocol refinancing. If Aave's variable borrow rate spikes above Compound's, you can migrate your entire position in a single transaction. Instadapp also offers automated rebalancing between protocols to maintain the best rates. Free to use (you only pay gas).

Manual approach (for smaller positions under $10,000): Set price alerts on CoinGecko or TradingView at multiple levels corresponding to your liquidation thresholds. Keep 20% of your position value in stablecoins in the same wallet, ready to inject as emergency collateral. Check your health factor daily -- it takes 30 seconds on the Aave or Compound dashboard.

Tax Implications of LTV Management

In the UK, borrowing against crypto is not itself a taxable event -- HMRC does not treat taking a loan as a disposal. However, if your position is liquidated, the forced sale of collateral triggers Capital Gains Tax on any gain above your cost basis. Adding collateral is not taxable. Repaying a loan by selling crypto to generate fiat is a disposal event for CGT purposes. If you use DeFi Saver's auto-repay feature (which sells collateral to repay debt), each automation trigger is a taxable disposal. Track these with Koinly or similar software -- DeFi Saver transactions are standard Ethereum transactions that tax software can import automatically.

Platform Selection Checklist for LTV Safety

Not all platforms handle liquidation the same way. Before depositing collateral, verify these five factors:

- Partial vs full liquidation: Nexo sells only the minimum collateral needed to restore your LTV. Aave liquidates up to 50% of your position in a single transaction. MakerDAO liquidates 100% with a 13% penalty. This difference dramatically affects your outcome — partial liquidation preserves most of your position, whilst full liquidation can wipe out collateral that would have recovered in value within days

- Liquidation penalty: Aave charges 5% on ETH, 10% on less liquid assets. Binance charges 2%. Nexo charges no explicit penalty but sells at market price during volatile conditions, which can be worse. Calculate the cost of a hypothetical liquidation before borrowing

- Margin call warning: CeFi platforms (Nexo, Binance) send margin call notifications via email and push, giving you hours to act. DeFi protocols (Aave, Compound) have no margin calls — liquidation bots execute automatically the moment your health factor drops below 1.0, often within the same block. If you use DeFi, automated protection tools are not optional

- Withdrawal speed: Can you add collateral within minutes? On Aave, collateral addition is a single transaction (30 seconds). On Nexo, if your collateral is in a different wallet, the transfer time plus confirmation time can take 10-60 minutes depending on the blockchain. During a crash, 60 minutes is an eternity

- Insurance coverage: Nexo's $775M insurance covers custody breaches (hacking), not insolvency or market losses. Aave has no insurance — purchase Nexus Mutual coverage separately (2-5% annually) for positions above £10,000. No insurance product covers liquidation losses caused by price drops

Conclusion: Mastering LTV for DeFi lending Success

Understanding and managing loan-to-value ratios is fundamental to successful crypto lending, representing the cornerstone of effective risk management in the volatile cryptocurrency market. The difference between profitable borrowing and devastating liquidation often comes down to disciplined LTV management, conservative risk-taking, and the ability to maintain emotional control during periods of market stress when the temptation to increase leverage is highest.

Key Principles for Success

- Conservative approach: Always maintain LTV ratios well below platform maximums to provide adequate safety margins

- Continuous monitoring: Check your positions regularly, especially during volatile periods when prices can change rapidly

- Emergency planning: Have clear procedures for adding collateral or repaying loans quickly when market conditions deteriorate

- Platform diversification: Don't put all your borrowing on a single platform to reduce counterparty risk

- Market awareness: Adjust strategies based on market conditions, volatility levels, and macroeconomic factors

- Psychological discipline: Resist the urge to increase leverage during bull markets or panic during corrections

- Continuous education: Stay informed about platform updates, new features, and evolving best practices

Remember that crypto lending is a powerful tool for accessing liquidity without selling your assets, but it requires respect for the risks involved and a thorough understanding of the mechanics that govern liquidation events. By maintaining conservative LTV ratios, implementing proper risk management protocols, and staying informed about market conditions and platform developments, you can use crypto loans effectively while protecting your capital from the extreme volatility that characterizes cryptocurrency markets.

The crypto lending landscape continues to evolve with new platforms, innovative features, and developing regulatory frameworks that create both opportunities and challenges for borrowers. Success in this environment requires staying educated about these developments, starting conservatively with small positions, and gradually building your expertise as you gain experience with different platforms and market conditions. The most successful crypto borrowers treat LTV management as an active discipline rather than a set-and-forget strategy, adapting their approach based on changing market dynamics while maintaining unwavering focus on capital preservation.

One aspect that many borrowers overlook is how interest accrual itself affects your LTV ratio over time. When you borrow at 5% APR on a DeFi protocol, the outstanding debt grows continuously, which means your effective LTV creeps upwards even if the collateral price remains perfectly stable. On a $10,000 loan at 50% LTV, the accrued interest adds roughly $42 per month to your debt, pushing your LTV from 50% to approximately 50.2% after just one month. Over a full year without any repayment, that same position drifts from 50% to 52.5% LTV purely from interest accumulation. This silent drift catches borrowers off guard during extended holding periods and is one reason why periodic partial repayments are essential for maintaining your target safety margin.

The interaction between LTV management and tax planning also deserves careful attention. In the United Kingdom, repaying a crypto loan is not a taxable event, but the method you use to fund that repayment matters enormously. Selling appreciated cryptocurrency to reduce your LTV triggers a capital gains event, potentially creating a tax liability that offsets the benefit of maintaining a safer position. Conversely, adding fresh stablecoin collateral purchased with fiat avoids any capital gains implications while achieving the same LTV reduction. Planning your collateral management strategy with tax consequences in mind can save you thousands of pounds annually, particularly if you are managing positions across multiple protocols with different collateral types.

Multi-asset collateral strategies offer another layer of LTV optimisation that many borrowers fail to exploit. Rather than depositing a single volatile asset, splitting your collateral across two or three assets with low correlation to each other can provide a more stable effective LTV. For example, a position backed by 60% ETH and 40% stablecoins will experience roughly 60% of the LTV volatility compared to a pure ETH collateral position, because the stablecoin portion acts as a buffer during price drops. Aave V3's efficiency mode takes this further by offering higher LTV limits for correlated asset pairs, allowing you to borrow more safely when your collateral and debt are denominated in assets that move together.

Seasonal and cyclical patterns in cryptocurrency markets also inform intelligent LTV management. Historical data shows that volatility tends to increase during Bitcoin halving cycles, major regulatory announcements, and traditional market stress events. Borrowers who proactively reduce their LTV ratios by 5-10 percentage points ahead of known volatility catalysts — such as Federal Reserve meetings or major protocol upgrades — create additional breathing room precisely when it matters most. This approach requires more active management than simply setting a static LTV target, but it has consistently outperformed passive strategies during the high-volatility episodes that cause the majority of liquidations.

Finally, consider building a dedicated emergency fund specifically for collateral top-ups, separate from your regular savings. A reserve equal to 20% of your total collateral value, held in stablecoins on the same chain as your borrowing position, allows you to respond to margin calls within minutes rather than hours. The cost of maintaining this reserve — the opportunity cost of capital sitting idle — is trivial compared to the 5-15% liquidation penalties that most protocols impose. Treating this emergency fund as a non-negotiable component of every borrowing position, rather than an optional extra, is what distinguishes disciplined borrowers from those who eventually lose capital to preventable liquidations.

Sources & References

- Compound. (2025). Compound Collateral Factors. LTV calculations and borrowing limits.

- Aave. (2025). Aave Risk Parameters. Official documentation on LTV ratios and liquidation thresholds.

- MakerDAO. (2025). MakerDAO Whitepaper. Collateralization ratios and stability mechanisms.

- Aave. (2025). Aave LTV Parameters. Loan-to-value ratios and risk management.

- Nexo. (2025). Nexo LTV Guide. CeFi platform LTV requirements and tiers.

Frequently Asked Questions

- What is the LTV ratio in crypto lending?

- LTV (Loan-to-Value) ratio is the percentage of your collateral value that you can borrow. Formula: (Loan Amount / Collateral Value) × 100%. For example, borrowing $5,000 against $10,000 collateral = 50% LTV. Lower LTV means a safer position.

- What is a safe LTV ratio for crypto loans?

- Conservative safe ratios: Bitcoin 30-40%, Ethereum 25-35%, Altcoins 20-30%. This provides a 30-50% buffer before liquidation. Never exceed 50% LTV on volatile assets. Stablecoins can safely use 70-80% LTV

- What's the difference between max LTV and liquidation threshold?

- Max LTV is the maximum you can borrow initially. The liquidation threshold is the LTV at which your position is liquidated. Example: Aave ETH has 80% max LTV but liquidates at 82.5%. The 2.5% difference is your safety buffer.

- How do I calculate my current LTV?

- Current LTV = (Current Loan Value / Current Collateral Value) × 100%. Check your platform dashboard for real-time values. Remember that both the loan (due to interest) and the collateral (due to price changes) have constantly changing values.

- What happens if my LTV gets too high?

- If your LTV reaches the liquidation threshold, your collateral gets automatically sold to repay the loan. You lose your collateral, plus a liquidation penalty of 5-15%. To prevent this, add collateral or repay the loan when the LTV approaches the danger zone.

- Can I borrow more if my LTV is low?

- Yes, if your LTV is below the maximum allowed, you can borrow more. Example: 30% current LTV with 50% permitted max means you can borrow an additional 20% of collateral value. However, consider keeping a buffer for safety.

- How does price volatility affect LTV?

- Collateral price drops increase your LTV (more dangerous). Price increases decrease your LTV (a safer approach). Example: A 20% drop in collateral price can change a 40% LTV to a 50% LTV. This is why conservative LTV ratios are crucial for volatile assets.

- Should I use the maximum LTV offered by platforms?

- No, never use maximum LTV. Platforms offer high LTV to attract users, but it's a hazardous approach. If the platform offers a maximum LTV of 70%, use only 35-40% for safety. The extra borrowing capacity isn't worth the risk of liquidation.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.